I can’t believe the Lloyds (LSE: LLOY) share price. After declining for a decade, it’s finally pointing the right way. We’ve waited long enough.

Lloyds shares are up 36.95% over the past year, more than three times the 12.1% return on the FTSE 100 over the same period. They boast a trailing yield of 4.78%, lifting the total return to more than 40%.

Who saw that coming? I did, actually. I bought the shares in June and September last year, at an average price of 43.62p. Today, they trade at 57.84p, plus I’ve reinvested two dividends. I don’t often get my timing this right.

FTSE 100 income star

I felt the stock was due a revival but I didn’t expected it to happen while interest rates were still high, house prices stagnating, and consumer spending squeezed.

Yet it has. One reason is that investors are forward-looking. They think things will get better six to nine months down the line at which point rising wealth will drive up demand for savings and mortgage products.

Better still, this will cut debt impairments. In fact, that’s already happening. Lloyds now allocates just £57m to cover bad loans, against £243m last year.

Investors seem to be factoring in rather a lot of good news but the recovery will also bring challenges. When the Bank of England finally cuts base rates, this will erode Lloyds’ net interest margins, the difference between what it pays savers and charges borrowers. Margin compression has already begun and it hurts.

On 24 April, Lloyds reported that Q1 net interest margins had dropped from 3.22% to 2.95%, while operating expenses climbed. Profits fell 28% to £1.63bn. That doesn’t seem to bother investors. Lloyds’ shares have climbed 12% since then.

Investors have also chosen to ignore a potential motor finance mis-selling scandal, for which Lloyds has set aside a modest £450m. Any compensation bill could be much higher than that. Nobody knows.

This stock isn’t as cheap

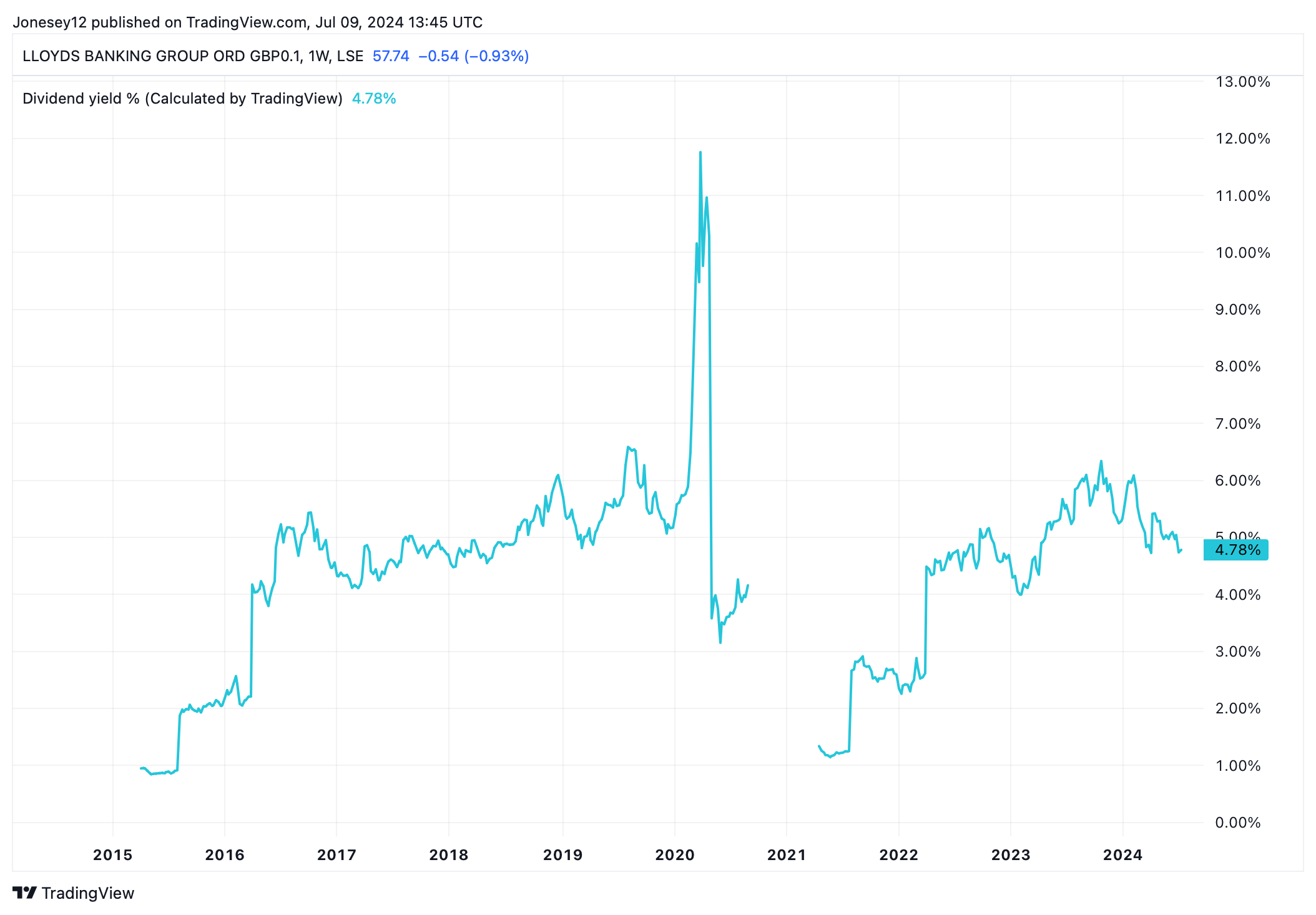

Another problem is that the rising share price has driven down the yield. Last October, it spiked at 6.3%. Today it’s back down to 4.78%. That’s not bad, just not as good as it was. Let’s see what the chart says.

