Howden Joinery Group (LSE:HWDN) isn’t an exciting artificial intelligence company. But it has a lot of the properties I look for in an investment for my Stocks and Shares ISA.

The firm has a differentiated business model, a strong competitive position, and some attractive unit economics. I think it’s worth a closer look.

B2B model

The distinctive feature of Howden’s business model is that it only sells to trade professionals. I think the significance of this is huge, but it’s easy to underestimate its importance.

Operating in this way means the business doesn’t need retail showrooms. The big advantage of this is that it’s a lot cheaper than maintaining stores and that manifests itself in two ways.

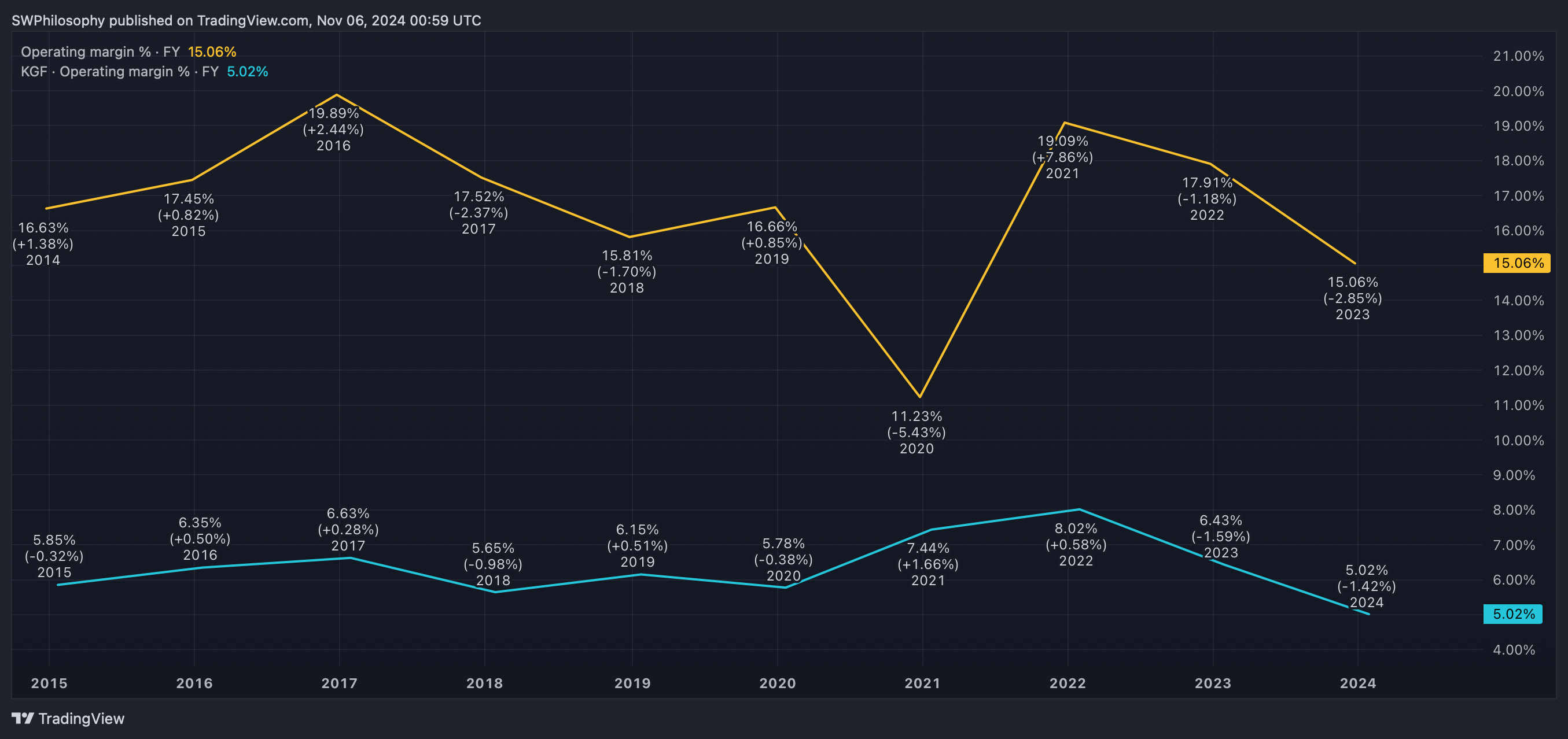

The first is that Howden can enjoy wider margins than its rivals. Over the last 10 years, the firm’s operating margins have been higher than Kingfisher‘s, which owns B&Q and Screwfix.

Howden vs. Kingfisher operating margins 2015-24

Created at TradingView

In addition, it allows the company to charge the lowest prices in the industry. As a result, it has established itself as the leader in its field, with around 70% market share.

This combination is extremely powerful. Being able to charge customers less while making more money puts Howden in a strong position that’s extremely difficult to disrupt.

Growth outlook

With a 70% market share, there’s an obvious question about where growth is supposed to come from. There are a couple of potential avenues for the business.

One involves strengthening its existing position further. That might seem optimistic, but the firm has increased its market share this year even as the overall market has been contracting.

Another is by moving into nearby markets. While Howden has a strong position in kitchen sales, the business has scope to expand into bathrooms and other adjacent lines.

The recent Budget could well also be positive for the company. The firm doesn’t stand to benefit directly from an increase in housebuilding, but it relies heavily on consumer spending.

As a result, the decision to avoid increasing taxes on workers could be positive for Howden. And this could lead to continued growth in the near future.

Inflation

The biggest risk with Howden, I feel, is inflation. In 2023, the company’s revenue growth stalled as pressure on household budgets caused home improvement projects to be deferred or cancelled.

Inflation might have come back into line with the Bank of England’s targets recently. But investors would be unwise to dismiss the risk entirely going forward.

Anyone thinking of buying the stock should expect highly cyclical earnings. They will be much better in some years than others – and the stock price is likely to reflect these fluctuations.

The key to offsetting this risk, in my view, is to consider buying the stock when it’s trading at an unusually low multiple. And that is the case right now.

Howden price-to-book ratio 2014-24

Created at TradingView

The stock is at one of its lowest price-to-book (P/B) ratios of the last 10 years. This, combined with the quality of the business, makes it one I’m thinking about for my Stocks and Shares ISA.