Are these the best UK shares to consider buying as US stocks whiplash?

US stocks took a pretty big tumble as April kicked off, only to reverse course as the threat of tariffs got put on pause. By comparison, UK shares are proving to be a better safe haven from all the volatility. The FTSE 100 has taken a hit, but it pales in contrast to the recent downward trajectory of the S&P 500 and Nasdaq.

And with US investors potentially exploring international opportunities, the UK stock market might be a popular destination for new capital. So which UK shares could be good buys right now?

Exploring options

Global tariffs put a lot of pressure on businesses with complex supply chains. But there are plenty of British enterprises that don’t have this sort of exposure. For example, Safestore Holdings (LSE:SAFE) owns and operates a portfolio of self-storage facilities in the UK and Europe with next-to-no direct ties to the US economy.

Similarly, Howden Joinery operates within the UK and Europe. While the firm imports a significant amount of wood, lumber was explicitly excluded from proposed US tariffs. Then there’s also AstraZeneca. The pharmaceutical giant relies on the US healthcare market for a large chunk of its revenue stream. But, just like lumber, pharmaceuticals were also excluded from the tariff list, leading to minimal disruption.

The list of UK shares that could have minimal or no impact from US tariffs is quite substantial. And these companies are likely where most investors could find refuge from volatility.

Tariffs could cause indirect damage

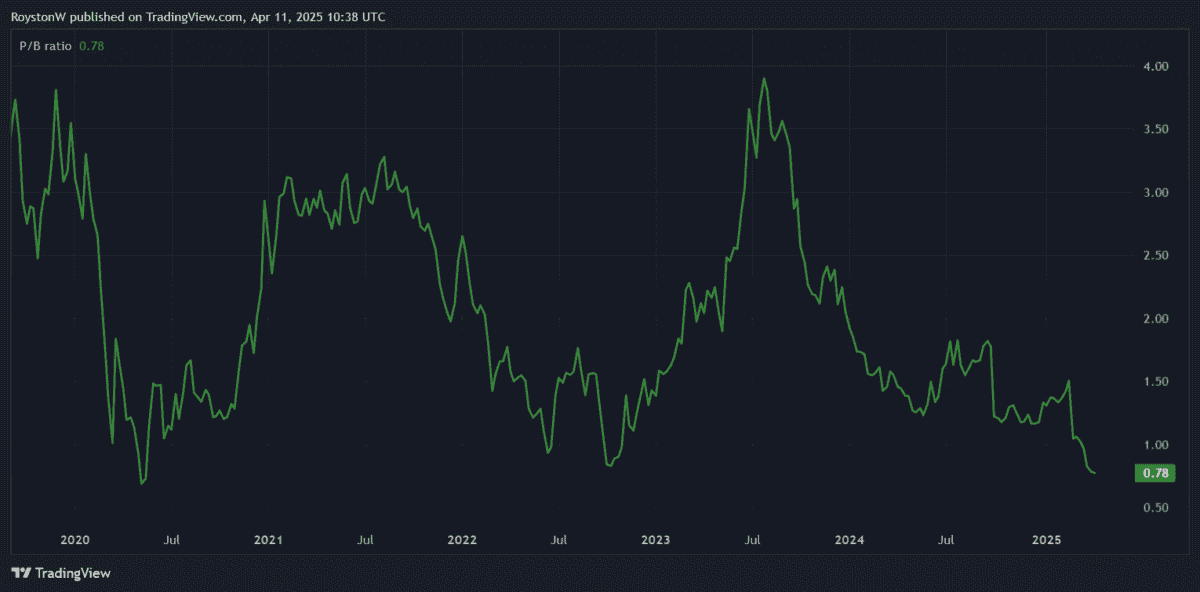

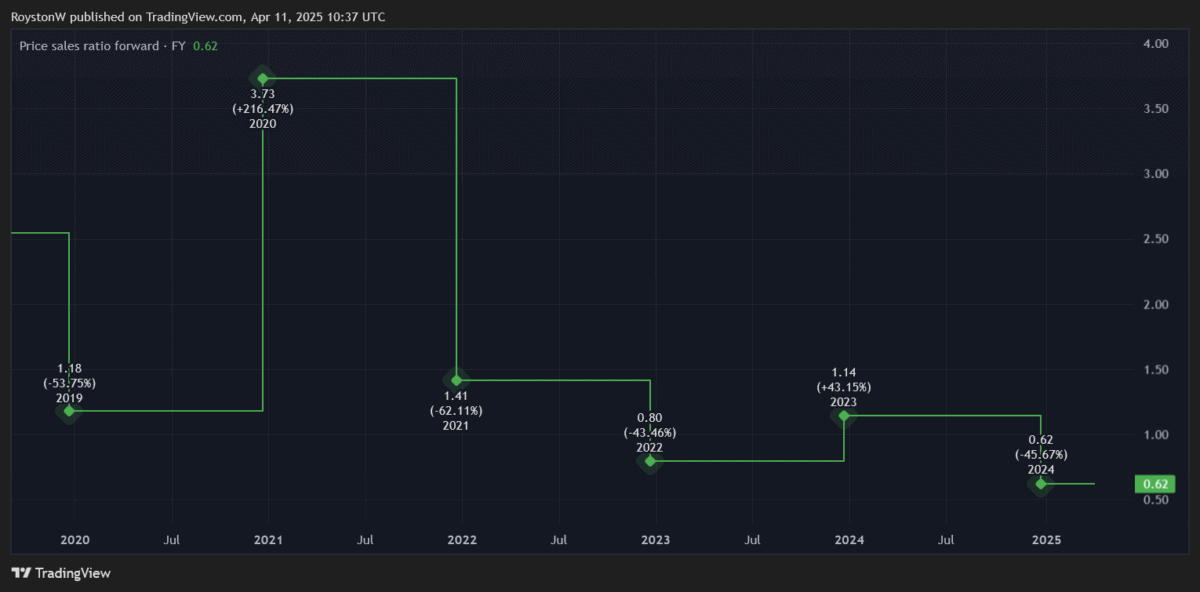

Just because a business won’t get directly caught in the crossfire of a potential global trade war doesn’t mean the stock’s an instant buy. Investors still need to do their due diligence and look at the operational risks as well as potential rewards. With that in mind, let’s take a closer look at Safestore.

The company’s in the middle of navigating a cyclical downturn in the self-storage market, with its 2024 performance landing pretty flat. Thankfully, investors did see a welcome return to growth in the first quarter of 2025. However, while not directly exposed to the US market, Safestore could still be indirectly impacted.

Retaliatory tariffs from the UK or Europe could drive up domestic costs, resulting in both businesses and individuals seeking to save more money. That could translate into Safestore customers ending their leases, putting more pressure on the firm’s cash flow in the short term.

Stay focused on the long run

Tariffs will undoubtedly cause headaches in the business world if they end up being implemented in markets beyond China in the next 90 days. However, in the long term, high-quality businesses will adapt. And in my opinion, Safestore seems perfectly capable of doing just that.

This isn’t the first time it has had to navigate a downturn in its target market. And while most of its competitors are being more conservative, management continues to invest in its European expansion to perfectly position the firm for when the cycle eventually ticks back up.

In fact, it was this strategy that saw Safestore become the industry leader in the UK. And if management can replicate its success in Europe, the stock could have a long way to climb in the long run. That’s why I’ve already added this business to my defensive income portfolio.