The Barclays (LSE: BARC) share price has been on a tear, soaring 65% over the past year and an eye-popping 110% over two.

That makes it one of the FTSE 100’s hottest stocks, and loyal investors are finally seeing handsome returns after years of struggle. But after such a strong rally, can the momentum continue?

I’m always cautious about chasing a stock that’s already enjoyed a massive run. Also, there are signs of a slowdown, with Barclays shares dipping 2% in the last month.

Can this FTSE 100 bank keep going?

Yet the stock still looks cheap to me. It trades at just 8.4 times earnings, while its price-to-book ratio sits at 0.6. That’s well below the 1.0 typically seen as fair value for banks.

For income seekers, the dividend yield has dropped to 2.8% after the rally. But I wouldn’t be too disappointed by that. The forward yield is forecast to rise to 3%, and it’s covered a whopping 4.6 times by earnings. That’s an incredibly strong cushion, suggesting plenty of room for further hikes.

In February, Barclays said it will reward shareholders with another £1bn share buyback after a bumper set of full-year results. These saw pre-tax profits jump 24% to £8.1bn. Investment banking income rose 7% to £11.8bn as dealmaking bounced back.

The final quarter showed the momentum gathering pace, with Q4 profits spiralling from £100m to £1.7bn year on year. All this helped drive the shares to their highest level since 2010. But the board did set aside £90m for potential costs from the motor finance mis-selling scandal.

Of course, banks are never far from trouble. Earlier this month, Barclays suffered a three-day IT meltdown that left customers locked out of their accounts. The bank is now set to pay up to £7.5m in compensation. In today’s digital-first world, that kind of disruption just isn’t acceptable, especially given the drive to shutter branches. It partly explains the recent share price dip.

Share buybacks and growth hopes

The 17 analysts covering Barclays produce a median price target of almost 357p. If correct, that’s a solid increase of almost 20% from today’s 297.5p. Combine that with the dividend yield, and investors could be looking at a total return of more than 23%.

Of course, forecasts are just that – forecasts. In today’s uncertain world, plenty could change.

While higher interest rates have boosted Barclays’ margins, they also risk squeezing the global economy and pushing up debt impairments. If borrowers start struggling, bad loans could eat into profits. Unlike most FTSE 100 banks, Barclays still has a foot in the US, and could take a hit if the North American economy continues to struggle.

Barclays still has plenty of room to grow, and its valuation remains attractive. Looking ahead, the group expects to generate around £12.2bn in net interest income for 2025, up from £11.2bn. Operating margins are expected to climb from 30.3% to 38.3% this year.

For those looking to add exposure to banking stocks, it’s certainly one to consider.

There are signs that it can keep the party going for a while yet. Brokers seem to think so. But after doubling in two years, investors shouldn’t expect another quickfire surge.

In a couple of weeks, the current year’s ISA contribution deadline will pass. Any unused 2024-25 allowance an investor still has will disappear forever.

Of course, a new year’s allowance will open up. But I think it still makes sense for an investor to consider making the most of their existing allowance before it vanishes, if they can.

Not maximising the available tax benefits is not the only mistake one can make with an ISA, however. Here are another couple I am always keen to avoid!

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice. Readers are responsible for carrying out their own due diligence and for obtaining professional advice before making any investment decisions.

Mistake one: ignoring small-looking fees, year after year

Imagine paying 0.5% charges for an ISA with an initial £20,000 value each year for 25 years. Then imagine paying 0.75% instead.

What would the difference be?

In the short-term it sounds tiny. In fact, it is not. In one year, there would be a £50 difference between 0.5% (£100) and 0.75% (£150).

Over the long term, though, the contrast becomes even starker.

Chipping 0.5% off the ISA each year, after 25 years, the costs would add up to £2,355. At 0.75%, the costs would total £3,431 – over a thousand pounds more.

That is before even considering any change in share prices or dividends, remember.

I think it is a mistake for an investor not to pay close attention to the different fees and costs associated with various Stocks and Shares ISAs when deciding what one is best for their own needs.

Mistake two: taking money out of the tax-free wrapper unthinkingly

Another potential mistake is moving money out of one’s ISA unnecessarily.

When I say “unnecessarily”, I have a specific situation in mind – withdrawing dividends to spend as cash rather than using other available money.

Sometimes, of course, life’s expenses may make this necessary. But sometimes, instead of spending spare money that already sits outside of the ISA tax wrapper, it may be tempting to take dividends out of the ISA and spend them instead.

But once they are removed from the ISA, those dividends can not be reinvested inside the ISA without eating into the annual allowance.

This matters because, inside an ISA, dividends can compound with all the tax benefits of being inside the ISA.

Imagine a £20k ISA compounding at 5% per year for a decade. Within 10 years, that ISA will be worth almost £33k. So those dividends will have added another £13k of investable money inside the ISA — without using up a penny of allowance.

That helps explain why I hold shares like Topps Tiles (LSE: TPT) inside my Stocks and Shares ISA. By keeping the tile retailer’s dividends inside my ISA, I can use them to buy more shares in that company, or other ones.

Topps has been a disappointment for me lately, as it happens. The dividend yield of 7% is juicy. But the share price has fallen 23% in a year and last year’s dividend was a third less than the year before.

Ongoing weakness in the tile market overall remains a threat to sales, profits, and the dividend.

