In today’s budget (6 March), the Chancellor of the Exchequer said the government intends to sell part of its 31.9% shareholding in NatWest Group (LSE:NWG). I think this could be a good opportunity for me to generate some additional passive income.

It usually makes me wary when a major investor sells up. But in this case, I think the decision is based on a need to deliver some pre-election tax cuts, rather than anything being fundamentally wrong with the bank.

Shareholder returns

Indeed, NatWest recently confirmed that its dividend, in respect of the year ended 31 December 2023 (FY23), is going to be 17p a share. This means its stock is presently yielding 6.8% — comfortably above the FTSE 100 average of 3.9%.

And analysts are forecasting the payout to increase to 15.7p (FY24), 17.6p (FY25), and 18.3p (FY26).

If correct, this means a £10,000 investment today could generate £2,057 in passive income, over the next three years.

Of course, dividends are never guaranteed.

But the bank is expected to generate nearly £11bn in post-tax profits from 2024-2026. Based on the current number of shares in issue, this is 2.4 times the anticipated cost of the forecast payouts.

This suggests there’s plenty of scope to continue paying generous dividends, even if the bank’s financial performance deteriorates slightly.

And there could be some capital growth, too.

That’s because, looking at the charts, it seems to me that the bank is undervalued.

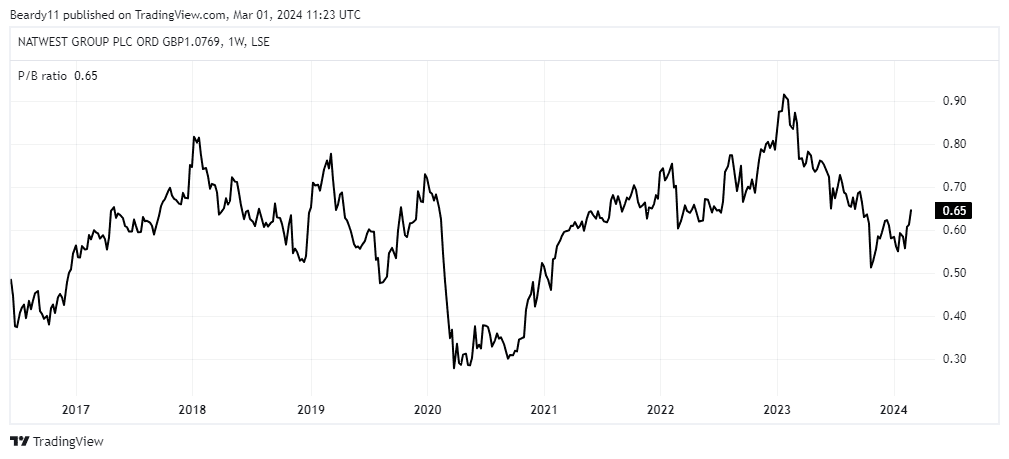

Historically low valuation

The price-to-book (P/B) ratio compares a company’s stock market valuation with its accounting value. As shown below, NatWest’s P/B is currently 0.65, and has been falling for some time.

Chart by TradingView

A P/B at this level means if it ceased trading, sold all its assets for the amounts disclosed in its financial statements, and used the proceeds to clear its liabilities, it could return 379p a share to shareholders.

That’s a 49% premium to its current stock price.

It’s a similar story when it comes to its price-to-earnings (P/E) ratio. The bank is currently trading on a multiple of just over five.

As the following chart illustrates, this has been falling steadily for some time. With a P/E of eight — which is what NatWest was valued at 12 months ago — it’s share price would be 57% higher.

Chart by TradingView

A difficult industry

But there are a number of risks associated with the sector. In particular, earnings per share can be volatile.

Chart by TradingView

And that means dividends can be erratic. For example, in 2020, the bank only returned 3p to shareholders.

NatWest is also heavily exposed to the UK economy which is currently in a technical recession. At 31 December 2023, 92% of its loans were made to UK individuals and companies.

Despite these challenges, I think the upcoming sale is a good opportunity to buy a solid passive income stock for my portfolio.

Also, due to the large number of shares involved, I think it’s likely they will be sold at a discount to the current market price. That sounds like a win-win to me.

When the time comes, I’m therefore going to register my interest in what will probably be — in monetary terms — the government’s largest share sale for over 30 years.