When it comes to double-digit dividend yields, investors are often told to stay away as it’s usually a warning sign that something’s wrong. But there are some rare exceptions. And SDCL Energy Efficiency Income Trust (LSE:SEIT), also known as SEEIT, just released a trading update that not only confirmed it can afford its 14.2% yield but that it’s already on track to hit its sixth consecutive year of dividend hikes.

The last five years have been pretty rough for this enterprise, with the share price tumbling more than 50% – a trend that’s continued in 2025. That certainly helps explain why the yield’s so high today. But is there a reason why investors are jumping ship? Or is this secretly an exceptional income opportunity?

Investing in energy efficiency

There are a lot of different ways to invest in the energy sector. However, rather than being dependent on fluctuating oil prices, SEEIT offers a unique opportunity for investors to help boost the efficiency of energy infrastructure.

The firm owns a fairly diversified portfolio of projects scattered across the globe in technologies like solar & storage, district energy systems, gas distribution networks, electric vehicle charging, biomass, and industrial process efficiency solutions, among others.

Despite what the share price would suggest, the operational performance of the group’s flagship projects is actually quite encouraging.

For example, its Primary Energy segment, which provides energy services to US blast furnaces, is meeting earnings targets while also positioned to benefit from the new US tariffs as domestic steel production rises. At the same time, the Red-Rochester division, which specialises in district energy systems, is actually beating internal expectations. It’s a similar story for its Onyx business, which focuses on deploying on-site solar and storage solutions for commercial customers.

With all that in mind, why is the stock price falling?

Investigating the yield

Clean energy assets have been particularly unpopular among investors in recent years. Higher interest rates make these capital-intensive businesses less desirable. And it explains why other similar trusts like Greencoat UK Wind and Foresight Solar Fund have also suffered a share price decline.

This interest rate risk appears to be one of the primary concerns investors have regarding this enterprise. While the prospect of future tariffs may be beneficial for some of its projects, if the inflation they cause proves not to be transitory, interest rate cuts could be delayed and possibly reversed.

At the end of September 2024, SEEIT only generated £48m in free cash flow after debt servicing costs. That was enough to afford shareholder dividends, but the coverage ratio was pretty tight at 1.1. Should any disruption occur to cash flow generation, either internally or externally, today’s impressive dividend yield might end up getting cut.

The bottom line

For now, SEEIT’s 14% payout’s here to stay. But, there’s a significant risk of a dividend cut later in 2025 if the group’s operations are disrupted. Personally, this isn’t a risk I’m willing to take for my income portfolio. However, for investors comfortable with a higher risk dividend opportunity, this enterprise may be worth a closer look.

After a stellar finish to 2024, the S&P 500 seemed as if it was primed to continue surging in 2025. Yet following the announcement of worldwide tariffs, the US stock market has subsequently proceeded to plummet, with its flagship index down more than 15% since the start of the year and over 12% since the start of April. At least that was the case until last week when tariffs were delayed, and US stocks shot back up.

Year to date, the S&P 500 was still down almost 9% as of 11 April. However, ignoring the recent rebound, any investor who put £5,000 to work at the start of the year with an index fund would only have £4,250. And the situation was even worse for those who concentrated on the Magnificent 7. On an equal-weighted basis, shares of Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia (NASDAQ:NVDA), and Tesla crashed. They were down over 25%, taking a £5,000 initial investment all the way down to £3,750.

There’s no denying it was a painful start to the year, especially for newer investors. Yes, last week’s upward surge helped take some of the pain away. But plenty of S&P 500 stocks are still trading lower today compared to the start of the year.

Investing during volatility

When investing in a volatile environment, ensuring we have some dry powder is often a prudent move. Apart from providing some helpful savings during economic turmoil, this cash offers the flexibility. It can allow investors to start buying shares when prices are in freefall. After all, some of the biggest gains we can make are during a stock market crash.