As a long-term investor, though, I plan to keep the penny share in my ISA.

I reckon tile demand will bounce back in due course. Topps’ large store network, growing online offering, and economies of scale should hopefully keep it competitive.

The shuttered Palisades nuclear plant in Michigan aims to become the first reactor in U.S. history to restart operations after permanently closing.

The restart project at Palisades would set a precedent as other closed nuclear plants in the U.S. are looking to reopen.

But inspections found Palisades’ steam generator tubes need significant repairs. The tubes are crucial components that protect the public from a radiological release.

The Palisades nuclear power plant in Covert, Michigan, Feb. 24, 2025.

Spencer Kimball | CNBC

COVERT, Mich. — A nuclear power plant on the shores of Lake Michigan is aiming to make history this fall by becoming the first reactor in the U.S. to restart operations after shutting down to be eventually dismantled.

The effort to restart the Palisades plant near South Haven, which shut down three years ago, is a precedent-setting event that could pave a path for other shuttered reactors to come back online.

But Palisades needs major repairs to restart safely, highlighting the challenges the industry will face in bringing aging plants back to life.

Palisades began commercial operations in 1971 during the early wave of reactor construction in the U.S. The plant permanently ceased operations in 2022, one of a dozen reactors to close in recent years as nuclear energy has struggled to compete against cheaper natural gas and renewables.

The owner of the plant, Holtec International, has said it hopes to restart Palisades this fall, subject to approval by the Nuclear Regulatory Commission. The restart project is backed by a $1.5 billion loan guarantee from the Department of Energy, $1.3 billion from the Department of Agriculture, and $300 million in grants from the state of Michigan.

The Energy Department on Monday approved the release of nearly $57 million from the loan, a sign that the Trump administration supports the project amid the turmoil and uncertainty in Washington over federal funding for projects started under the Biden administration.

But Holtec is facing major repairs to Palisades’ aging steam generators that could delay a schedule the NRC has called demanding. Holtec has disclosed to regulators that its inspections have found damaged tubes in the plant’s two generators, which were installed in 1990.

Inside the control room at the Palisades nuclear power plant in Covert, Michigan, Feb. 24, 2025.

Spencer Kimball | CNBC

Those tubes are crucial components that protect public health. If a tube ruptures at a nuclear plant, there is a risk that radioactive material will be released into the environment, according to the NRC. Plant owners are required to demonstrate to the NRC that if a tube does fail, any radiological release beyond the plant’s perimeter would remain below what the regulator describes as its “conservative limits.”

“The NRC is scared to death of steam generator tube ruptures. It’s a very real accident. It’s not a hypothetical,” said Alan Blind, who served as engineering director at Palisades from 2006 to 2013 under previous plant owner Entergy. Blind, who is now retired, said he supports nuclear power but is concerned about the condition of the Palisades plant based on decades of experience in the industry.

Palisades is currently in a safe condition, NRC spokesperson Scott Burnell said, as the steam generators are not in use because the plant is shut down and defueled.

Holtec President Kelly Trice told CNBC the company has done a “complete characterization” of the generators and “they are fully repairable.” The company has asked the NRC to complete its review of the repair plan by Aug. 15, but federal regulators are skeptical of the company’s timetable.

NRC Branch Chief Steve Bloom warned Holtec during a Jan. 14 public meeting that the work required to review the plan will “add to a schedule that is already very aggressive.” Eric Reichelt, a senior materials engineer at the NRC, called the schedule “very demanding,” telling Holtec at the meeting that only a few people are available at the regulatory body to do the necessary review work.

Steam generator repairs

In nuclear plants such as Palisades, water heated by the reactor passes through tubes in the generators, causing water outside the tubes to boil into steam that drives the turbines to produce electricity for the grid.

The radioactive water that circulates through the reactor and the clean water that boils in the generators do not come into contact with each other. If a tube ruptures, however, the contaminated water mixes with the clean water and radioactive material could be released into the environment through valves that discharge steam, according to the NRC.

Holtec’s inspections found more than 1,400 indications of corrosion cracking across more than 1,000 steam generator tubes at Palisades, according to a company filing with the NRC in October 2024. The tubes have not failed, Holtec CEO Krishna Singh told CNBC in February. Several had corrosion cracking with more than 70% penetration, according to the filing.

Due to the plant’s age, Palisades steam generator tubes are made of an alloy that the industry has since learned is prone to corrosion cracking, according to NRC. Holtec said it is using a technique to repair the tubes called “sleeving” in which a higher quality alloy is inserted and expanded to seal the damage.

Inside the control room at the Palisades nuclear power plant in Covert, Michigan, Feb. 24, 2025.

Spencer Kimball | CNBC

“The techniques of repair which we’re using, which is called sleeving, has been done in about 10 plants across the world and in some plants is done every outage, so this is not new, exotic technology,” Trice said. “It is a common repair technique, and we expect it to be done on time and on schedule.”

Holtec’s repair plan is scheduled to start this summer following inspection and testing, spokesperson Nick Culp told CNBC. Holtec can go ahead with the tube repairs on its schedule, but the company does so at its own risk as the NRC will decide whether the repairs meet requirements in the end, Burnell said.

But during the Jan. 14 meeting, NRC branch chief Bloom pushed back on Holtec’s statements that the company’s repair plan is following industry precedent.

