Despite showing signs of life recently, Diageo‘s (LSE:DGE) price is down 35% from its 2022 highs. And I continue to think this is a passive income opportunity I’m not willing to miss.

Historically, opportunities to buy Diageo shares at attractive prices haven’t come around all that often. So rather than wondering when the stock’s going to recover, I’m looking to buy it.

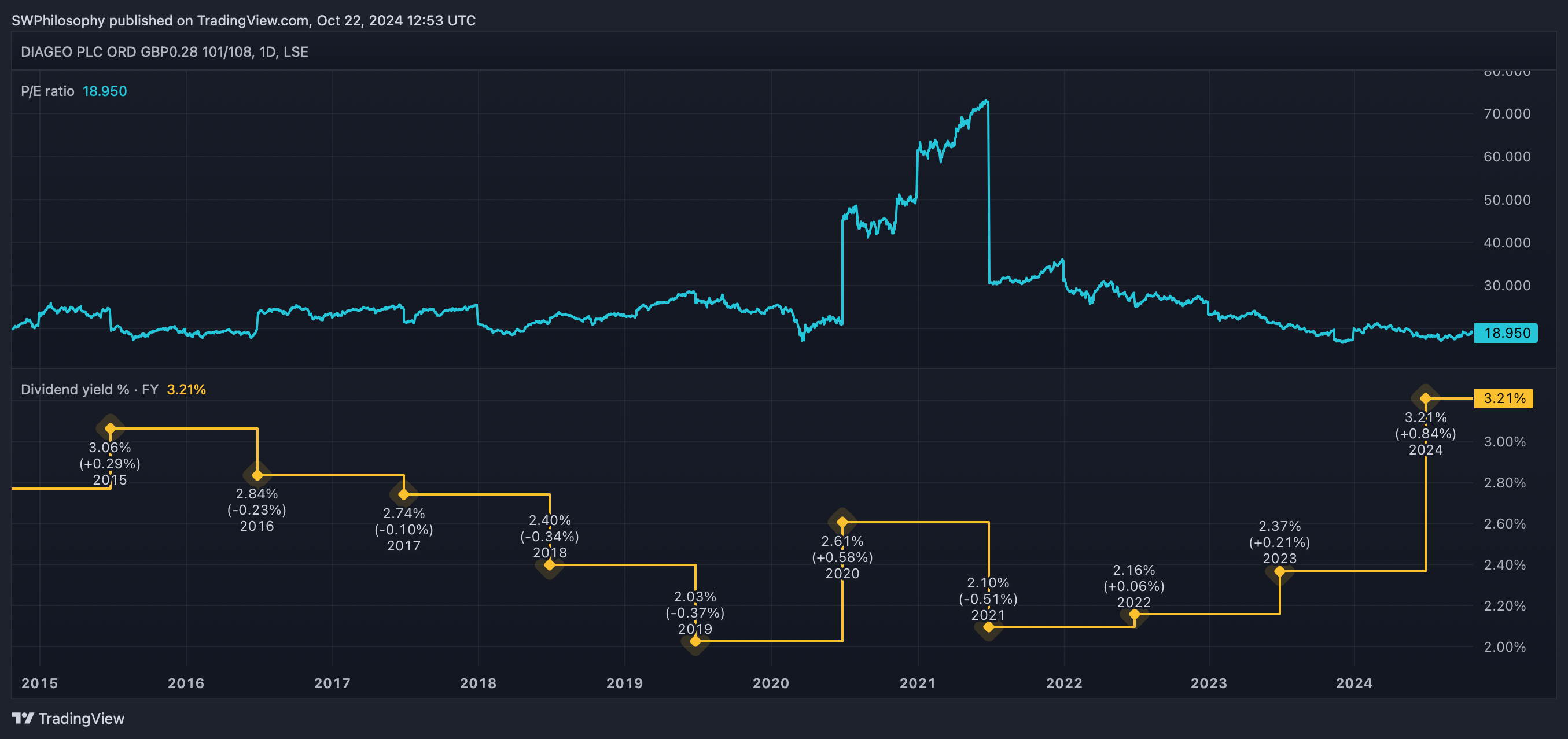

Valuation

Diageo shares currently trade at a price-to-earnings (P/E) ratio of just under 19 and have a dividend yield of 3.2%. Both of these represent unusually good value.

Diageo P/E ratio & dividend yield 2014-24

Created at TradingView

Over the last decade, the chance to buy the stock and get a dividend yield hasn’t come around often. In general, investors have had to settle for something between 2% and 3%.

Diageo shares traded at some unusual P/E multiples during the Covid-19 pandemic. But even in more usual times, investors have generally had to pay above 20 times earnings for the stock.

I don’t think anything significant has changed with the underlying business though. So while I wouldn’t have bought the stock at its highs, it’s a different story now.

Macroeconomic challenges

Diageo’s been battling through a difficult macroeconomic environment, which is why the stock’s been falling. Furthermore, there’s reason to think this might continue.

LVMH recently reported earnings for the third quarter of 2024. And the results were disappointing, with revenues down 3% compared to the previous year.

That has investors wary of a luxury goods recession, but the biggest decline came in its Wines & Spirits division, where sales fell 7%. This is something Diageo shareholders should take note of.

There’s not much the company can do about the macroeconomic environment. But the risk of consumer discretionary spending remaining weak is a genuine one for the FTSE 100 firm.

A durable business

Despite this, I’m still looking to load up on Diageo shares. I’ve been buying the stock for around a year or so and I think it could be a great source of long-term passive income.

The company has category-leading products in a number of categories, including scotch, gin, and vodka. And this isn’t a coincidence.

Diageo’s size means it’s able to spend heavily on marketing to keep its brands relevant to consumers. This makes it difficult for rivals to displace its competitive position.

The company’s scale also gives it a big advantage. It allows the firm to acquire smaller competitors in a way that adds value to them before they become significant challenges.

Why I’m still buying

Finding an under-the-radar bargain in the stock market can be an incredibly rewarding feeling. But sometimes the best opportunities are in plain sight.

Diageo shares have been cheap for a while, but I still think they’re unusually good value. With the company’s key assets still intact, I’m continuing to build my investment.