Another handy tactic is keeping a list of top-notch stocks to buy once the share price looks more attractive. That way, investors don’t need to spend countless hours investigating opportunities when disaster strikes. By being prepared, there’s a lower risk of missing out on potentially lucrative investments.

US stocks to consider in 2025?

It’s impossible to know for certain when the latest round of volatility will reach its bottom. As such, deploying a dollar cost-averaging buying strategy is likely prudent. And one Mag 7 business that I’ve got my eye on in this market is Nvidia.

The GPU chip designer is proving to be the dominant business in the AI infrastructure landscape, with some phenomenal growth under its belt. And despite US economic concerns, spending on AI-accelerator chips is set to reach $315bn in 2025.

Semiconductors have been excluded from the announced US tariffs. While the same isn’t true for other raw materials that go into Nvidia products (like steel and aluminium), customers might still just pay the higher cost to get their hands on Nvidia hardware.

After its 30% tumble this year, Nvidia shares now trade at a forward price-to-earnings ratio of 21. That’s significantly cheaper than its historical average of 52. With that in mind, assuming that AI adoption doesn’t hit a wall, steadily drip-feeding capital into the S&P 500 stock might be an investment worth considering throughout 2025.

Despite being the UK’s flagship growth index, the FTSE 250 has notably underperformed over the last decade. Even when factoring in dividends, this collection of 250 UK stocks has delivered only a total gain of 34%.

Admittedly, this result is offset by the recent volatility in the financial markets. However, even ignoring the price fluctuations of April 2025, the FTSE 250’s gains are still only 47%. On an annualised basis, that translates to just 3.9%. That’s a massive slowdown compared to the long-term 11% historical return of the index.

That means anyone who invested £10,000 10 years ago would only have around £14,700 today. That’s compared to the £18,500 offered by the FTSE 100 over the same period. However, while the FTSE 250 as a whole has underperformed, the same can’t be said for all of its constituents.

A big winner

Over the last decade, there have been plenty of successful growth stories of FTSE 250 companies making it into the top 100 UK stocks by market cap. However, the one business that seems to have stolen the show is Diploma (LSE:DPLM).

Even after joining the growth index in 2011, the industrial products distribution company continued its upward momentum. And after 12 years of market cap expansion, the business was promoted in late 2023 to the FTSE 100.

Investors who held on throughout this journey were rewarded with some pretty staggering returns. In fact, assuming dividends paid were reinvested, the total return over the last decade from this stock sits at 340%! That’s an annualised rate of return of 15.9%, outpacing even the S&P 500’s 12% over the same period. And a £10,000 initial investment would now be worth £43,804.

Still worth buying today?

Looking at Diploma’s 2024 results, management’s guidance for 2025 appeared to be quite flat versus its historical performance. Specifically, it predicted organic revenue growth of 6%, with an extra 2% coming from acquisitions. Skip ahead to the first quarter of 2025, and the business seems to be outpacing these targets. Organic sales are up 7% and acquisitive sales have jumped 5% after currency exchange impacts.

Obviously, that’s an encouraging sign. Yet management’s guidance for the full year remained unchanged. With uncertainty surrounding US tariffs, Diploma is seemingly keeping its expectations conservative. That’s not entirely surprising given the impact these import taxes could have on its complex international supply chains.

Investors sighed in relief last week when President Trump announced a 90-day pause on its global tariffs (with the exception of China). That certainly created a welcome rebound in the stock market. But with the threat of 10% tariffs still on the horizon, potential disruptions to Diploma’s business continue to loom ahead.

Nevertheless, top-notch businesses have a habit of adapting to a shifting economic landscape. That’s why, despite this risk, I remain optimistic for the long run. That’s an opinion seemingly shared by most analysts tracking this enterprise, which currently has an average 12-month share price target of 5,100p – 40% higher than current levels.

In other words, investors looking for fresh long-term growth opportunities in 2025 may want to consider buying Diploma. While past performance is no indicator of future returns, the now-FTSE 100 stock does have a habit of beating expectations.

