ISA millionaires love Legal & General shares – and so do I!

I was surprised to learn that Legal & General (LSE: LGEN) shares were the number one stock purchase among ISA millionaires in 2025.

Shares in the FTSE 100 insurer and asset manager seem an unlikely winner of a popularity contest, having slumped 23% over five years and 8% over 12 months. Yet I’m glad they’re in demand, because I hold them too.

We can assume that Stocks and Shares ISA investors who’ve hit millionaire status know what they’re doing. Kate Marshall, lead investment analyst at Hargreaves Lansdown, which compiled the figures, thinks so.

This FTSE 100 stock is a millionaire maker

She said that while some invest hoping to get rich quick, “the vast majority have built their fortune through the far more reliable approach of getting rich slow”.

Marshall said most don’t take enormous risks but “consistently invest as much as possible of their annual allowance, as early as possible in the tax year, in a diverse and balanced portfolio. And they’ve done this every year for decades”.

That’s very much our philosophy at The Motley Fool.

When it comes to Legal & General, I know what these investors are up to, because I’ve been doing it myself.

I bought its shares three times over the last 18 months, precisely because they’d fallen. This allowed me to get in at a good valuation and grab a higher yield. Now I plan to hold it for years, ideally decades.

Legal & General operates in a highly competitive corner of the market. It’s also a mature sector, where growth opportunities are limited. I don’t expect the share price to go bananas. There may be periods when it drives me bananas.

However, in the long run, I expect it to deliver a tasty combination of dividend income and share price growth. Mostly, though, it’s about the dividends.

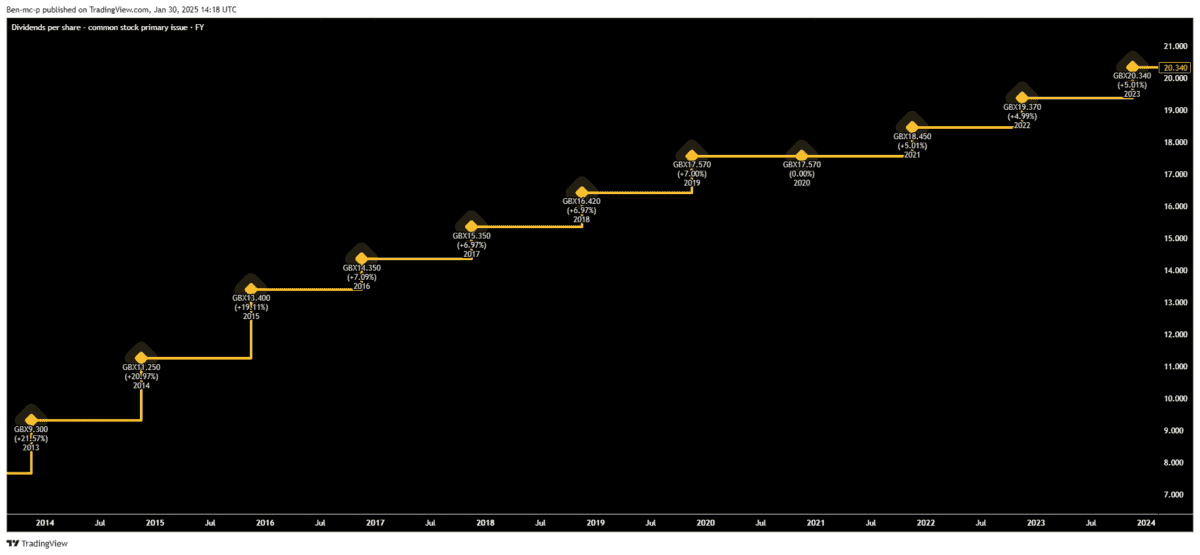

Legal & General now has a blockbuster trailing yield of 8.7%. Analysts forecast it to climb even higher, to 9.1% in the year ahead and 9.3% the year after.

Like most FTSE 100 companies, Legal & General rewards loyal investors by increasing shareholder payouts year after year. To do that, it needs to generate plenty of cash.

It’s a brilliant income stream

Worryingly, the forward dividend is covered only 1.1 times by earnings, whereas I’d prefer it to be covered twice. The board expects to generate up to £6bn of capital by 2027, which should support payouts, but there are no guarantees.

My shares have climbed a meagre 4.5% since I bought them. Yet, when dividends are included, my total return is almost 17%. And these are still early days.

I received my last payment on 17 September. The next is due on 5 June. I should get another before the year is out. I’ll reinvest every penny, building my stake. That will buy me more shares, which will pay me still more dividends.

If the current yield holds, I could double my money in around eight years, even if the shares don’t rise at all. And if they do, well that’s a bonus.

Sadly, I don’t think I’ll ever achieve ISA millionaire status. But it’s good to know I’m thinking along the right lines.