Chart by TradingView

Happily, markets forecast reckon the shares will yield 5.47% in 2025. Even better, they reckon net income will jump from £3.76bn in 2024 to £4.27bn in 2025.

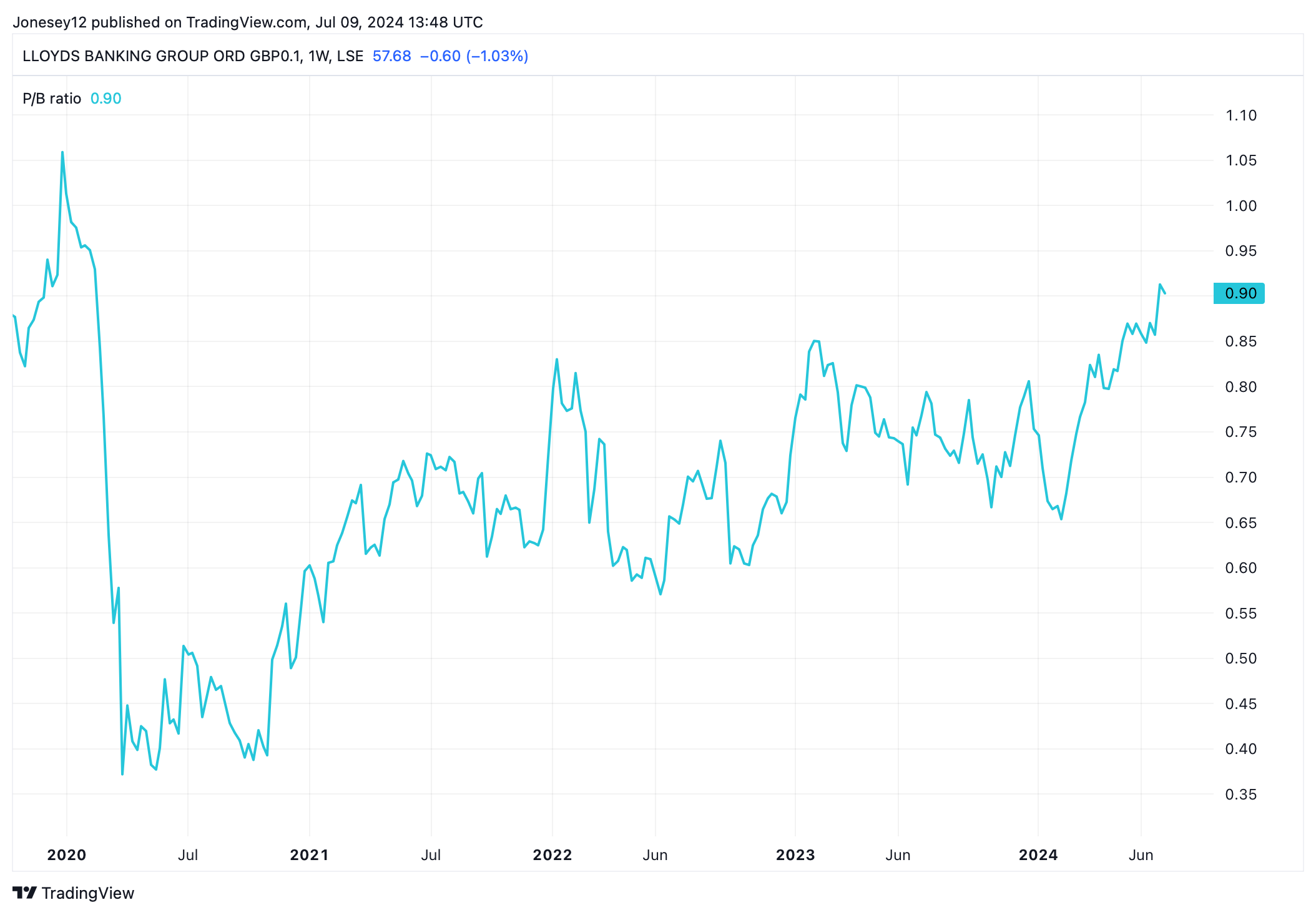

Another concern is that Lloyds shares aren’t as cheap as they were. Today, they trade at 10.4 times 2024 earnings. I bought at close to six times. The price-to-book ratio has steadily climbed, too. Three years ago, it languished around 0.4. Today it’s close to fair value. Let’s see what the chart says.

Chart by TradingView

I have no intention of selling my Lloyd shares. I’ve got a pretty good allocation, and plan to hold onto them for years. Decades, if I’m lucky. Yet I won’t buy more today. I think other FTSE 100 high yielders now offer better comeback potential.