The last 10 years have been quite eventful for the FTSE 100. The UK’s flagship index has gone through two major corrections in 2018 and 2022, along with two market crashes in 2020 and now 2025. Yet despite all this volatility, long-term investors have been rewarded with some notable gains.

When factoring in the additional returns from dividends, FTSE 100 index investors have reaped an 85% total gain. On an annualised basis, that’s the equivalent of 6.4% per year.

Compared to the S&P 500’s 182% gain over the same period, UK shares seem to have been left behind. Yet, it’s worth pointing out that volatility has been significantly lower here compared to the US. And these gains are still sufficient for a £10,000 initial investment to almost double to £18,500.

But what if instead of investing in a low-cost index fund, investors had bought individual large-cap stocks?

Explosive winners

While some have underperformed, despite being some of the largest London-listed companies, several other FTSE 100 stocks have vastly outperformed their parent index.

AstaZeneca’s steady stream of new drug approvals and portfolio expansion has delivered a total annualised return of 7.5%. At the same time, demand for RELX’s data collection has pushed up revenue and margins, resulting in an 11.8% average annualised return. However, it’s the actual company behind the UK stock market, the London Stock Exchange Group (LSE:LSEG), that’s stealing the show with a 15.4% annual gain!

To put this into perspective, £10,000 invested in the stock in April 2015 is now worth £41,995. And that might just be the tip of the iceberg. A newly signed partnership with Microsoft to bring the firm’s data and analytics tools to the cloud opens the door to new growth opportunities, including AI applications.

The expected long-term benefits of this 10-year deal are likely why analysts are overwhelmingly bullish on the future of this enterprise, with 17 out of 20 recommending the stock as either a Buy or Outperform.

Of course, with this deal being a big driver of expected future growth, the stock may be doomed to tumble if the benefits fail to materialise. This risk is only amplified by the elevated valuation today at a forward price-to-earnings ratio of 26.1, even after the recent stock market tumble. But I still feel it’s worth considering.

Not everyone is a winner

Picking stocks is a challenging process. And even the most promising ideas can fail to deliver on expectations. Shareholders of Ocado (LSE:OCDO) know this all too well. The troubles at the online grocery store turned robotics automation business has been so severe that it actually lost its FTSE 100 status back in 2021.

While Ocado shares were seemingly off to a great start, management’s decision to aggressively ramp up its investments in automated warehouse technology sent earnings plummeting into the red. And while peak capital expenditure is now finally in the rearview mirror, the share price is still around 25% lower than where it stood a decade ago.

Ocado’s story certainly isn’t over. And its latest results did reveal a welcome surge in underlying earnings and free cash flow – two steps in the right direction. However, it highlights the potential risk of investing in bad stock picks, even when looking at FTSE 100 companies.

By providing protection from wealth-sapping taxes, the Stocks and Shares ISA can substantially boost an investor’s chance to build a robust fund for retirement.

But how much would someone need to invest each month in a Stocks and Shares ISA to retire comfortably? Let’s take a look.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice. Readers are responsible for carrying out their own due diligence and for obtaining professional advice before making any investment decisions.