“Even though you’re quote, unquote, following a precedent, it’s not exactly, because it’s a different material, different type of sleeving,” Bloom said at the January meeting. The sleeve design that Holtec is proposing for the repairs has not been installed in steam generators before, though it has been used in other heat exchangers at nuclear plants, according to a company filing.

The sleeves are made of an alloy that has not shown signs of cracking in U.S. or international plants, according to the filing. The component has a service life of no more than 10 years, the filing said. Culp said testing and analysis of the sleeves “support the expectation of longer-term performance.”

The issues with the tubes raise the question of whether the aging steam generators should be replaced, an expensive project that Palisades’ previous owners knew would be necessary at some point but never tackled.

Inside the control room at the Palisades nuclear power plant in Covert, Michigan, Feb. 24, 2025.

Spencer Kimball | CNBC

Consumers Energy, for example, sold the Palisades to Entergy in 2007 for $380 million in part due to “significant capital expenditures that are required for the plant,” including the replacement of the steam generators, according to a filing with the Michigan Public Service Commission.

Consumers Energy assumed that the generators needed to be replaced in 2016, according to the filing. Entergy, however, did not replace them after purchasing Palisades. The utility found that purchasing new generators would make the plant economically unfeasible, said Blind, who was engineering director at Palisades during that time.

“They felt that with their expertise that they could prolong the remaining life, which is exactly what they did up until they shut it down,” Blind said.

Entergy closed Palisades in May 2022 and sold the plant to Holtec to take over its dismantling. But Michigan Gov. Gretchen Whitmer in a letter to the Department of Energy pushed to keep Palisades open, citing the jobs supported by the plant and the need for reliable, carbon-free power. Backed by the governor’s office, Holtec first applied for federal support to restart Palisades two months after it closed.

Indian Point leak

A steam generator tube rupture at the Indian Point nuclear plant — located 24 miles north of New York City in Westchester County, New York — demonstrates the potential risks such incidents pose to public health and the finances of utility companies.

On Feb. 15, 2000, operators at Indian Point Unit 2 received a notification that a steam generator tube had failed, according to the NRC’s report on the incident. Consolidated Edison issued an alert and shut the plant down, the regulator said. It would stay closed for 11 months while the cause of the rupture was investigated and the condition of the four steam generators was analyzed.

The rupture resulted in “a minor radiological release to the environment that was well within regulatory limits,” according to an NRC task force report. The incident “did not impact the public health and safety,” according to the report. Still, the NRC slapped Con Edison with a red citation, the most serious violation, after determining the leak was of “high safety significance.”

The leak was contained and there was no evacuation of neighboring communities, but authorities in Westchester County at the time were deeply worried about the risk to the public, said Blind, who was Con Edison’s vice president of nuclear power at Indian Point during the incident.

Inside the Palisades nuclear power plant in Covert, Michigan, Feb. 24, 2025.

Spencer Kimball | CNBC

“We had contained all of the radioactive water, but they were so scared that they were very close to closing all the schools,” said Blind. “They weren’t going to let the children come to school in the morning until they saw how this all played out. It’s all very serious.”

The leak proved costly for Con Edison. The utility replaced the four steam generators at an estimated cost of up to $150 million, according to company filings from the time. The bill would have been higher had Con Edison not had replacement steam generators already on hand. The utility had owned replacement generators since 1988 but had not installed them. Con Edison also paid more than $130 million in charges associated with the 11-month outage at the plant.

Blind said Con Edison decided to replace the steam generators at Indian Point to reduce the risk that there would be another tube rupture when the plant restarted.

“We were a publicly traded company,” Blind said. “And it came down from the board, it said we can’t live with this uncertainty.”

The utility sold Indian Point Units 1 and 2 to Entergy for $502 million in 2001 under a deal that also included gas turbine assets. The sale was under consideration before the tube rupture. Con Edison estimated an after-tax loss of $170 million from the Indian Point sale, according to filings from the time.

Blind said the stakes of the planned Palisades restart are high for the entire nuclear industry. Demand for nuclear power is growing again in the U.S. as states, utilities and the tech sector seek more reliable, carbon-free power. The renewed interest has been referred to as a “nuclear renaissance” after years of reactor shutdowns in the U.S.

Constellation Energy, for example, is planning to restart its Three Mile Island plant in 2028 subject to NRC approval. Constellation has said the steam generators at the plant have undergone inspection and maintenance and are in good condition. NextEra Energyannounced in July 2024 that it is evaluating whether restarting its Duane Arnold plant in Iowa is feasible.

An incident at Palisades “would be devastating for the entire industry,” Blind said. “There would be calls for rethinking this renaissance idea,” he said.

Holtec’s Culp said the sleeves used to repair the steam generators at Palisades will be continuously monitored, inspected and subject to regulatory oversight while they are in service. The plant employs multiple layers of defense “to protect our workforce, community, and environment,” he said.

NRC inspectors will observe Holtec’s repair activities as they are implemented and will ensure the steam generators meet all the requirements for safe operation, Burnell said. “This includes making sure that the public and the environment are protected from radiological concerns,” the NRC spokesman said.

Alphabet (NASDAQ:GOOGL) shares are on my watchlist. The stock’s fallen 11% over the past month and even more from its early February highs. Because of this dip, the stock’s one-year performance is now just 10%.

