The FTSE 100 has had a bumpy week but this former stock market darling actually ended Friday (9 August) slightly higher at 1.95%. It’s a rare slice of good news in a dismal year.

Investors in global spirits giant Diageo (LSE: DGE) will take any positive they can get right now. Its shares hit a year-low of 2,368p on Monday 5 August. Today they’re just a few pence higher at 2,426.5p.

The Diageo share price is down 27.95% over 12 months, which looks to me like a massive buying opportunity for a blue-chip stalwart like this one.

I thought Diageo was a great opportunity when I bought its shares last November, two weeks after plunging sales in Latin America and the Caribbean triggered a profit warning. So far I’m down 14.17%. So much for my timing.

Diageo can recover

This is the second time I’ve been caught out chasing profit warnings. My Burberry shares have fallen by more than a third since I decided they were an unmissable bargain.

While I like to get a cheap entry price, I buy shares with a minimum five to 10-year view, so they have plenty of time to recover. I wouldn’t buy more Burberry today but I think Diageo may be over the worst. Its shares now look too cheap to resist by its standards, as this chart shows.

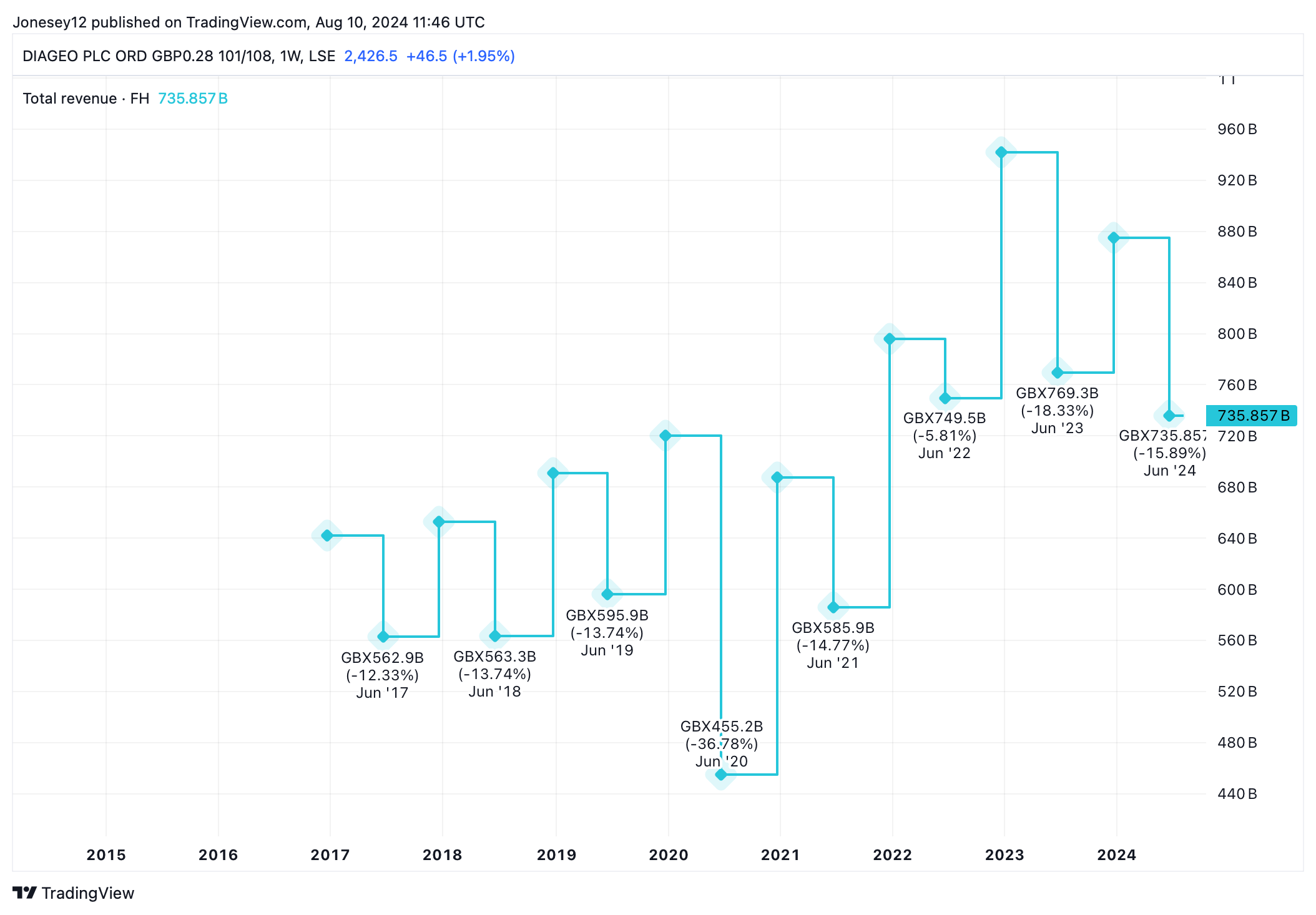

Chart by TradingView

Group revenues have been horribly patchy though, and this chart highlights the scale of the recent decline.

Chart by TradingView

I don’t expect Diageo to instantly snap back. Preliminary results published on 30 July showed a 1.4% drop in net sales to $20.3bn, albeit worsened by unfavourable exchange rate movements.

Organic operating profit fell 4.8% to $304m. Of this, all but $2m was down to Latin America & the Caribbean. CEO Debra Crew said “continued macroeconomic and geopolitical volatility” didn’t help. The problem is that global volatility isn’t going to end any time soon. It could get worse.

Recovery opportunity

On the plus side, record productivity savings of nearly $700m and $2.6bn in free cash flow add a splash of sunshine.

Diageo has always been seen as a defensive stock, because people typically carry on drinking in hard times. Yet there are two new threats to this scenario. The first is that Diageo now targets the premium end of the drinks market and drinkers are still drinking, but they’re trading down.

Then there’s the big question mark hanging over the stock – and much of the Western world. What’s happening to Gen Z? One in four don’t touch alcohol. While this has boosted sales of alcohol-free Guinness, can other brands get a new lease of life? Alcohol-free Johnnie Walker, anyone? Smirnoff? For a long-term investor like me, these trends pose a long-term threat.

Despite these concerns, I think the Diageo sell-off has gone too far. I have a pretty big serving, worth almost 5% of my self-invested personal pension. But I’m tempted to buy a splash more. At today’s low price, it seems rude not to.