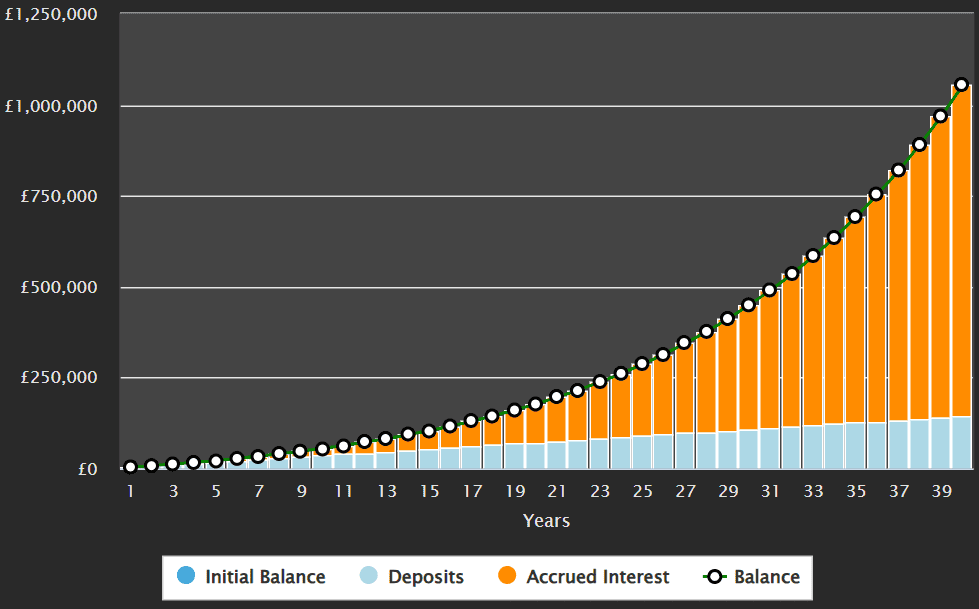

Compund returns

The first thing to say is the earlier someone gets started on their investment journey, the better. Time in the market allows for exponential growth through the power of compounding, which can turn even modest long-term contributions into a substantial retirement fund.

Let’s say someone has £100 to invest each month in their Stocks and Shares ISA. If they can achieve a 6% average annual return, here’s what their nest egg could look like by the State Pension age of 68, according to the date at which they began investing:

Age

Retirement pot(excluding broker fees)

25

£242,251

30

£174,426

35

£124,141

40

£86,863

45

£59,225

50

£38,735

As you can see, the differences are vast, illustrating the enormous effect of compound gains. Starting at 25 instead of 30 leads to nearly £68,000 more by retirement, just for beginning five years earlier.

The difference is even more striking when comparing a start age of 25 to 40. That’s a gap of around £155,000, despite contributing the same £100 each month.

Yet this isn’t to say that someone who starts investing later on can’t build a decent retirement fund. Even someone in middle age could conceivably retire in comfort with the right investment strategy.

A £51k passive income

It’s important to say that there’s no guaranteed return by investing in shares, trusts and funds. But history shows us that stock markets can be extremely effective way to target long-term wealth.

For instance, despite bouts of recent volatility, the average annual return of the FTSE 100 and S&P 500 indices over the last decade are 6.4% and 12.9% respectively.

Based on these figures, a 40-year-old who can invest £500 each month equally in these indices stands a good chance of achieving a Stocks and Shares ISA worth £854,877 by the time they reach 68.

If they then invested this in 6%-yielding dividend shares, they’d have a healthy £51,293 passive income to live off.

A top fund

There are many ways that investors can seek to build retirement capital, of which this is just one example. But a fund like the HSBC S&P 500 (LSE:HSPX) could be a good option to consider given the excellent long-term returns of US stocks that I’ve described.

Index funds like these provide excellent diversification across hundreds of companies, helping investors capture a multitude of opportunities while also allowing them to spread risk.

This particular fund holds high-growth shares like semiconductor maker Nvidia, online retailer Amazon and social media specialist Meta. Defensive shares such as telecoms provider Verizon, drinks manufacturer Coca-Cola and healthcare company Johnson & Johnson also provide steel.

It’s a combination that could deliver a blend of healthy capital gains, dividend income and long-term resilience.

A ramping up of global trade tariffs could well impact future returns. But US shares have a proven record of bouncing back from economic crises, which makes an S&P 500 fund a solid opportunity to think about.

Investing for a second income is a tricker task than usual right now. With the global economy facing significant challenges and uncertainties, it’s tough to predict how corporate earnings and investor dividends will hold up in the months and years ahead.

However, investors can lessen the chances of their passive income sinking by investing in a variety of different stocks. This can be achieved easily and cheaply by purchasing one or more dividend-paying exchange-traded funds (ETFs).

