The Unilever (LSE: ULVR) share price is finally starting to live up to its potential. It’s jumped an impressive 25.38% in the last six months, and is up 15.27% over the year.

Since I hold the shares myself, I’m thrilled. This appears to vindicate my strategy of buying top FTSE 100 companies when they’ve fallen out of favour, in the hope of benefitting when they spring back into life.

I bought my first Unilever shares in June last year, which promptly dropped and left me facing a double-digit paper loss. Now I wished I’d bought more at the reduced price. I did load up on the stock in May this year, and again in June. Now I’m going to sit back and enjoy the ride.

FTSE 100 recovery play

I’m up 15.14% so far (plus a couple of dividends) and I reckon there’s a lot more to come. I plan to hold the stock for years. Decades even.

The consumer goods giant should do pretty well at every stage of the economic cycle. People still need to clean their homes and wash their hair in a recession. When the economy is doing well, they’ll spend a bit more freely.

Even inflation shouldn’t be a barrier to growth, as Unilever’s array of brands gives it pricing power, allowing it to pass on higher labour and materials costs to customers.

Yet it’s possible to take a good thing too far. Unilever boasts of having hundreds of brands, but in practice its focus has been too wide and vague.

CEO Hein Schumacher has targeted the problem and has been looking to offload lesser brands such as Timotei, Impulse, and Brylcreem, to focus on the winners. Yet his overhaul still has some way to run.

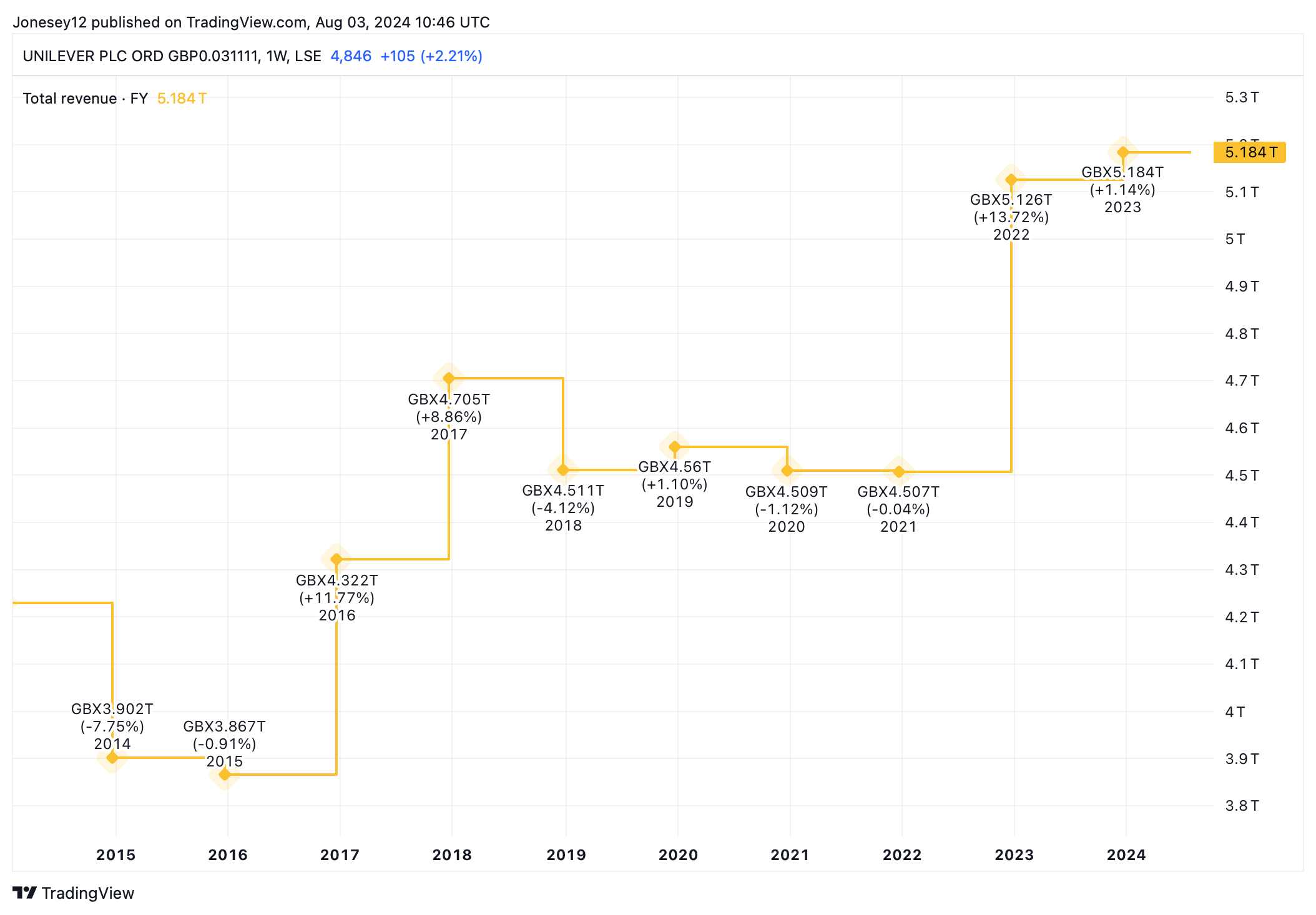

On 26 July, analysts at Berenberg hailed a return to “high-quality earnings growth”, up 3.9% year on `year. Let’s see what the chart says.

