Of the 14 analysts offering a 12-month price forecast for Aviva (LSE: AV.), the highest prediction has the shares rising to £5.84 in the next year. That’s a rather impressive 18.9% premium from its current price.

Analysts’ forecasts must always be taken with caution. They can be, and often are, incorrect. The average target price is £5.20. That’s 5.9% higher than where the share price is now and seems more reasonable.

Of the 16 analysts providing stock ratings, seven think Aviva is a ‘strong buy’, one ‘buy’, seven ‘hold’, and just one ‘strong sell’. It seems analysts are bullish on the stock. I get it, I’ve been paying very close attention to it recently.

But I want to see if the FTSE 100 insurance stalwart has the potential to rise by nearly 19%. And if so, is it time to consider buying some shares?

Price-to-earnings

Let’s start by looking at its price-to-earnings (P/E) ratio. As shown below, it currently sits just above 13. For context, the Footsie average is 11. Rivals Legal & General (32.2), Admiral Group (23.4), and Prudential (15.4) all trade on higher multiples.

Created with TradingView

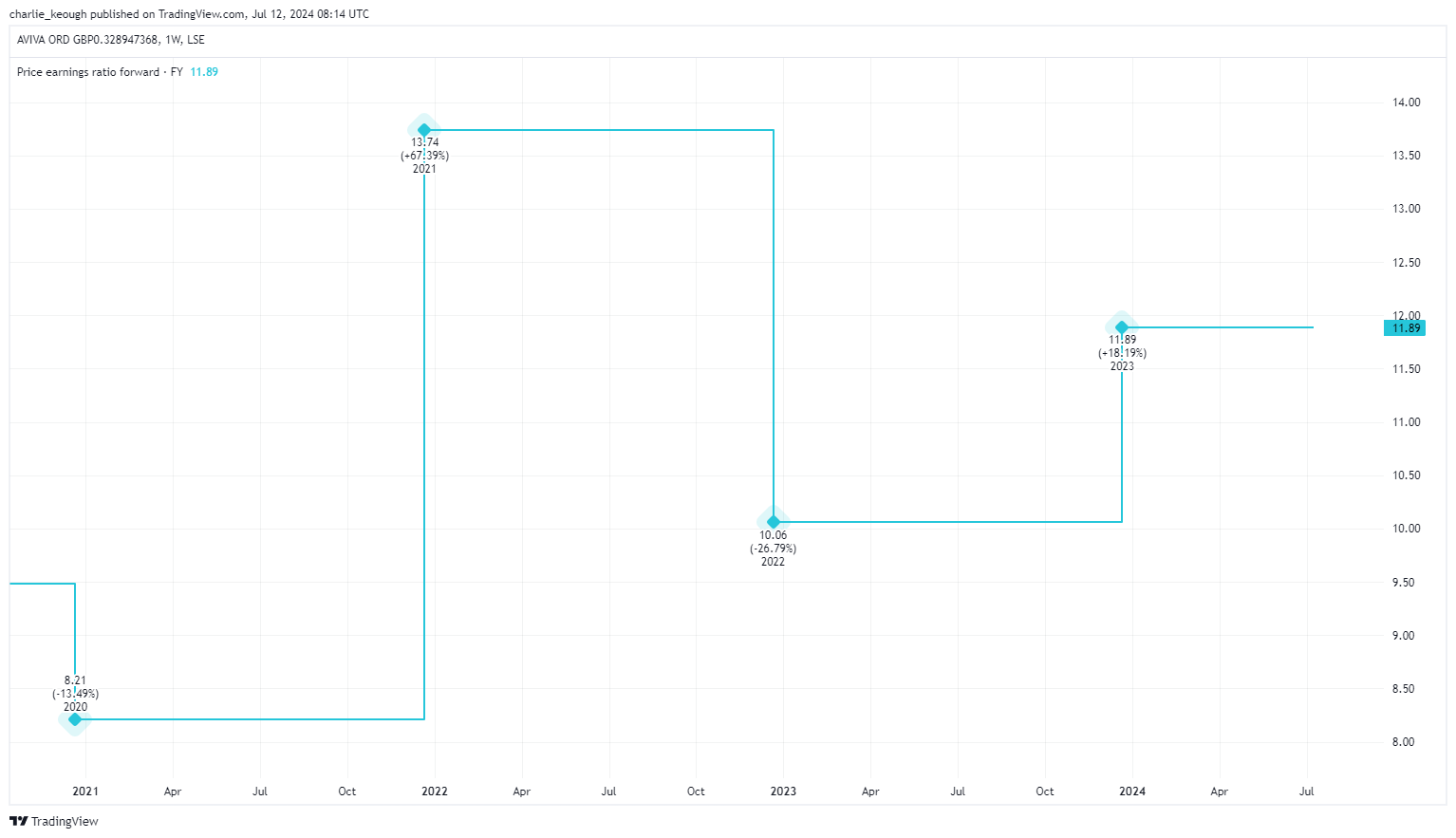

As the chart below highlights, Aviva also trades on a forward P/E of 11.9. That’s slightly higher than Prudential (11.1), in line with Legal & General (11.9), and significantly cheaper than Admiral Group (23.5). Overall, I think Aviva has an attractive valuation.