As such, £10,000 invested a year ago would now be worth just under £11,000. That’s also factoring in the fact that Alphabet shares are denominated in dollars and the pound has appreciated slightly over the past year.

Clearly, this isn’t a bad return. However, while Alphabet lacks the sparkle of some of its mega-cap, big tech peers, I’m starting to wonder if it’s a little overlooked.

What the data tells us

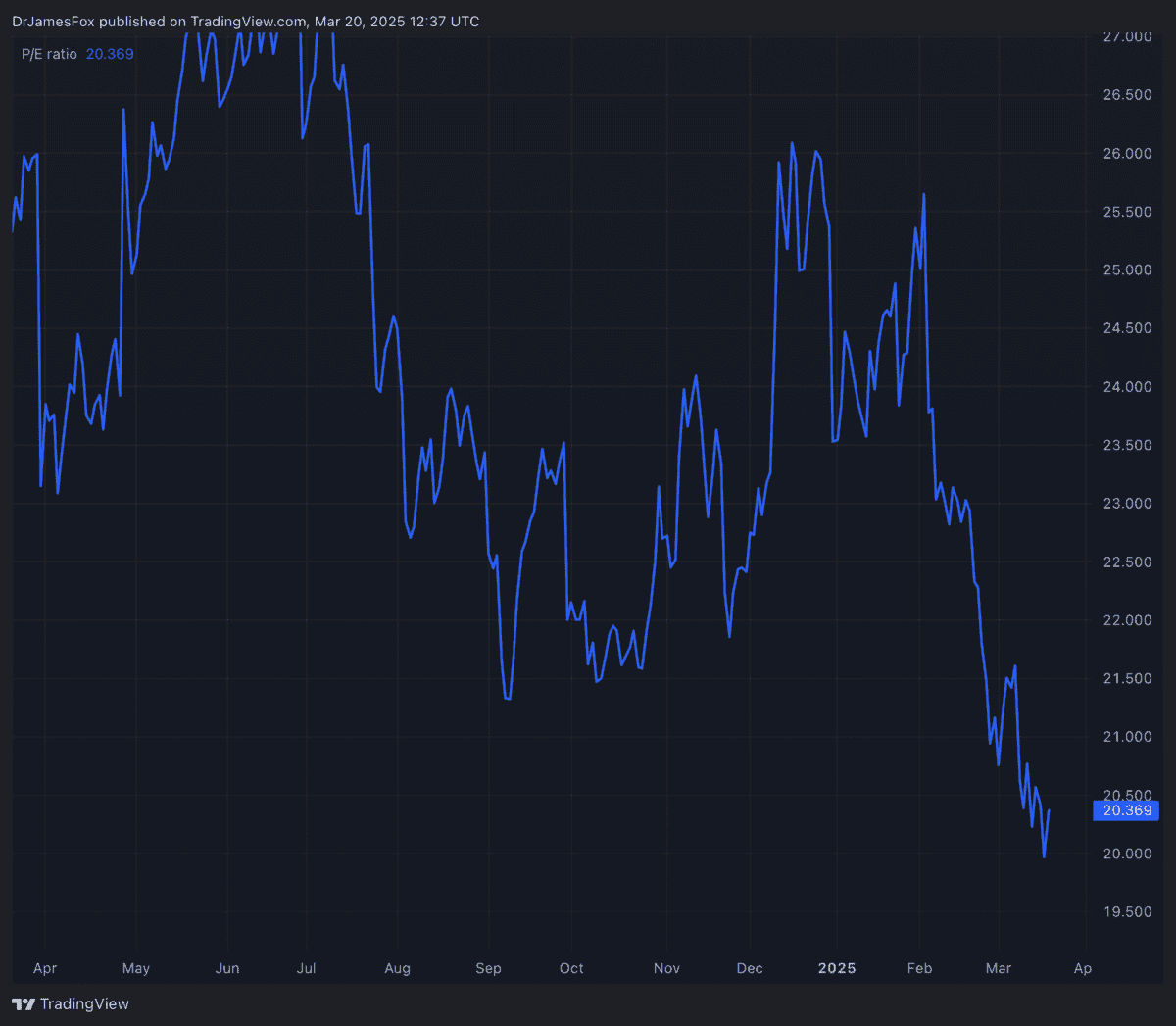

Let’s start with the boring but most important part. In terms of valuation, Alphabet’s forward price-to-earnings (P/E) ratio is 18.3 times, which does represent a significant premium to the communication services sector average (13.3 times), but a discount to the information technology sector average (21.8 times).

It’s also the cheap ‘Magnificent Seven’ stock, based on the forward P/E ratio. The closest peer is Meta,at 23.5 times.

Source: TradingView — Google’s falling P/E (TradingView data may differ slightly from the data presented above)

Alphabet’s price-to-earnings-to-growth (PEG) ratio is also a key sign of an undervalued stock. Currently, Alphabet’s PEG ratio stands at 1.10, which is lower than the communication service sector median of 1.27 and information technology sector 1.67. The metric’s achieved by dividing the forward P/E ratio (18.3) by the expected earnings growth rate. Interestingly, this is also the second-cheapest PEG ratio among the Magnificent Seven, with the exception of Nvidia.