Some such funds are geared specicially towards paying high dividends. They can also hold companies that have strong records of dividend growth. By holding a basket of shares, ETFs can be a better way to target a dependable passive income over time, though it’s important to remember that dividends are never, ever guaranteed.

With this in mind, here are two dividend-paying ETFs I think are worth considering today.

A US-focused fund

As the name implies, the iShares US Equity High Income ETF (LSE:INCU) is geared towards generating income from North American assets (218 in total). For this financial year, its dividend yield’s huge, at 10.1%.

Perhaps surprisingly, it comprises a large section of tech stocks (including Nvidia, Microsoft and Apple). Around 28.3% of the fund is devoted to the information technology space.

But this iShares ETF holds classic defensive sectors, too, to give it added steel and exposure to higher dividend yields. Real estate, healthcare and telecoms also feature prominently.

In addition, the fund also generates income from US government-backed securities and cash. The BlackRock ICS US Treasury Fund’s the single largest holding here.

The ETF’s pure focus on US assets could leave it vulnerable if investor confidence in the States begins to dim. But right now, I still believe it offers decent diversification for dividend chasers.

X marks the spot

The Global X SuperDividend ETF (LSE:SDIP) holds 100 of some of the highest-yielding dividend stocks out there. As a consequence, its forward yield’s now 12.9%, which puts it in the top three largest-yielding ETFs.

In total, it has holdings in 105 businesses, which provides reslience even if one or two dividend shares deliver disappointing cash rewards. It’s also well diversified by geography — the US is its largest single territory by share exposure, comprising 30.5% of the fund. And its holdings span multiple sectors including financial services, mining, real estate and utilities.

Major holdings include satellite operator SES, food manufacturer Marfrig and telecom business Proximus.

GlobalX does have high weightings in cyclical industries. For instance, financial services companies and energy producers account for 27.5% and 23.6% of the fund respectively. This carries higher danger during economic downturns than ETFs that are focused on more defensive industries.

Yet the fund’s ability to deliver a large and constant stream of passive income during previous crises helps soothe any concerns I have. Its unbroken record of delivering monthly distributions dates back to 2012.

Investing in a mix of US and UK shares with a long-term outlook can be a road to a luxurious retirement. By sticking to a plan and dedicating a sizable amount of income each month, it’s possible to bring in considerable returns — and achieve generational wealth.

I know it’s an overused phrase but it’s worth repeating: the sooner one starts, the better. The miracle of compounding returns means there can be a huge difference between 20 years and 30 years. The snowball effect means the returns grow exponentially, with each extra year resulting in even more rapid growth.

However, that doesn’t mean it’s easy — or guaranteed. There’s a myriad of different geopolitical factors to consider that can send global markets soaring or tanking. At times, it can be a nerve-wracking experience that requires patience and dedication — but the reward may be worth the risk.

Let’s do some calculations.

The road to riches

The S&P 500 has returned 12% on average in the past decade, with dividends included. The FTSE 100 has returned only 6.3%. That suggests investors should focus purely on US stocks but a mix of both is a good way to protect a portfolio against a market downturn in one region.

It’s realistic to assume a well-balanced portfolio of UK and US stocks could return 8% on average. A monthly investment of £300 into an 8% portfolio could grow to £177,884 in 20 years. Keep going for another 20 years and the compounding returns would bring the total up to £1,054,284.

That’s a long time but if a dedicated investor started at 30, they could reach it soon after retirement. Even a late starter at 40 could reach almost half a million in 30 years.

Created on thecalculatorsite.com

Top UK growth stocks

The S&P 500 may have hosted some impressive growth stocks in recent years but the FTSE 100 shouldn’t be ignored. Stocks like Games Workshop and Alpha Group have enjoyed spectacular growth in recent years.

However, I’m more partial to well-established companies with proven track records of long-term growth potential. One that I think UK investors should consider is 3i Group (LSE: III), an international investment company primarily focused on private equity and infrastructure.