Chart by TradingView

Higher earnings have been driven by the long-awaited revival of “volume growth and gross margins”, Berenberg says. The broker hiked its target price for the stock from £49.60 to £55.70. Today, the shares trade at £48.43p, so that’s a potential increase of another 15%.

Growth and dividends

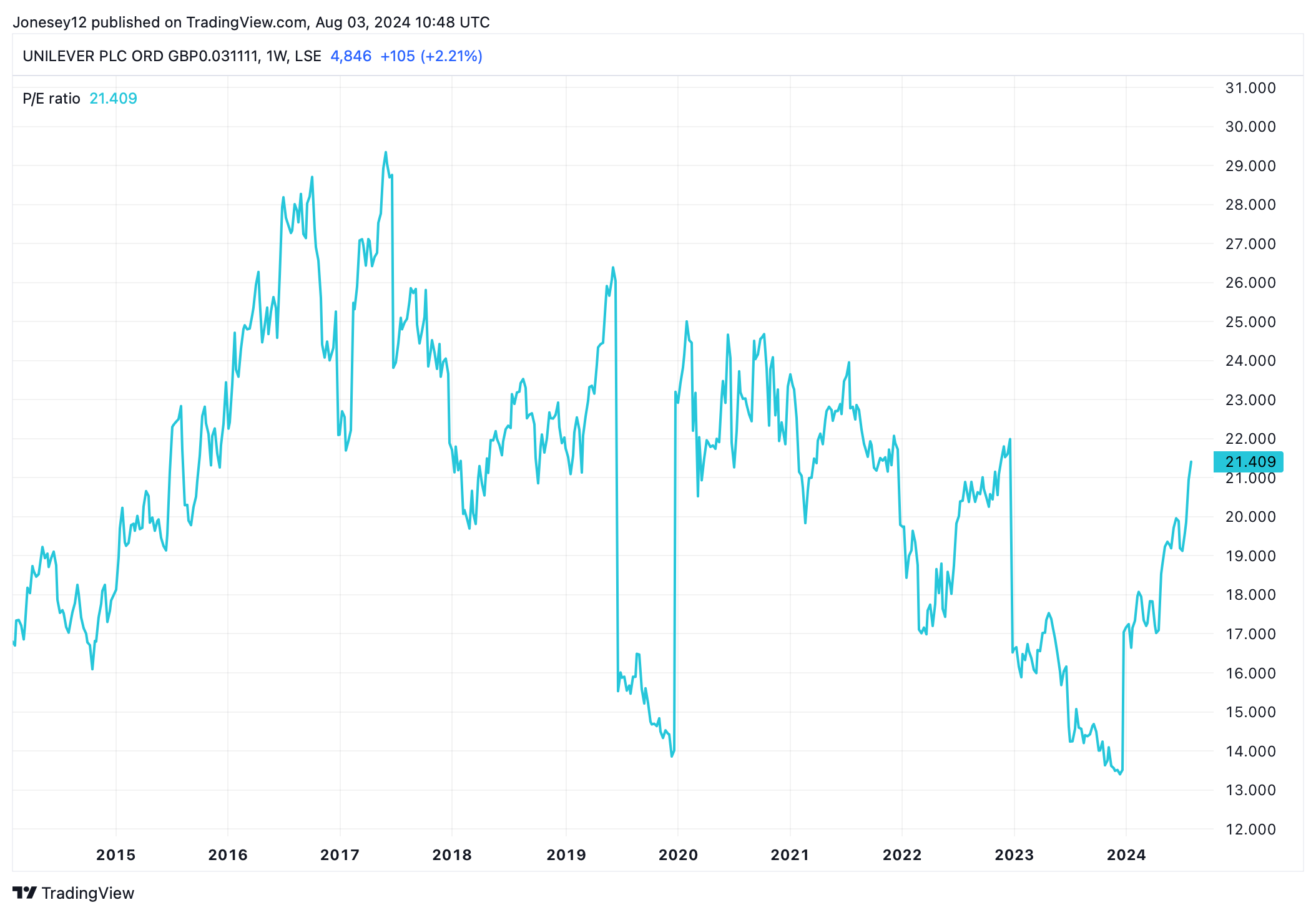

Unilever shares aren’t the bargain they were, having recovered from last year’s trough to trade at 21.09 times earnings today, as this chart shows.

Chart by TradingView

It’s never been a great income stock and the yield has declined to 3.06%. Dividend growth has been sluggish lately. The board cut the shareholder payout to €1.46 per share in full-year 2021, then lifted it slightly to €1.48 in 2022 and held it there in 2023.

There’s also a risk that today’s global uncertainty could smother the recovery. However, I noted that during Friday’s meltdown Unilever was a rare winner, growing 1.34% as its defensive abilities shone through. I think it could go on a long bull run. If so, I’ll be thrilled to have got in early.