Shares in UK packaging firm Macfarlane Group (LSE:MACF) look very attractive to me. As far as I can tell, only three analysts cover the stock and I think the market is underestimating the firm’s prospects.

Earnings are currently depressed by what I believe are cyclical pressures, but the stock is trading at an unusually low multiple. As a result, the share price looks to me like a coiled spring.

What does MacFarlane do?

MacFarlane is a packaging company. It adds value for its customers by cutting down on waste, reducing breakage costs, and improving transport and storage efficiency.

Around 86% of total revenues come from its distribution division. As the UK’s largest packaging distributor, it benefits from economies of scale that help reduce costs.

The other part of the business is manufacturing. This is a smaller part of group sales, but higher margins from a focus on bespoke packaging for high-value products mean it generates 26% of operating profits.

Acquisitions have been key to MacFarlane’s strategy. Since 2020, the firm has added 10 separate firms to its organisation, which accounts for a lot of its growth.

Discount pricing

Right now, Macfarlane shares trade at a price-to-earnings (P/E) multiple below 12, which is at the lower end of its 10-year range. But given the company’s recent performance, this isn’t entirely unjustified.

Macfarlane P/E ratio 2015-2024

Source: TradingView

The firm’s latest earnings report reported declines in both sales (8%) and profits (4%). And it would have been worse but for the effect of some recent acquisitions.

Manufacturing revenues were strong but lower prices and volumes on the distribution side resulted in overall sales falling. Management is largely attributing the weaker demand to cost-of-living pressures.

The risk for investors is that these prove persistent – and there’s not much Macfarlane can do about this. And if earnings keep falling, I see no reason to expect the P/E multiple to expand from its current level.

Investment thesis

Even accounting for ongoing inflation weighing on consumer demand, I think there’s a good chance earnings could move higher from their current levels. One reason for this is recent acquisition activity.

In its latest report, management noted its acquisition of Polyformes (completed in July) should boost earnings from the next update. I therefore expect to see strength in the manufacturing division.

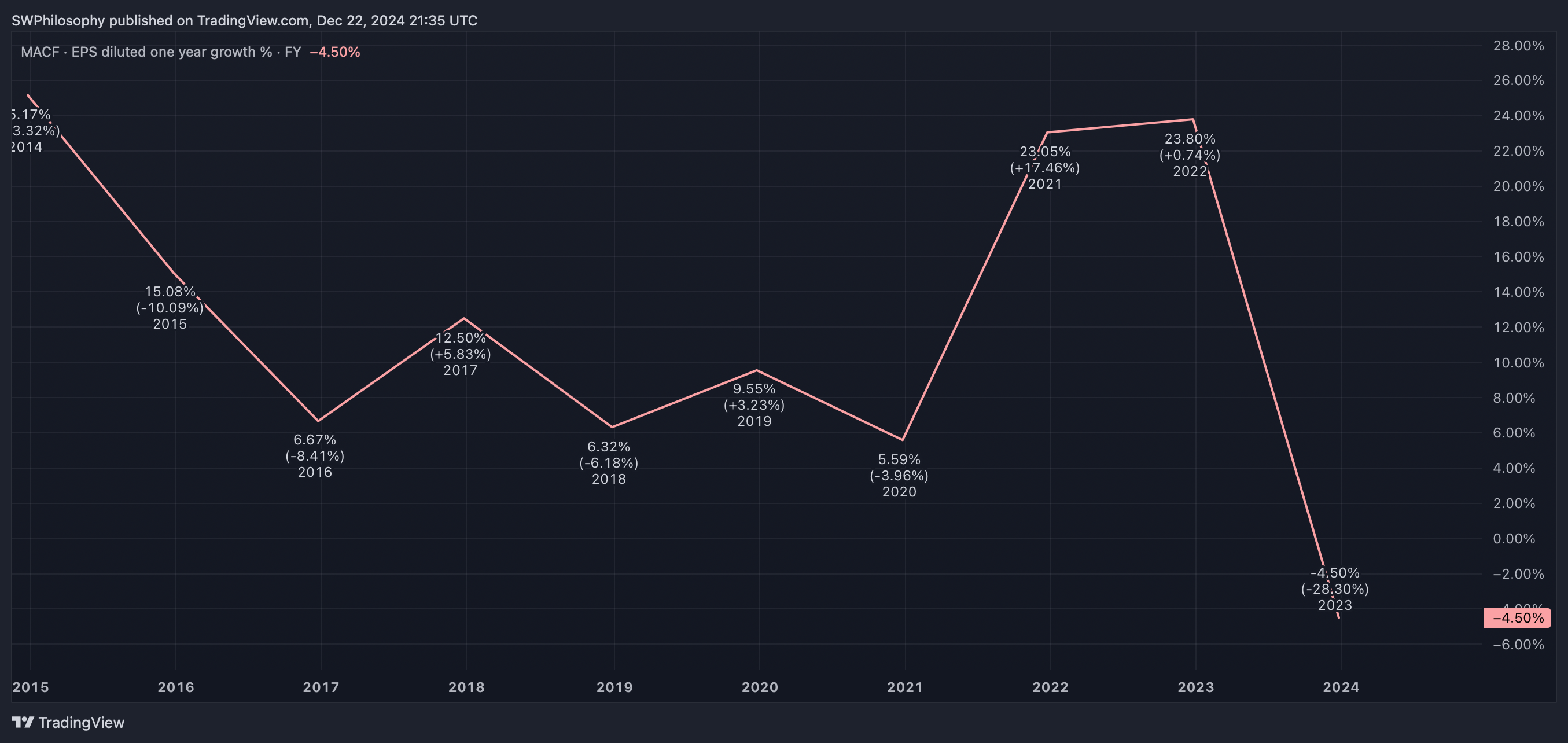

Investors should also note that Macfarlane’s growth has been exceptionally strong during the last couple of years. As a result, earnings per share (EPS) have grown at an average of 8.5% over the last decade.

Macfarlane EPS growth 2020-2024

Created at TradingView

I think the company can get back to growing its earnings in 2025. And if it does, I can see clear scope for the stock to trade at a higher multiple, providing a strong return for investors.

My price target

If earnings per share get back to 10p (2022 levels), I think the stock could trade at a P/E multiple of 15 (the mid-point of the 10-year range). That implies a share price of £1.50, which is 39% above the current level.

I think this could happen in 2025. But even if it takes three years, investors could still do very well by owning the stock – even before factoring in a dividend with a current yield of 3.34%.