I’ve been keeping a close eye on the National Grid (LSE: NG.) share price in the last couple of months. I reckon now could be a smart time for me to open a position.

Share price performance

It has been a volatile year for the stock. It was making good ground, rising 6.6% between 2 January and 22 May, until an announcement revealing a 7-for-24 rights issue sent its share price tumbling. As a result of that, its share price plummeted by over 20%.

The stock has staged a nice recovery since then. Yet while it’s gaining momentum, it’s still slightly cheaper than it was pre-announcement. That’s why I’m more tempted now than ever before to snap up some shares.

A reliable stock?

One of the main reasons why I’m keen to add it to my holdings is because National Grid is a stock that can provide stable returns.

That may sound contradictory. After all, I’ve just highlighted how its share price has been on a rollercoaster ride this year.

However, zooming out and looking at the long term, it has been a solid performer on the FTSE 100. In the last five years, it has produced a return of 27.5%. The FTSE 100, on the other hand, is up 10.4% during the same period.

National Grid is a defensive stock. The business is an electricity and gas stalwart. Keeping Britain powered is a job that’s unaffected by factors such as the state of the economy. With that comes steady revenue and cash flows.

I’m also bullish on its long-term prospects following its May announcement. With the cash it plans to raise, it’ll invest £60bn over the next five years into its growth.

Passive income

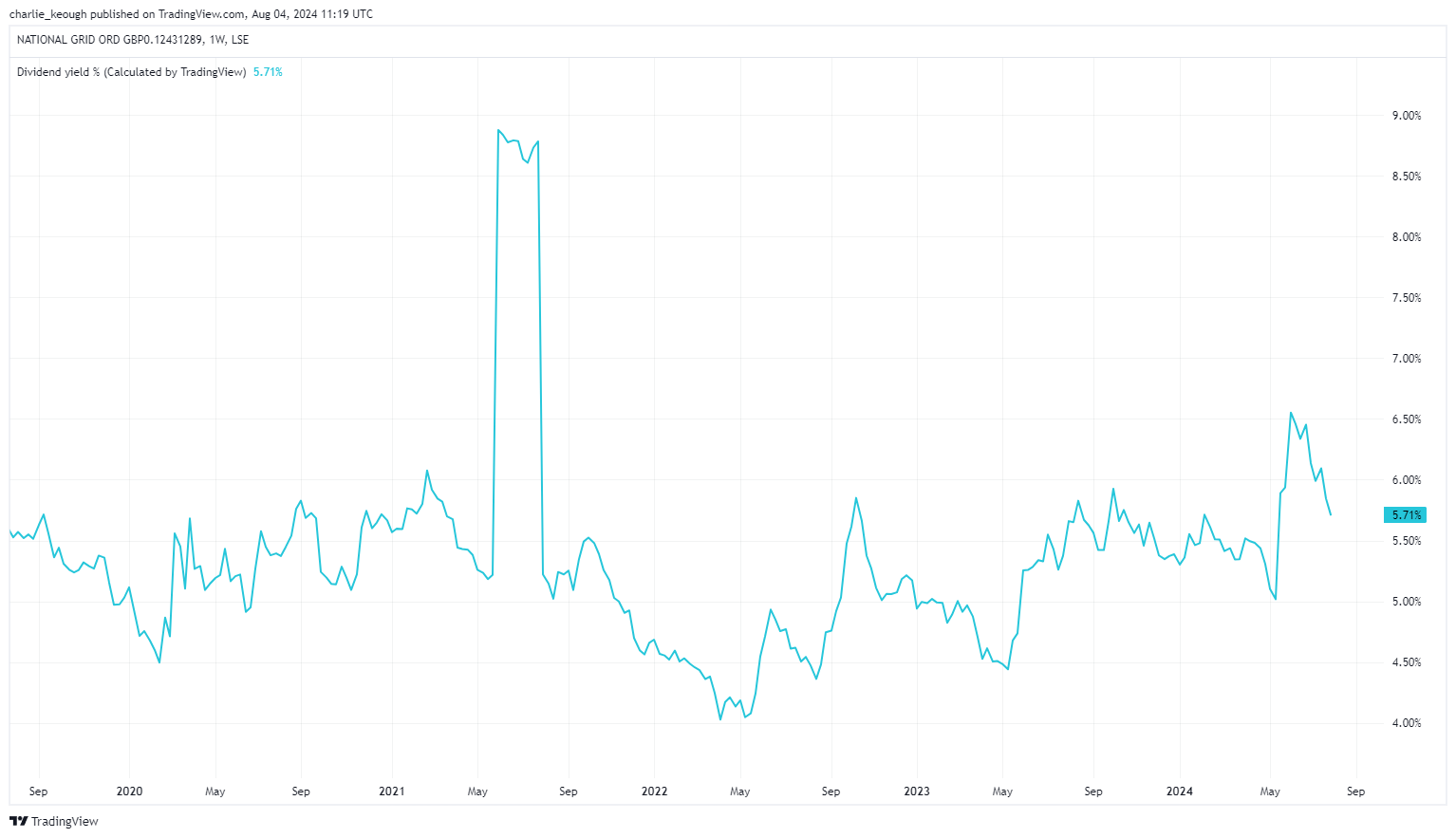

To go with its stable returns, the stock is a great source of passive income. Its dividend per share will fall given the rights issue. However, it still boasts a 5.7% yield. The firm has said it plans to maintain its progressive dividend policy in the coming years.