This combination of a solid cash position, manageable debt, and attractive valuation is certainly appealing to me. Alphabet has $95.6bn in cash, though its recent purchase of Wiz might have slightly reduced this. Total debt current sits at $28.1bn.

Catalysts and risks

Alphabet’s a tech giant with its business strength coming from its dominant position in digital advertising. It controls more that 90% of the search market share, and continues to see growth is YouTube and Google Cloud. Collectively, its diversified revenue streams, including cloud services and hardware, provide stability amid sector shifts.

Catalysts include Waymo’s expansion, including key markets like Tokyo and Silicon Valley, marking its first international foray and scaling autonomous ride-hailing services. Partnerships with Uber and plans to increase rides from 200,000+ a week highlight near-term growth potential.

Long-term prospects include the business’s investments in quantum computing. Alphabet’s Willow processor recently demonstrated breakthroughs in error reduction and processing speed, though commercialisation remains years away. And while there are plenty of small competitors in this sector, I’m backing a mega-cap stock like Alphabet to be the first to commercialise the technology.

However, risks loom from regulatory scrutiny (antitrust cases), artificial intelligence (AI) competition and high capital expenditure, which could put pressure on profitability. What’s more, Google Cloud’s slower-than-expected growth and quantum computing’s unproven practicality add uncertainty as we look further into the future. Tesla will also be a major competitor in autonomous ride-hailing when it catches up.

Nonetheless, I’m still considering adding this stock to my portfolio. In addition to the above, the Relative Strength Index — a technical indicator that measures share price movements — suggests the stock’s close to ‘oversold’ territory.

As a long-term investor, I like the timeframe of decades I have in which to invest my Self-Invested Personal Pension (SIPP).

But while time can be the friend of the long-term investor, it can also multiply the cost of some mistakes.

For example, a small-seeming annual charge or account management fee can suddenly look big when taking a 20- or 30-year view.

Here are three things I think an investor should look for when finding shares to buy for their SIPP, to try and help time be their friend rather than their enemy.

1. Ongoing business relevance

Times change – and so do industrial and consumer needs. Once-mighty businesses fade away.

If you doubt that, just have a look at the some of the companies that have featured in the FTSE 100 over the past four decades.

PC maker Amstrad? Paper miller Arjo Wiggins Appleton? Trident jet manufacturer Hawker Siddeley?

None now exist as independent companies.

But other businesses that have been in the FTSE 100 from day one do, including J Sainsbury, Shell, and Unilever (LSE: ULVR).

Predicting long-term business trends can be difficult. But some areas (like food retail and energy provision) are likely here to stay for the long term one way or the other, I reckon.

So when buying shares for a SIPP, I think a savvy investor will ask whether their target share’s business area looks likely to endure over the long run.

2. A sustainably great business needs a competitive advantage

But just because a business area endures, that does not mean that specific firms will hang around.

To differentiate itself from rivals, a business needs some form of competitive advantage.

I think Unilever is a good example here.

It owns a range of premium brands like Hellmann’s and Dove that help set its products apart from unbranded rivals. It also owns unique products such as Marmite as well as having developed proprietary product formulations and having a huge global distribution network.

That does not necessarily mean it is a consistently strong business, by the way. Ingredient inflation can eat into profit margins while having three chief executives in under two years could mean that business performance in coming months and years is unsettled.

Indeed, while I would happily buy Unilever shares for my SIPP at the right price, for now the company is too pricey for my tastes given such risks.

But the company does illustrate in bucketloads something I look for when finding shares to buy for my SIPP: a sustainable competitive advantage.

3. Valuation, valuation, valuation

It may seem surprising that I am unwilling to buy Unilever shares even though I like the company.

But most people would not buy a car or home they liked if they felt it was not attractively priced.

For me, it is the same with investing. A good business does not necessarily equate to a good investment. In fact, it can be a terrible one. It depends on what one pays to invest in it.

That is why, when assessing possible shares to buy, I always ask whether they are attractively valued.

Investing in shares that pay dividends is a common, practical way for people to earn passive income.

That does not mean it is easy. Dividends are never guaranteed and share prices can fall, so a smart investing approach matters. But without much effort, I think a realistic and sensible investor could build substantial passive income streams over time.

As an example, with a spare £20k, here is what an investor might be able to achieve while sticking to proven blue-chip companies from the top tier FTSE 100 index.

Investing smartly and realistically

Twenty grand is a good amount actually, as it easily allows an investor to diversify across a few different shares. That is a simple but important risk management principle and £20k could also typically be invested as one year’s ISA allowance. This year’s contribution deadline is just a fortnight away.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice. Readers are responsible for carrying out their own due diligence and for obtaining professional advice before making any investment decisions.

I think an investor would do well to follow other principles of good investment. It also makes sense to buy and hold shares using a suitable and cost-effective trading platform. So a good starting place would be to compare different share-dealing accounts and Stocks and Shares ISAs on the market.

Each investor is different and what works well for one may not be the best choice for another.

Finding shares to buy

I mentioned above the idea of buying a carefully-chosen variety of proven blue-chip businesses. I think it makes sense to do what billionaire investor Warren Buffett does and stick to what you know and understand. Again, that will differ from investor to investor.

To illustrate the approach I take, I could use one share in my portfolio: Legal & General (LSE: LGEN). It has a large market of potential and actual customers, thanks to its focus on retirement-linked investments.

