Here’s why I’m buying FTSE 100 shares not S&P 500 stocks

The S&P 500 index of leading US companies includes some that have seen massive success in the past few years, from Nvidia to Apple.

I owned Apple shares several years ago and both it and Nvidia are on my shopping list if they become available again at what I think is an attractive valuation.

in recent months though, I have bought some FTSE 100 shares but not S&P 500 ones. Here’s why.

Buffett on the circle of competence

A basic but important consideration is that, like billionaire investor Warren Buffett, I think I can give myself the best chance of stock market success by sticking to what I know and understand. Buffett refers to it as a circle of competence.

I understand a fair bit of the US economy and do invest in some US stocks. But overall, I have a better handle on what is happening in the UK, so feel better able to spot some investment opportunities here.

Take JD Sports Fashion (LSE: JD) as an example. When it announced last year that it was taking over US rival Hibbett, I was already very familiar with JD — but had never heard of Hibbett.

Attractive valuations

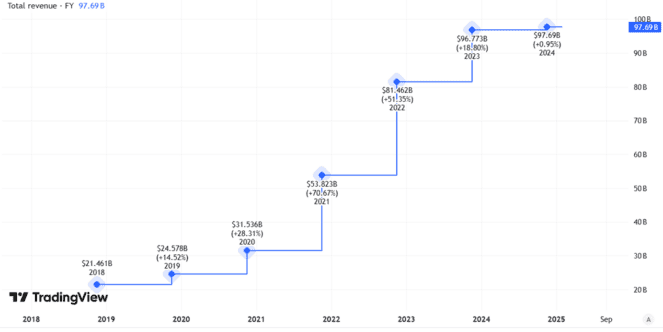

In fact, JD is one of the FTSE 100 shares I have been adding to my portfolio lately and I feel it is worth other investors doing further research into it too.

That may seem surprising. Its share price in the past five years tumbled 49%.

Nor is its yield of 1.1% even that attractive for a FTSE 100 firm.

The average yield in the blue-chip index right now is 3.6%, so the JD one is much closer to the S&P 500 average of 1.2%. While JD may not be a good illustration in this regard, juicy yields in general are also an attraction of many British over American shares to me at the moment.

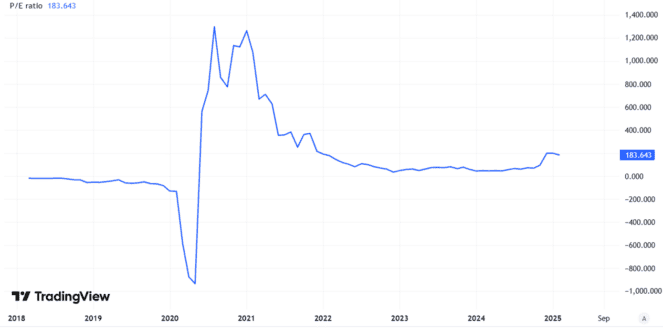

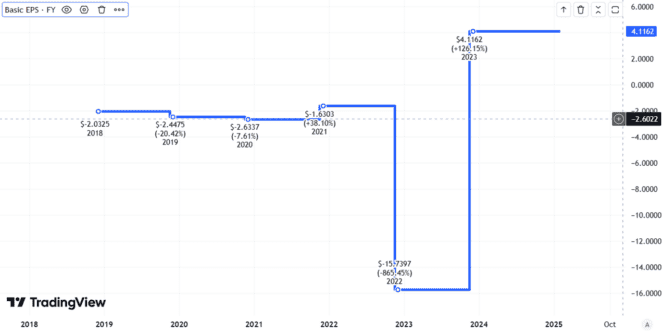

But the key attraction for JD as far as I am concerned is its valuation. That share price fall combined with long-term business growth means that it now trades on a price-to-earnings (P/E) ratio of 13. Knocking out exceptional items (JD is investing heavily in expanding its store network) the valuation looks even cheaper.

That is close to the average P/E ratio of FTSE 100 shares, currently at 15. That is half the S&P 500’s P/E ratio of 30.

I think that means British shares are much better value, but I could be wrong. If I buy a share that looks undervalued, the business may perform well but the valuation gap will not necessarily close (it could even get wider). A lot of investors prefer to invest in the US than the UK at the moment.

Exchange rate risks

Another point I consider when buying shares is any exchange rate risk. If I bought an S&P 500 share today, I could see its (dollar) price grow but end up losing money when I sell if the exchange rate moves unfavourably.

The reverse could also happen though, and I might benefit from currency fluctuations.

On top of that, though a share like JD is denominated in sterling, a lot of its revenues are in US dollars since the Hibbett takeover and indeed other currencies. It also sources internationally so has exchange rate risk in its supply chain.