Created with TradingView

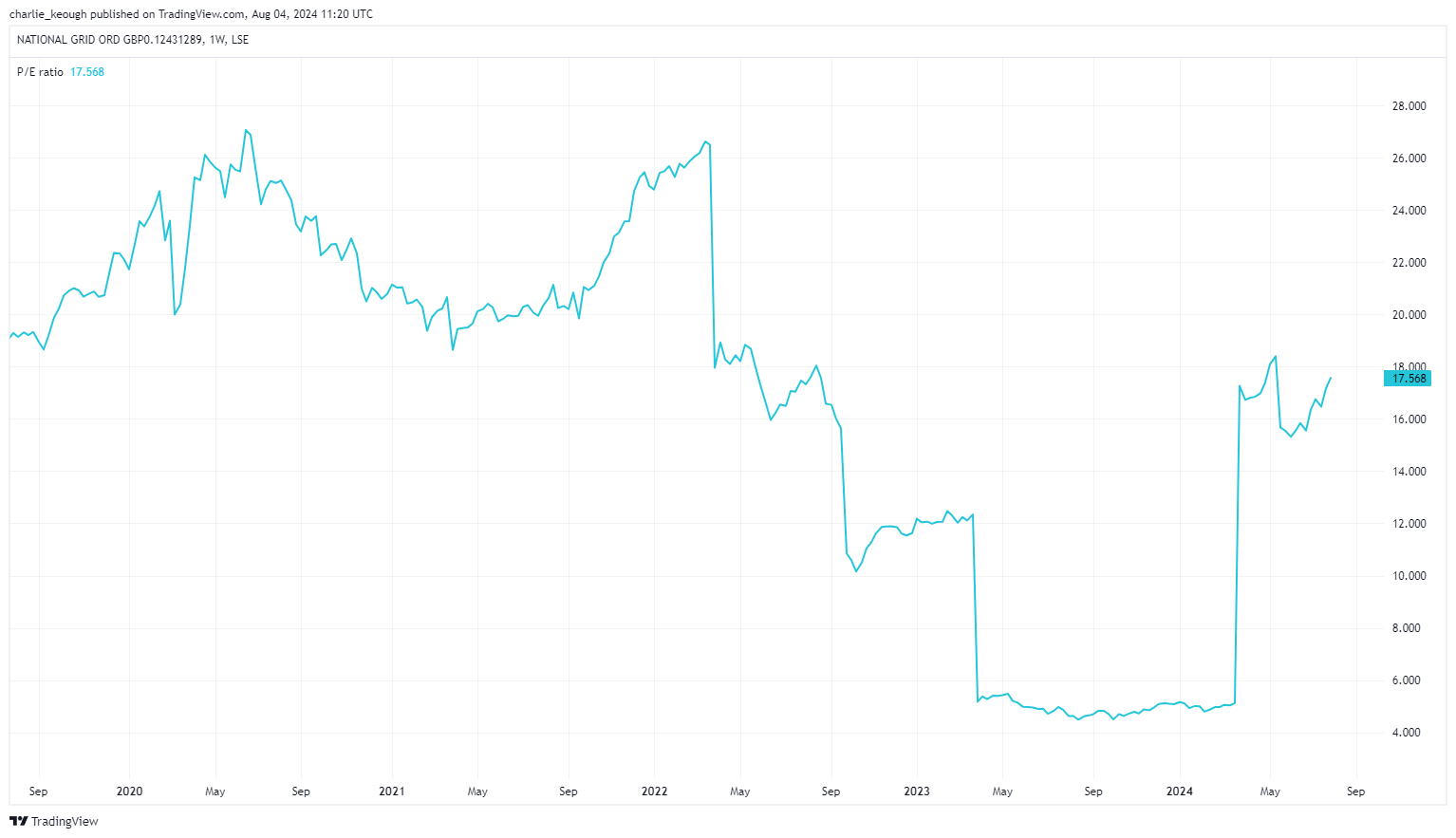

As the chart below highlights, it also looks like decent value for money, trading on a price-to-earnings ratio of 17.6. While that’s above the FTSE 100 average, I’m content with paying a premium for a business like National Grid.

Created with TradingView

My concerns

I do have some concerns. Taking a look at its balance sheet reveals the business has £43bn of debt on its books. That could hinder growth.

On top of that, there’s a risk its investment into its future doesn’t pay off. As part of this, the business will have to navigate issues such as the energy transition. That will pose a big challenge.

I’d buy

Don’t get me wrong, it’s nice to own shares that can provide massive returns, such as Nvidia. But in my opinion, it also makes a lot of sense to hold stocks such as National Grid. Such companies bring stability.

For example, it has been difficult to keep up with the Nvidia share price recently. Just last week the stock has traded between $102.7 and $121.3.

While National Grid has been volatile this year, I’m confident the last few months are a rare occurrence. That’s why, if I had the cash, I’d buy it today.