Legal & General has a long heritage and long brand that ought to help it long into the future to attract and retain clients. It has a proven business model and a large customer base.

My main reason to own it is for passive income. It has raised its dividend annually over the past few years and plans to keep doing so, though dividends are never guaranteed. The sale of a large US business could mean smaller profits in future and that could hurt the dividend, for example.

Building towards an income target

At the moment, the share has a dividend yield of 8.8%. So every £100 invested now will hopefully earn £8.80 in dividends annually. That is well above the FTSE 100’s average yield of 3.5%.

Still, in today’s market I think an investor could realistically aim to achieve double that (7%) from the right portfolio of blue-chip dividend shares.

In one year, £20k invested at an average 7% yield ought to provide £1,400 of passive income. That is roughly £116 each month. By reinvesting those dividends (what is known as compounding) though, an investor could build a bigger portfolio – and passive income streams.

Compounding at 7% annually for two decades, an investor could turn a £20k portfolio into one worth over £77k. At a 7% yield, that ought to generate £451 a month of income.

It seems a while ago already that Tesla (NASDAQ: TSLA) was a darling growth stock, with a market capitalisation well north of a trillion dollars. Tesla stock has now lost over half its value from the high point it hit over the past 12 months. It has crashed 42% since the beginning of the year.

However, that still puts it 37% higher than just one year ago – and 729% up over a five-year period.

Back in 2020, Tesla was trading below $100 a share.

Could it get down there again – and if so, ought I to buy some for my portfolio?

Tesla’s growth has been phenomenal – but it may be over

A large part of what has spurred the Tesla stock price has been its outstanding growth story.

This has not merely been a prospect dangled in front of investors – it has been a large-scale business reality.

It has close to quadrupled since 2020, from a high base.

But last year’s growth of barely 1% was a step change compared to the prior years. It was also the first year when deliveries of Tesla cars declined rather than grew.

What about profit?

Last year net income was a beefy $7bn. But not only was that less than half the previous year’s number, it also represented an inflection point, as the chart turned from many years of growth to contraction.

There could be worse to come. An increasingly competitive electric vehicle market may hurt both sales volumes and profit margins. Add to that the potential impact of Tesla boss Elon Musk’s high-profile political activities and I see a risk that Tesla will report falling sales revenues and weaker profits this year.

That does not mean it is not still a solid business. But Tesla stock soared because investors loved the growth story. If that growth story is over, it could be bad news for the share price.

If it was to fall in line with the S&P 500 average P/E ratio of 28 (still hardly a bargain, in my view), that would mean Tesla stock losing just over 75% of its current value. That would take it down to around $57 apiece.

That is if – and I see it as a big if for the reasons I explained above – Tesla can even maintain earnings at last year’s level.

I’d like to invest, at the right price

Still, Tesla has confounded critics for years and may keep doing so.

The firm has a large following among investors, has built an incredible business at speed and could continue growing. It has a strong brand, large user base, and financially attractive vertically integrated manufacturing and sales model.

On top of that, its power generation business looks set to keep growing at pace.

I see a case for the price crashing well below $100. For now, I think Tesla stock still looks badly overvalued. But if it got cheap enough, I would happily start buying.

The potential gain from owning shares in Lloyds (LSE: LLOY) over the past year has been considerable. During the past 12 months, the Lloyds share price has moved up 36%.

On top of that, there is a dividend yield of 4.5%. Someone who bought the shares a year ago at the lower price however, would now be earning a yield of around 6%.

Still, with the Lloyds share price still in pennies, might there be further room for increase – and should I invest?

The price could rise again

To answer the first of those two questions, I do think the share could move even higher from here. The price-to-earnings ratio of 11 strikes me as reasonable, rather than overly expensive.

When it comes to valuing banks however, many investors prefer to use a price-to-book value ratio. Here, the picture is less attractive. Not only has the share become more expensive lately using this ratio, it now also looks potentially overvalued, as a ratio above 1 indicates that the share price is higher than the underlying book value.

So why do I think the Lloyds share price could still move higher from here? As the past year’s rally shows, many investors have continued to buy into the bank. With a proven business model, strong brands and large customer base in a market with high barriers to entry, I see a lot to like about Lloyds.

If it can maintain or improve its business performance, that could help justify a higher share price.

An ongoing share buyback programme should also push up both the earnings and book value per share, potentially justifying a higher share price for Lloyds.

Here’s why I’m not buying

Despite that however, I continue to avoid the share and have no plans to add Lloyds to my ISA or SIPP at the present time.

I recognise the bank’s strengths but see challenges from an uncertain economic outlook. Given Lloyds’ role as the country’s leading mortgage provider, that could eat into profits if loan defaults rise. There are also other risks, such as ongoing costs from a car financing mis-selling scandal.

Last year saw the bank’s post-tax profit fall by nearly a fifth. Yes, it was still a mammoth £4.5bn. But a fall on that scale does not fill me with confidence about the outlook for the business.