Its portfolio includes stable, cash-generating businesses that support consistent dividend payments. Its flagship holding, Action, is a European discount retailer that has delivered exceptional growth.

The stock has steadily increased from 460p per share to 3,874p. That’s a 742% increase, representing an annualised growth of 11.2% per year.

It’s dividend growth is even more impressive, increasing a compound annual rate of 32% over the past 15 years. That shows strong dedication to returning value to shareholders.

However, there are drawbacks to consider. As a private equity firm, 3i’s earnings can be volatile and closely tied to economic cycles. Performance fees and asset valuations fluctuate with market sentiment, which can impact dividend stability. Additionally, its reliance on a few key assets, like Action, introduces concentration risk.

Still, the company has consistently delivered strong performance, reflected in its rising net asset value (NAV) and growing dividends. Its investment in infrastructure, especially, provides reliable income over time, making it appealing to passive income seekers.

Last week saw the dawn of another tax year and with it, for many investors, a brand new ISA allowance.

A lot of attention gets paid to the £20,000 maximum annual contribution many people can make to an ISA. But of course not everyone has a spare £20k lying around – or anything near it.

The good news is that that is just a maximum. It is possible to start investing in an ISA with far less.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice. Readers are responsible for carrying out their own due diligence and for obtaining professional advice before making any investment decisions.

Putting £800 to work

I reckon £800 is ample to get going.

For example, an important though simple principle of risk management for stock market investors is diversification. That basically means not putting all of your eggs in one basket.

Another consideration is whether fees and costs will eat up a disproportionately high percentage of an ISA. I think £800 is enough that that need not be the case, though to try and avoid that risk it makes sense for an investor to compare different Stocks and Shares ISAs to see what one suits their needs best.

Setting an objective

Different people have different goals when they invest.

For some, earning passive income in the form of dividends is the name of the game. For others, buying shares that look undervalued and holding them for the long term in the hope of serious share price gain is what they want. Some investors aim for both dividends and share price growth at once.

Even with £800 I think it makes sense to get clear about objectives and then make investment choices based on that.

Finding shares to buy

Having an objective is one thing – how about bringing it to life?

The recent stock market turbulence has thrown up some potentially excellent buying opportunities for an ISA in my opinion.

But it can be an unnerving time for any investor, let alone a new one. Sticking to an area one understands makes sense. Rather than just comparing the price of a share now to what it was before, I think the approach is the same as a savvy investor always uses: looking for shares that are priced well below what the business outlook suggests they ought to be worth over the long run.

One share to consider

As an example, one share I think investors should consider for an ISA at the moment is Scottish Mortgage Trust (LSE: SMT).

This is an investment trust, meaning it holds stakes in a variety of different companies. So it can offer some level of diversification even to an investor with just a few hundred pounds to spare. It can also buy stakes in private companies that do not typically sell shares to small private investors. For example, Scottish Mortgage has a stake in rocket company SpaceX.

Scottish Mortgage shares have moved around a lot over recent months due to the trust’s large exposure to tech shares like Nvidia and ASML. With the tech sector still reeling from US tariff uncertainty and cooling investor enthusiasm, I see a risk that that will hurt the net asset value of Scottish Mortgage further – and its share price.

I see investing as a long-term activity, however. Scottish Mortgage has a proven ability to find tech winners early on.

It has been a simply wild week for Tesla (NASDAQ: TSLA) on the stock market, with price swings that would be unusual for a much smaller company let alone one with its market capitalisation. I have long wanted to buy some Tesla stock for my portfolio if I could do so at a price that I felt was attractive, so have been waiting for such a moment.

For now, though, I have not made a move.

I continue to think Tesla is badly overvalued. As an investor, however, I try to see both sides of a situation. After all, a market is composed of both buyers and sellers at the same time.

As part of that, here are three reasons that could suggest Tesla stock may be a long-term bargain – and why I do not find them persuasive at the current price level.