Created with TradingView

Price-to-book

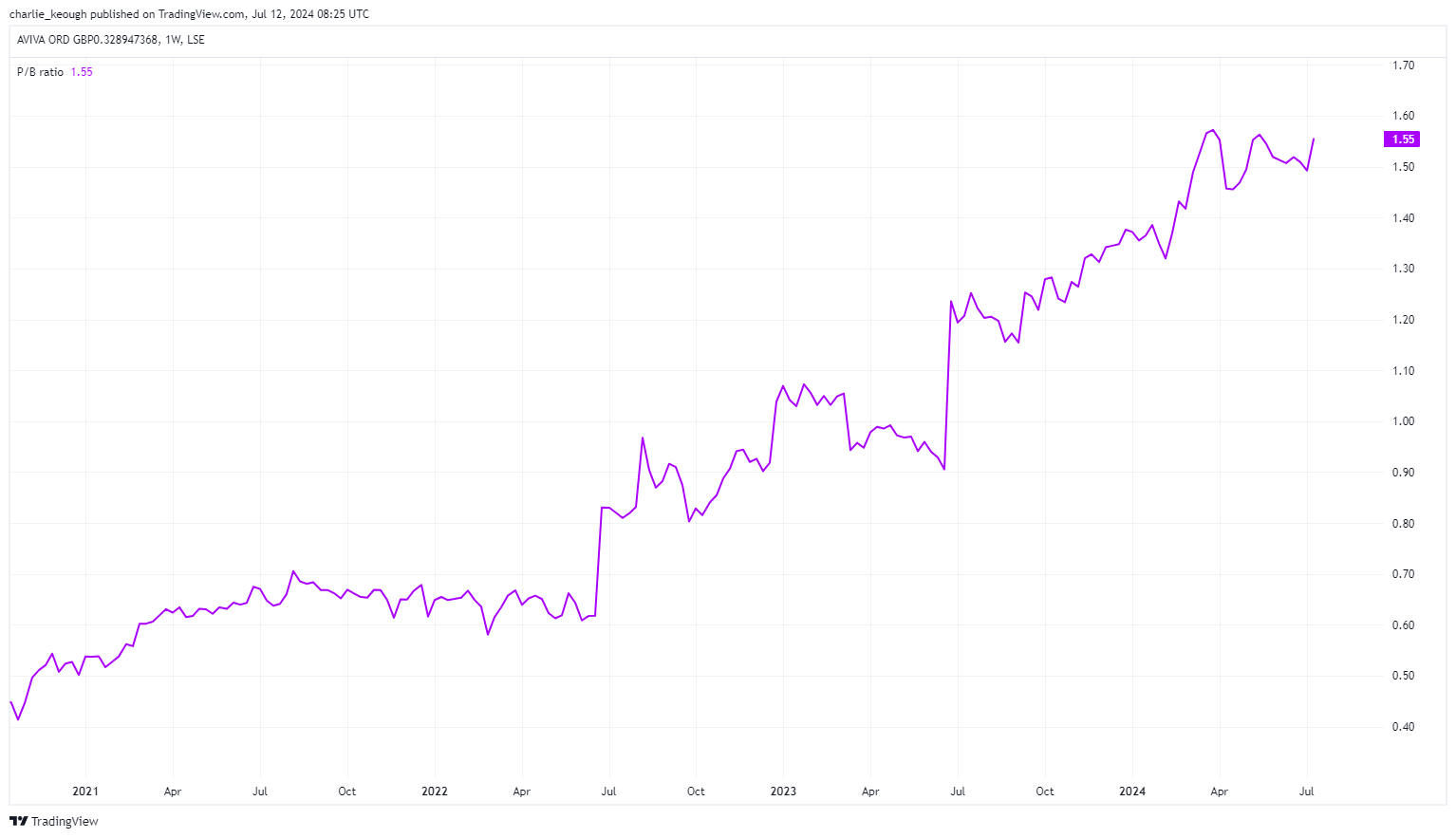

Then there’s its price-to-book (P/B) ratio to consider. As seen below, Aviva’s P/B is 1.6. That’s below the average of 3.6, including Prudential (1.5), Legal & General (3.2), and Admiral (8). Again, that signals Aviva looks like good value.

Created with TradingView

Dividend yield

Its thumping dividend yield is another thing the stock has to offer aside from its solid valuation. It sports a 6.8% yield, the ninth-highest on the FTSE 100. Its forward yield for this year is 7.1%. That’s forecast to rise to 7.8% in 2025 and 8.4% in 2026.

For 2023, the firm increased its payout by 8%. That was the third year on the bounce it had upped shareholder returns. Off the back of a strong performance last year, Aviva also put in motion a new £300m share buyback.

Fine form

It has carried its fine form from 2023 into this year. For Q1, it posted strong growth across the group, including a 16% rise in General Insurance premiums. Protection & Health sales rose 5%.

Alongside that, it further “accelerated new business” in its capital-light businesses as it continues on its streamlining mission.

The business is becoming more nimble to focus on its core markets. I think that, coupled with its strong brand recognition and market position, place it in good stead to keep delivering.

Focusing on core markets does come with inherent risks. It’s now reliant on these to perform. That includes the UK. If the economy continues to flag and consumer confidence remains low, as it may do over the next few months, that could spell trouble. There’s also the threat of rising competition.

One to watch

But with its dominant position, I’d back Aviva to excel despite these challenges.

I’m not expecting the stock to jump to £5.84 in the next year. Nonetheless, I like the look of the shares at their current price.