Plenty of stocks look like excellent value at the moment. But with UK shares heating up, this might not be the case for much longer.

Here are two brilliant picks I reckon investors should consider buying this month.

JD Sports Fashion

My first selection is JD Sports Fashion (LSE: JD.). There’s no sugarcoating it, the stock has put up an incredibly underwhelming performance this year. It’s down 30.1% year to date and 51.9% from its five-year high.

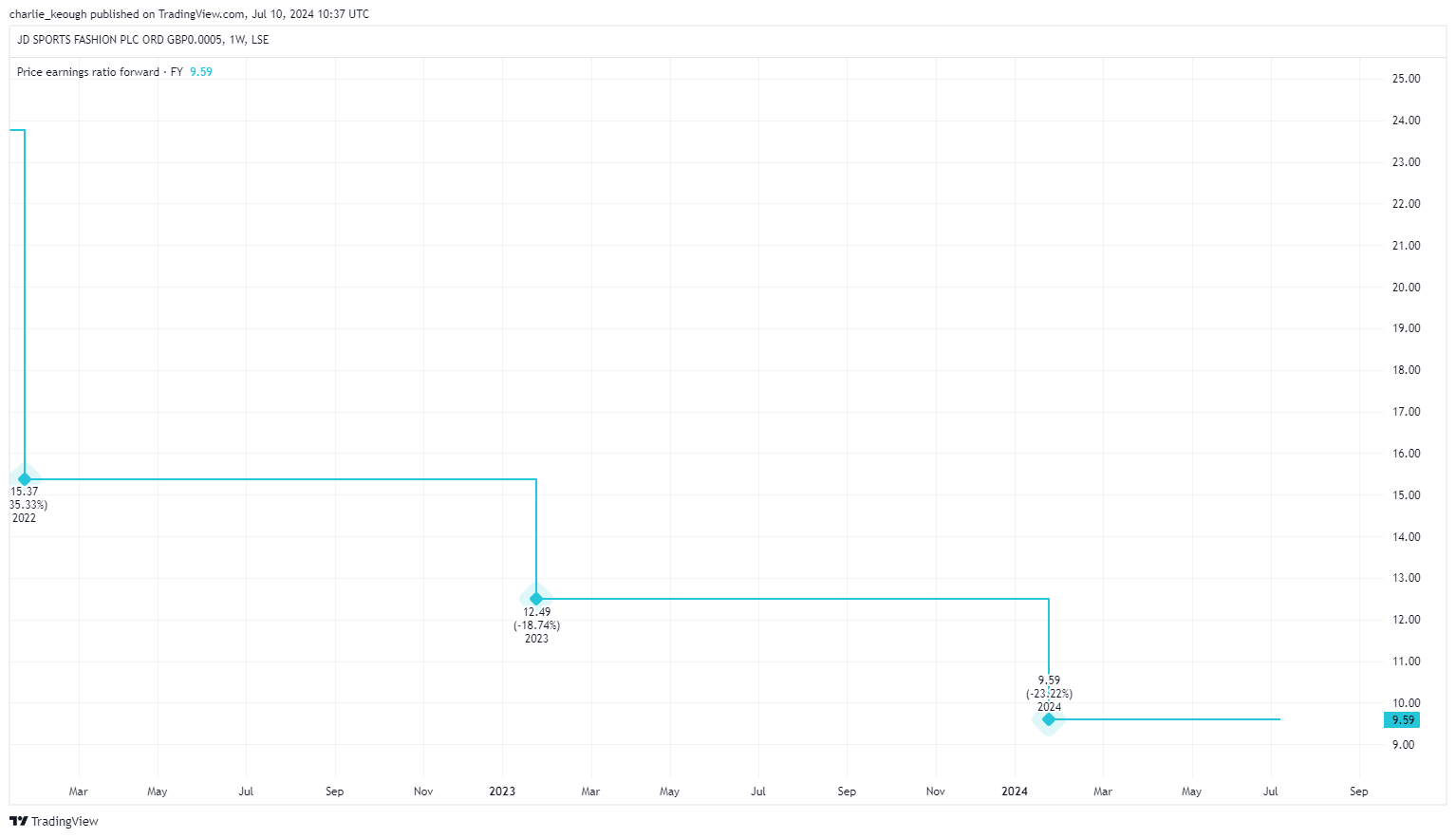

But for contrarian investors who like to sniff out value, I reckon JD is one to consider. With its decline, it now looks cheap as chips, trading on 10.7 times earnings. As the chart shows below, it’s trading on just 9.6 times forward earnings.

Created with TradingView

It has issued a couple of profit warnings in recent times and that has spooked investors, hence its cheap price. Consumers are still tightening their purse strings, so it may be the case that we see JD struggle for a bit longer as tougher trading conditions persist.

That means I could hold out and try and buy at the bottom. But as the old adage goes, time in the market is better than timing the market. I see plenty of value in JD shares today. I think it would be too risky to try and wait for the stock to bottom out.

Zooming out, I see plenty of reasons to like JD. It functions in the athleisure sector, which is predicted to grow at an annual compound growth rate of 9.3% until 2030. And despite an already strong position in the market, the business continues to expand. It opened 216 new stores last year.