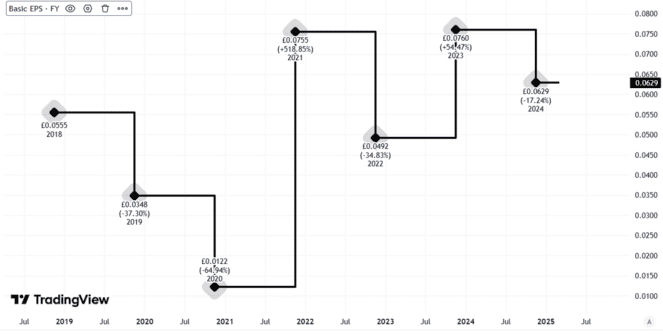

Despite share buybacks, the Black Horse Bank’s basic earnings per share have moved around in different directions over the past several years.

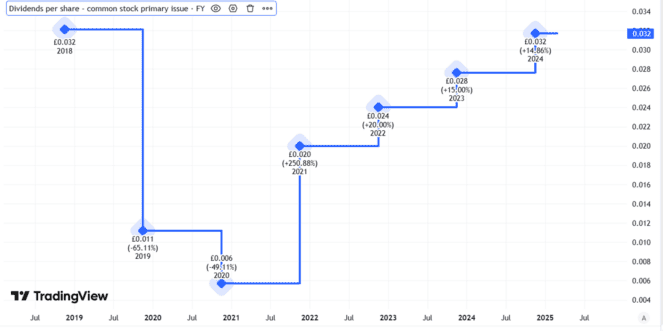

Those buybacks actually put me off investing, as I think the board would have done better to use spare cash to restore the dividend per share to its pre-pandemic level.

Instead, it has dragged its feet for years on this, making me think it does not fully appreciate the importance of the dividend to many investors.

So although I reckon the Lloyds share price may move higher still, I also have concerns about the risks of investing at the current level and have no plans to do so.

Penny stocks are known for their often eye-poppingly-low valuations. This reflects challenges like thin balance sheets, unproven business models, and competition from larger rivals.

It also reflects the volatility that small-cap shares often experience.

What they’re less famous for, however, is the presence of high dividend yields. This simply reflects the fact that younger companies tend to prioritise any spare capital they have to investing for growth rather than paying shareholders cash rewards.

However, the following penny shares are the exception, offering an attractive blend of value and dividends. And today their dividend yields sail comfortably above the 3.6% average for FTSE 100 shares.

Here’s why I think they’re worth serious consideration today.

HSS Hire

With a forward price-to-earnings (P/E) ratio of 7.7 times and 9.8% dividend yield, HSS Hire (LSE:HSS) offers attractive all-round value. Its cheapness reflects tough economic conditions in its markets, and by extension an uncertain profits outlook.

The penny stock is a prominent supplier of tool and equipment hire services in the UK and Ireland. Despite its position as market leader, continued weakness in the construction sector poses obvious dangers to shareholder returns.

Yet, for patient investors, I believe HSS shares could eventually prove a shrewd buy. It has major structural opportunities to exploit, such as government plans to build 1.5m new homes between now and 2029, and the fast-tracking of 150 major infrastructure projects.

In the meantime, HSS is extensively cutting costs to help it ride out current market difficulties.

Topps Tiles

Tile retailer Topps Tiles (LSE:TPT) shares many of the same qualities and problems as HSS.

Near-term earnings are under threat from difficult conditions in end markets. On top of this, the sector in which this penny stock operates is highly competitive.

Yet, like the tool hire giant, it also has significant long-term structural opportunities as Britain gets building again. And as market leader, it’s in the box seat to exploit any market upturn (it has 20% of the tile market).

For this fiscal year (to September 2025), its shares trade on a forward P/E ratio of 8.9 times. They also carry a market-beating 8% dividend yield.

Alternative Income REIT

Alternative Income REIT (LSE:AIRE) isn’t a conventional penny stock in that it prioritises dividend distribution over earnings growth. This reflects its status as a real estate investment trust (REIT).

Under REIT rules, at least 90% of yearly rental earnings must be paid out by way of dividends. For this financial year (ending June 2025), this means an 8.7% dividend yield.

With exposure to multiple sectors including healthcare, retail, residential, and industrial, Alternative Income’s diversified model provides stable earnings across the economic cycle.

It’s still vulnerable to interest rate movements that can push up borrowing costs and depress asset values. But I think this threat is more than baked into its rock-bottom valuation.

Today it trades at a 13.9% discount to its net asset value (NAV) per share.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice.

My Stocks and Shares ISA may be jam-packed with dividend-paying FTSE 100 stocks but that doesn’t mean that I shy away from investing in out-and-out growth businesses too. After enduring a couple of torrid years, I see one standout compelling growth story in the years ahead.

China uninvestable

Driving the narrative behind the poor share price performance of Prudential (LSE: PRU) is that China had become uninvestable. The delayed relaxation of Covid travel restrictions between the Chinese Mainland and Hong Kong undoubtedly hurt the Asian powerhouse economy.

On top of that the country’s bubble in real estate has been unwinding. This hurt domestic imports of commodities essential for a booming economy.

Given that nearly half of all its insurance profits are derived from China and Hong Kong, its little surprise that the share price has been falling. It’s down over 40% in two years.

Covid blues

The strong FY24 results released on Thursday (20 March) highlight that the sell off had been completely overdone. New business profit was up 11% to $3.1bn. But I believe this is just the beginning.

The markets in which the company operates are some of the fastest growing in the world. In both China and India, GDP is expected to grow by 5% in 2025.

