The Diageo (LSE: DGE) share price has taken a battering lately. It’s down 15.7% over the last 12 months and 28.37% over three years.

Problems came to a head last November, after it issued a profit warning after sales plunged in its Caribbean and Latin American markets. As the local economy slowed, cash-strapped drinkers switched to cheaper local brands, while inventory issues left Diageo sitting on a heap of unsold stock.

Should I sell this FTSE 100 underperformer?

This looked like a great opportunity to buy a company I’d had on my watchlist for years, but at a much reduced valuation. I piled into Diageo’s shares on the assumption that they’d recover in sharp order. They haven’t.

The cost-of-living crisis is dragging on, not just in the UK but worldwide. Drinkers don’t have as much money as they did, or as much to celebrate.

Diageo is another FTSE 100 company that hoped to make a big splash in China, but the Chinese economy isn’t what it was. People have less cash to spend on premium Western brands. Trade war fears have intensified since Beijing slapped provisional anti-dumping tariffs on European brandy imports.

While I wait, I’ve started to worry. What if Diageo’s shares never recover? Younger people are drinking less. Apparently, they don’t want their alcohol-fuelled tomfoolery to wind up on social media, and impact their job prospects.

I’m wondering whether older people are slowing down too. I went to Sheffield University 40 years ago and had a small reunion over the weekend. We all took it easy on the booze front. The rest of Sheffield was still rocking, but maybe not as much as I remembered. That may just be my middle-aged perspective.

I’m holding but I’m not buying more

While Latin America and the Caribbean continue to disappoint, full-year 2024 results showed Africa, Asia Pacific and Europe remained “resilient”. Diageo has been holding or gaining share in its key US market too.

Hopes that the Federal Reserve will engineer a soft landing have given the stock an extra boost. Diageo shares are up 4% in the last week.

Today, Diageo has a price-to-earnings ratio of 19.34. That’s higher than the FTSE 100 average of around 15 times earnings, but cheaper than the 24 times it used to trade at. It looks steep judged by its price-to-sales ratio of 2.7 too. Investors are paying £2.70 for each £1 of revenues Diageo generates.

The 21 analysts offering one-year price forecasts for Diageo have set a median target of 2,676.5p per share. That’s just 2% higher than today’s 2,621.5p. Broker forecasts are just educated guesses, but it’s still disappointing.

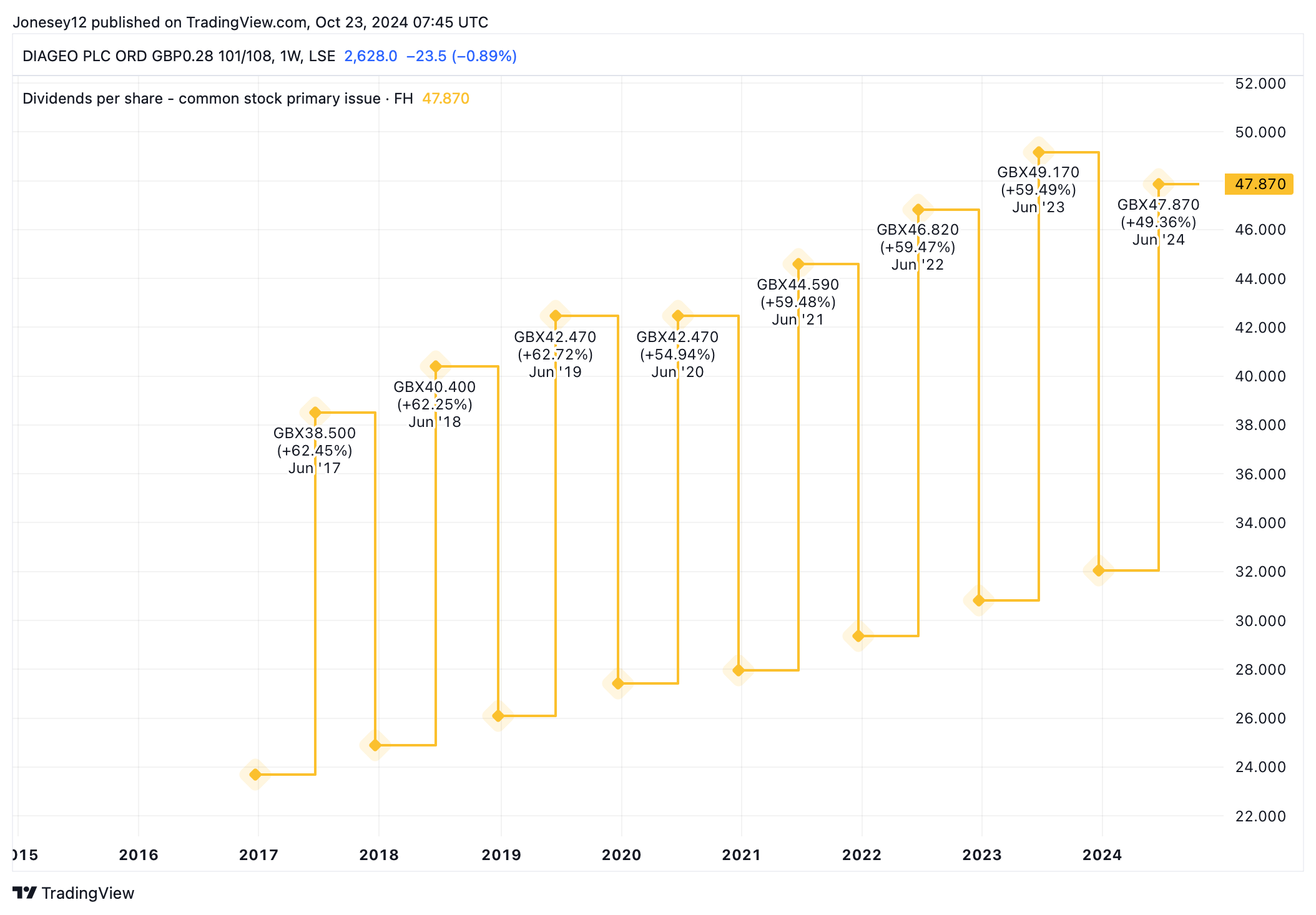

Operating margins of 21.5% and return on capital employed of 30.7% cheer me up. While the yield is just 3.07%, Diageo has a solid track record of dividend growth, as this chart shows.

Chart by TradingView

I’ve decided to hold on to my Diageo shares. I’d be daft to sell before the economic recovery, which must surely come at some point. When it does, we might all get our taste for spirits back. I’m not buying more though.