Analysts have a whopping 160.2p 12-month target price for the stock. That’s a massive 42.9% premium from its current price. While those, of course, are just predictions, I think they highlight just how much potential JD has.

Rio Tinto

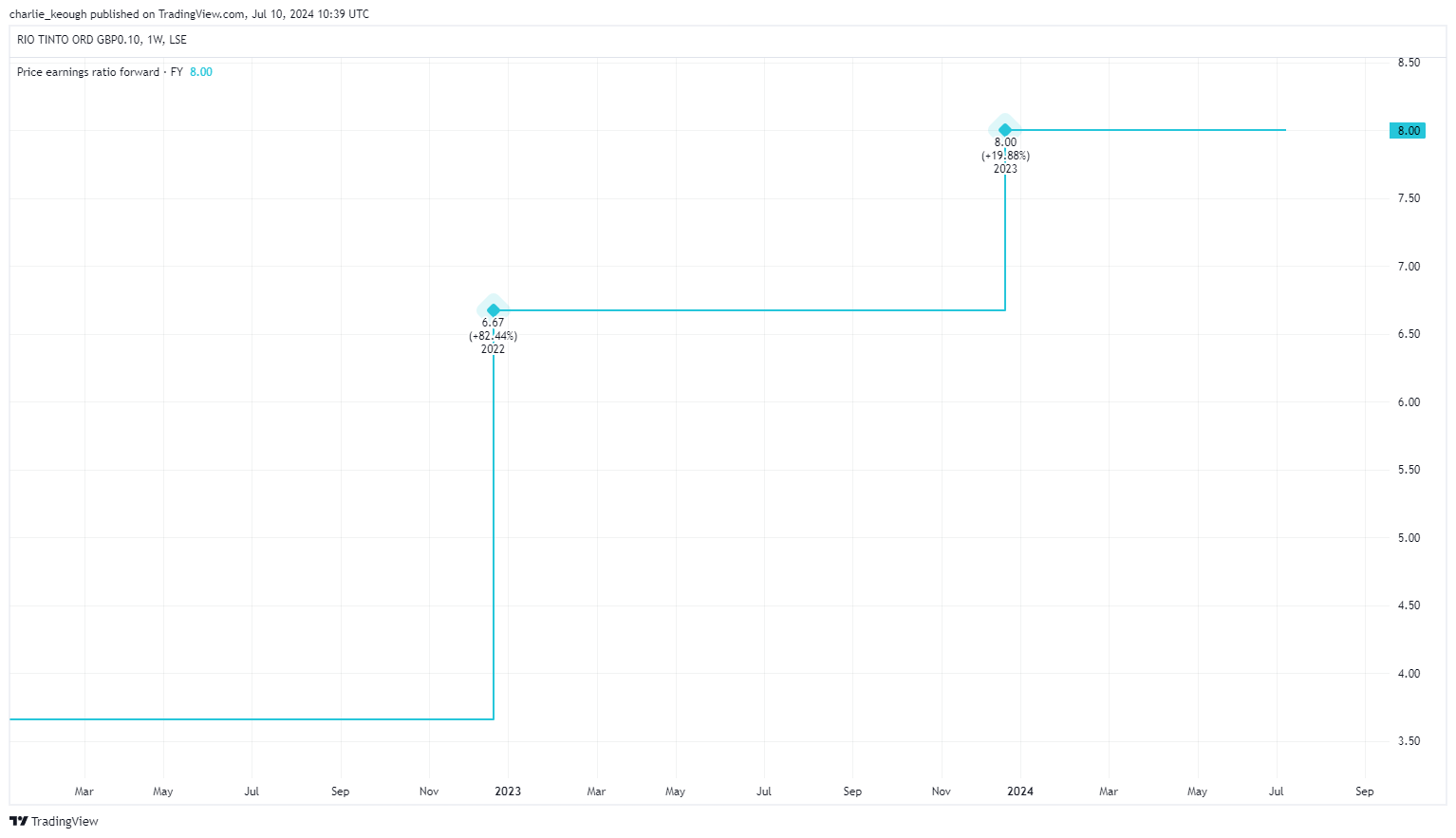

Next under the microscope is Rio Tinto (LSE: RIO). The FTSE 100 stalwart is down 11.6% so far this year. That said, it’s up 6.9% in the last 12 months.

Its fall in 2024 means the stock is trading on 10.8 times earnings, below the Footsie average. As seen below, it’s trading on just eight times forward earnings.

Created with TradingView

I think that’s cracking value for a business of Rio Tinto’s nature. I’m bullish on the moves it’s making as it expands further into the lithium sector. That includes its £825m acquisition of the Rincon lithium project a few years back.

Its cheaper price also means its dividend yield has been boosted. It sports a 6.6% yield, placing it inside the top 10 of the Footsie’s highest payouts. What’s more, it has consistently paid a dividend for over a decade.

The stock is cyclical. So, we may experience a few more blips like the one that has occurred this year. Around half of its sales derive from China, which can also provide complications.

But for the long term, I think Rio Tinto could be a savvy buy at its current price. Chinese demand has slowed but we’re seeing signs of it picking up again.

Analysts have a £61.64 12-month price target. That’s an 18.4% increase from where it is today.