1. Potentially enormous end markets

The basic way to think about a company’s prospective future sales is to consider how big its target markets are and what sort of share of those markets.

Tesla is already huge when it comes to sales. Last year, it reported $98bn in revenues.

The end market potential is enormous. Cars alone make for a large market, but Tesla has ambition to extend into other types of vehicles, from lorries to what are basically minibuses.

It also wants to extend into offering automated taxis. Taxi provision is another big market.

On top of that, Tesla has a fast-growing business in power generation. That market is vast and also resilient.

As if that was not enough, Tesla plans to compete in robotics.

2. Tesla has a lot of competitive advantages

Recently, a lot of investors have focussed on some of the risks Tesla faces.

Its chief executive’s high political profile could put off some customers. Tax credits in key markets could come to an end. The electric vehicle market has become much more competitive, leading to pressure on profit margins across the industry.

Those risks are all real in my opinion – and significant.

But risk is part of business and Tesla has long proven that it can navigate challenging commercial environments.

As well as risks, it benefits from a range of competitive advantages that might help it grow market share in those large end markets I mentioned above – something it has been doing in power generation recently.

Its high profile helps build awareness of the brand at low cost. It has deep expertise in automotive software, power storage, vertically integrated manufacturing, and a host of other areas. If it can convert its competitive advantages to profits, that could be good news for Tesla.

3. Proven earnings growth capability

For now, the price of Tesla stock puts me off buying. The price-to-earnings ratio of 124 is far too high for my tastes.

The risks I mentioned above could mean Tesla’s earnings fall sharply again, as they did last year.

But what if they go the other way? Not necessarily soon but in, say, five or 10 years?

Tesla went from being a heavily loss-making company for years to one that turned an annual profit in the billions of dollars. If it can grow its earnings enough in the long term, today’s stock price could turn out to be a bargain.

Igor Golovniov | SOPA Images | Lightrocket | Getty Images

The chaos around tariffs continues to rattle global stock markets, as fears of higher costs and concerns over a potential economic slowdown weigh on investor sentiment.

However, the pullback in several stocks due to these ongoing challenges has created an opportunity to pick attractive stocks trading at compelling levels. Top Wall Street analysts can help identify stocks that could navigate short-term headwinds and deliver solid returns over the long term.

With that in mind, here are three stocks favored by the Street’s top pros, according to TipRanks, a platform that ranks analysts based on their past performance.

Affirm Holdings

We start this week with Affirm Holdings (AFRM), a buy now, pay later (BNPL) platform. As of the end of 2024, Affirm had 21 million active customers and 337,000 active merchants.

On April 7, TD Cowen analyst Moshe Orenbuch initiated coverage of Affirm stock with a buy rating and a price target of $50, reflecting a valuation of about 23-times the 2026 adjusted earnings per share. “AFRM is one of the top performing BNPL brands in the U.S. with a full-suite [point of sale] lending capability vs peers, and likely the most pro-consumer practices in the industry,” said the analyst.

Orenbuch thinks that AFRM possesses more seasoned underwriting capabilities than its rivals, as the company began underwriting longer-term loans before offering BNPL solutions.

The analyst also highlighted the company’s partnerships with big e-commerce players like Amazon and Shopify. Orenbuch contends that these key partnerships reflect Affirm’s capabilities while allowing it to pursue higher volumes from both big and small businesses more effectively than other BNPL players. Additionally, he pointed out that Affirm has a strong funding program that has historically helped it secure better terms in the capital market compared to others in the consumer lending industry.

Orenbuch added that AFRM fared better than nonprime lenders in the tough credit period in 2022-2023. He contends that even if gross merchandise value growth slows down over the short term due to weakness in the job market, it will have a short-term impact on AFRM’s profits and likely not weigh on its long-term profitability trajectory.

Orenbuch ranks No.22 among more than 9,300 analysts tracked by TipRanks. His ratings have been profitable 64% of the time, delivering an average return of 19.4%. See Affirm Holdings Stock Charts on TipRanks.