A growing middle class is increasingly expecting access to what Western consumers take for granted. In particular, insurance and savings products.

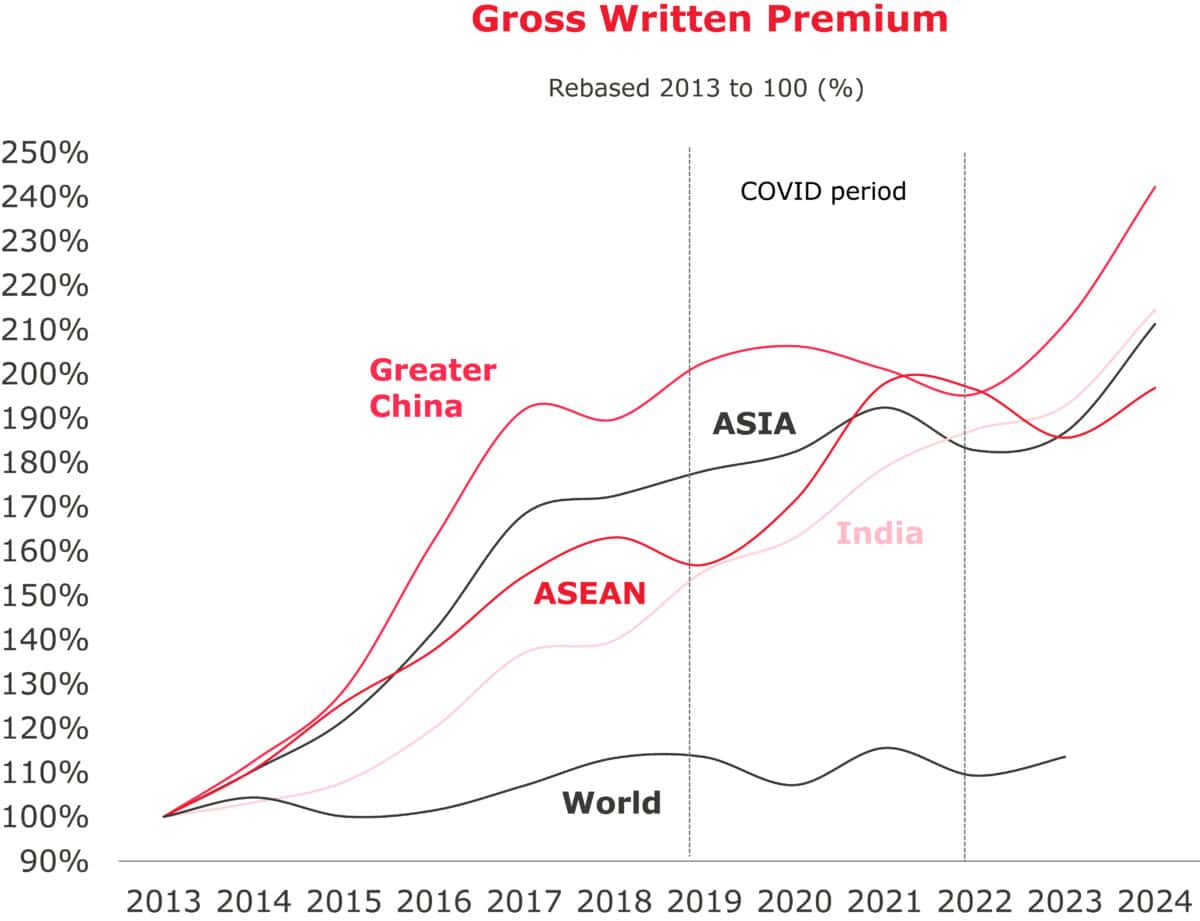

Times may have been tough for such consumers during Covid. However, the following chart highlights that gross written premiums in its core markets has now fully recovered.

Source: Prudential presentation

Structural growth drivers

The opportunity presented to it in the coming years is truly gargantuan. Out to 2033, the total addressable market in Asian life insurance gross written premiums is predicted to double to $1.6trn.

The drivers for this growth are varied. By 2040, 28% of China’s population will be over 60. Wealth creation across Asia is increasing too. Today, the region accounts for 30% of total global wealth creation. Third, are low insurance penetration rates. The gap in insurance coverage is estimated at a whopping $119trn in Asia.

I believe that it is well placed to capture a significant slice of this burgeoning market. Key for the business is it growing cohort of agents.

Selling insurance-related products is first and foremost a people business. Prudential has been working hard to recruit quality agents and train them in selling their products. Many of its agents are now members of the prestigious Million Dollar Round Table network.

Risks

Of course, there are plenty of risks here. All insurance businesses face ongoing credit and liquidity risks. Uncertain interest rate trajectories and increasing protectionism policies could affect underlying growth drivers. This is particularly acute in China where concerns about the long-term health of its property sector won’t go away.

But when I look at the bigger picture here, I think it makes for one of the most compelling growth stories in the FTSE 100. The hike in its dividend per share by 13% in FY24 highlights to me that management is very bullish too.

Beyond its growing dividend, it’s also in the middle of executing a $2bn share buyback programme. With all this, it’s little wonder I have been hoovering up Prudential shares lately while they remain cheap.

Financial News

Daily News on Investing, Personal Finance, Markets, and more!