Forecast earnings growth of 17% a year but down 12%, is now the time for me to buy this heavyweight FTSE stock?

There was only one reason I did not buy shares in the FTSE’s Smith & Nephew (LSE: SN) after its 31 October Q3 results release.

Aged over 50 now, I focus on stocks that pay very high dividends. My aim is for these to keep generating a high income so I can continue reducing my working commitments.

My minimum annual yield requirement is 7%+, while the medical technology giant currently delivers 2.7%.

However, I would have bought the shares on Q3 results day if I had been even 10 years younger. And I would have been right to do so, I believe. The full-year 2024 results released on 25 February looked even better to me.

That said, it is still not too late for investors whose portfolio it suits to consider the stock, according to my analysis.

The key risk in the business

The catalyst for the share price drop after the Q3 2024 results was the firm’s reduction in revenue growth guidance to around 4.5%from 5%-6%.

The reason for this was the continued rollout of China’s Volume Based Procurement (VBP) programme. In this, the government bulk-buys drugs via tenders to secure the lowest prices.

This means that Smith & Nephew will have to increase production to drive revenue higher there, which will take time. The VBP effect is forecast to continue this year, and I see it as a key ongoing risk for the firm.

Strong results nonetheless

Despite this drag on revenue, Smith & Nephew posted good Q3 2024 results, in my view.

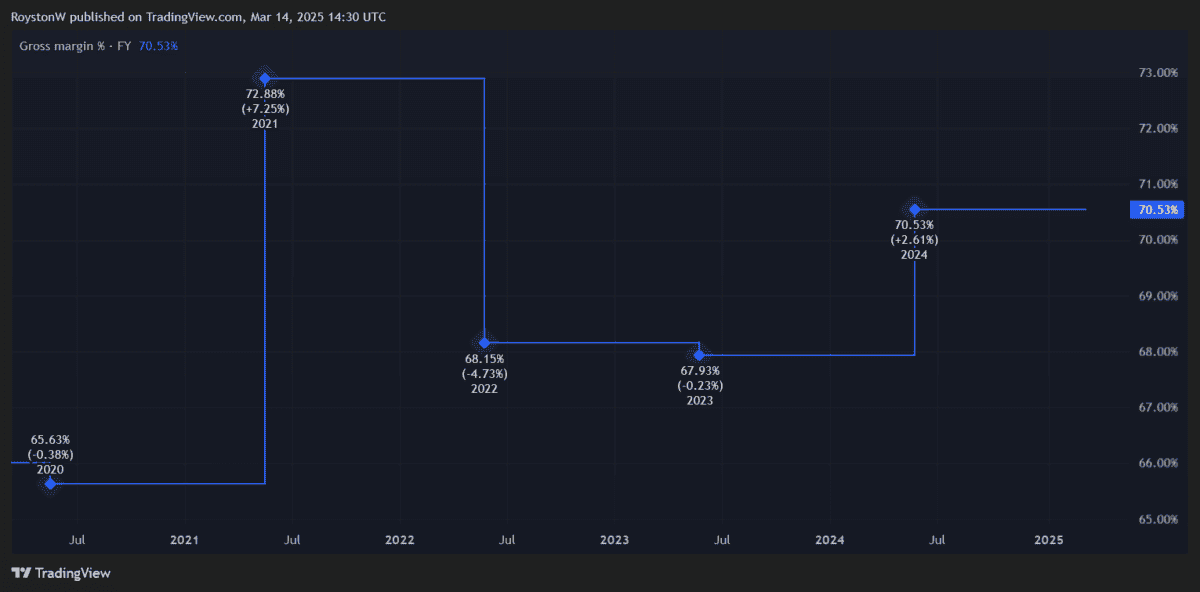

But its full-year 2024 results were even better. Revenue rose 4.7% year on year to $5.81bn (£4.59bn), with a 7.8% Q4 increase over the same period last year. Operating profit soared 54.6% to $657m, with operating margin jumping 47% to 11.3%.

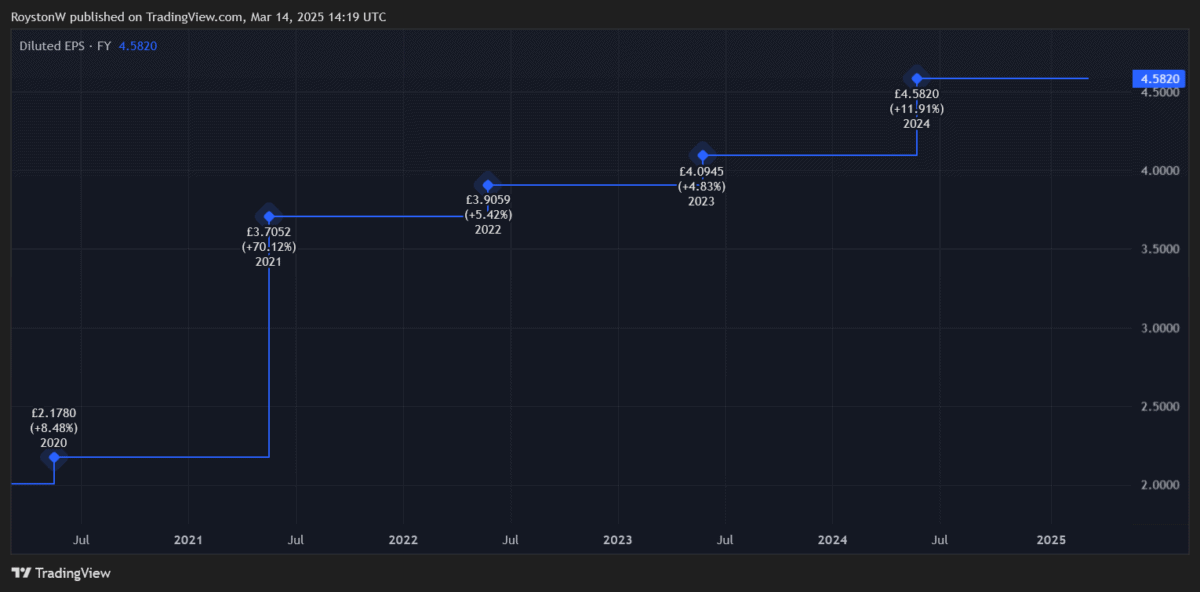

Earnings per share leapt 56.3% to 47.2 cents, and cash generated from operations rose 50.2% to $1.245bn.

Analysts forecast Smith & Nephew’s earnings will rise 17% each year to the end of 2027. It is this growth that powers a firm’s share price and dividends higher over time.

How undervalued are the shares?

Smith & Nephew trades at just 2.2 on the key price-to-sales ratio against a 3 average for its peers. These consist of EKF Diagnostics at 2, Carl Zeiss Meditec at 2.4, ConvaTec at 2.9, and Sartorius at 4.8. So, it is cheap on that basis.

The same is true of its 2.3 price-to-book ratio against a competitor average of 3.4. And it is also the case with Smith & Nephew’s 40.1 price-to-earnings ratio against the 72.5 average of its peers.

I used a discounted cash flow analysis to pin down what these all mean in share price terms. Including other analysts’ numbers and my own, this shows the shares are technically 34% undervalued at their current price of £10.95.

Therefore, given the current price of £11.10, the fair value for the shares is £16.59. Market unpredictability may push them lower or higher than that, of course. But it underscores to me how much value is left in the stock.

Consequently, if I were not focused on high-yield shares, I would buy this high-growth stock today and see it as worth further research for other investors.