TJX Companies

This week’s second stock pick is TJX Companies (TJX), an off-price retailer that operates more than 5,000 stores across nine countries, including the TJ Maxx, Marshalls, HomeGoods, Homesense, and Sierra stores in the U.S. TJX and other off-price retailers sell merchandise at deep discounts compared to prices offered on comparable merchandise by department stores or other retailers, as they opportunistically purchase their inventory at lower costs.

Recently, Jefferies analyst Corey Tarlowe reaffirmed a buy rating on TJX stock with a price target of $150. The analyst stated that Jefferies’ updated “Inventory Insanity” analysis following the fourth-quarter results revealed that inventory rose 2.9% year over year across the firm’s coverage group of 85 companies compared to 2.2% in Q3 2024. Tarlowe thinks that TJX Companies is the best positioned in the off-price space to take advantage of the surplus inventory in the marketplace.

“Therefore, with an experienced team of +1.3k buyers, we believe TJX should witness and outsized benefit from continuing to buy opportunistically across its +21k vendors and more than 100 countries,” the analyst said.

Moreover, Tarlowe expects TJX to gain from the secular shift towards the off-price sector, which could help the retailer grab market share from other, more traditional retailers. The analyst also sees the company’s further expansion in the Home category and overseas markets as unique growth opportunities.

Tarlowe noted that TJX delivered a peak gross margin of 30.6% in fiscal 2025 despite an unfavorable comparison with the previous year, which included a 53rd week (due to a leap year). He thinks that management’s fiscal 2026 gross margin guidance of 30.4% to 30.5% seems conservative, especially given that the company exceeded its fiscal 2025 margin outlook.

Tarlowe ranks No.574 among more than 9,300 analysts tracked by TipRanks. His ratings have been successful 55% of the time, delivering an average return of 10.2%. See TJX Companies Insider Trading Activity on TipRanks.

CyberArk Software

Finally, let’s look at CyberArk Software (CYBR), a cybersecurity company that specializes in identity security solutions. The company is scheduled to announce its first-quarter results on May 13.

Heading into the Q1 2025 results, TD Cowen analyst Shaul Eyal reiterated a buy rating on CYBR stock with a price target of $450. The analyst thinks that CyberArk is well-positioned to navigate the challenging market conditions and surpass the Street’s revenue estimate. Eyal’s optimism is backed by checks by his firm that indicated continued strength in demand, with CYBR’s effort to expand its platform away from its core privileged access management gaining traction among customers.

Additionally, Eyal noted that despite increasing global macro challenges, value-added resellers, consultants, and partners are not seeing any slowdown in the second-quarter pipeline. He cited some of the key reasons for CYBR’s consistent performance, including its Identity and Access Management’s mission criticality and the persistent attack on digital identities by hackers. Also, rival SailPoint’s recent results and outlook didn’t indicate any slowdown, which bodes well for CyberArk as both companies are targeting similar market tiers.

Eyal sees the possibility of CyberArk revising the mid-point of its fiscal 2025 revenue guidance higher as the year progresses. Nevertheless, he contends that even if the company reiterates its guidance despite a possible Q1 2025 beat, it will still be viewed positively, given the growing macro challenges.

The analyst also highlighted CYBR’s efforts to expand its platform through strategic acquisitions like that of Zilla, which offers identity governance and administration solutions, and Venafi, which provides machine identity solutions. He continues to see a huge opportunity for CyberArk in the Agentic AI market.

“CYBR is executing well and remains well positioned to achieve its LT FY28 targets of $2.2B in rev and $600M of FCF [free cash flow],” said Eyal.

Eyal ranks No.14 among more than 9,300 analysts tracked by TipRanks. His ratings have been successful 64% of the time, delivering an average return of 22.5%. See CyberArk Ownership Structure on TipRanks.

Financial News

Daily News on Investing, Personal Finance, Markets, and more!