40 and no pension? Here’s what £400 a month in a Stocks and Shares ISA could become

A Stocks and Shares ISA is a popular option for UK investors looking to build extra income for retirement. The tax-free allowance means investors can sink up to £20k per year into the account with no tax on the capital gains.

That’s probably a bit more than most people can afford to squirrel away each year. But no worries, even £400 a month can quickly add up to a lot due to the miracle of compounding returns.

Here’s one strategy a late but highly motivated investor could use to aim for a comfortable retirement.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice. Readers are responsible for carrying out their own due diligence and for obtaining professional advice before making any investment decisions.

Diversified risk

A self-directed ISA brings with it a certain level of responsibility regarding risk. Unlike a Cash ISA, the investor needs to navigate their own path to ensure positive growth.

However, the potential for higher returns is much greater. The key is to balance risk and reward. One way to do this is through a diversified mix of stocks, funds, and investment trusts.

Take Scottish Mortgage Investment Trust (LSE: SMT), for example. This highly diversified trust provides exposure to almost 100 stocks from a range of different countries.

Its core focus is on leading tech giants such as Nvidia, Meta, and TSMC. However, it’s also enthusiastic about global e-commerce, opting not only for popular choices like Amazon and Shopify but also smaller outfits like Sea Limited, DoorDash, and even private equity like Rappi.

Being heavily weighted towards US tech stocks is a moderate risk and one that’s resulted in volatility before. Since suffering a sharp drop in 2022, the fund has been trading at a discount to its net asset value (NAV). That means investors get exposure to all listed stocks at a price cheaper than buying them individually.

In February 1995, the shares were changing hands at a meagre 42p a pop. Fast-forward 30 years and they’re now valued at 1,087p. That equates to an annualised growth of 11.45%.

That’s somewhat higher than average for UK stocks. However, it’s realistic to aim for annual growth of 10% with a decent portfolio of stocks. After all, the FTSE 100 returned 9.5% last year.

Retirement goals

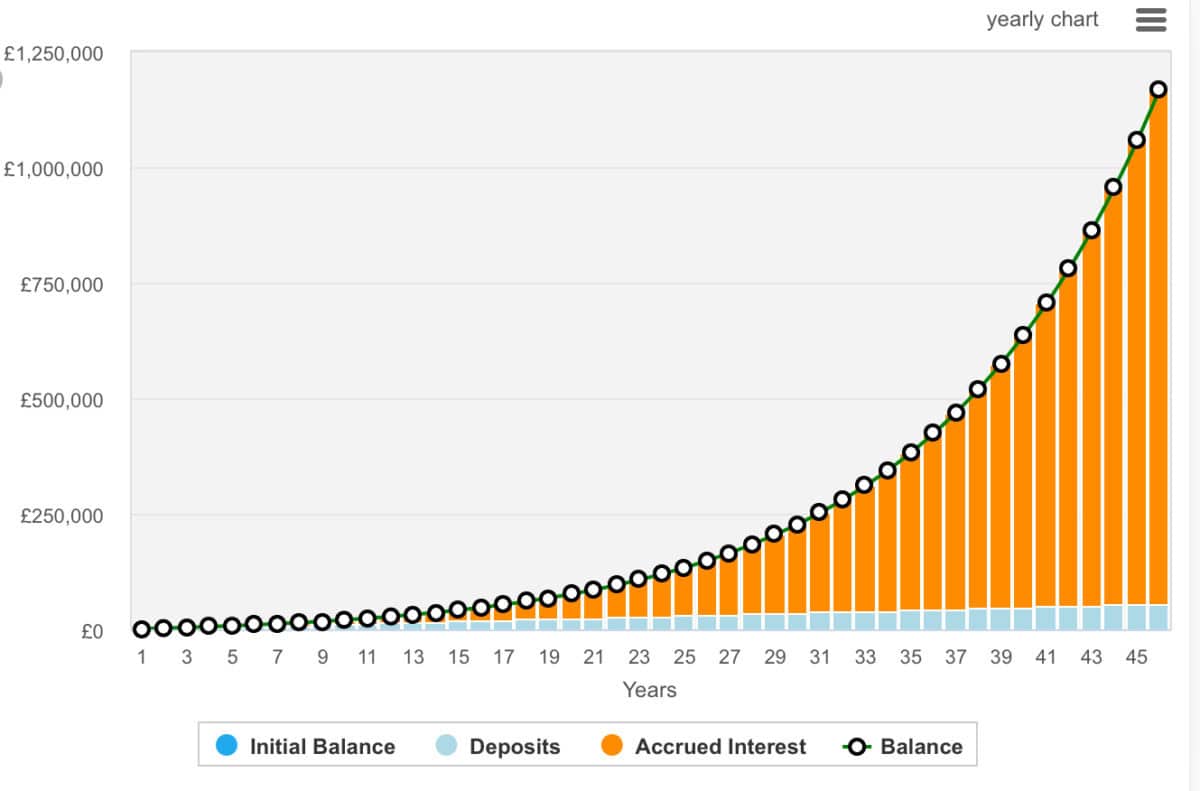

By investing £400 a month into an ISA with an average return of 10%, the pot could grow to over £535,000 in 25 years. That’s from only £120,000 invested (£400 x 12 x 25). At that point, the investor could begin drawing down approximately £53,500 a year — a sizeable pension pot to live off!

Even if performance tapered off to a below-average return of only 5%, it could still grow to nearly £240,000. In a strong portfolio of dividend stocks with an average 7% yield, that would return £16,800 a year.

Most likely, the final amount would fall somewhere in between these two extremes. In a standard rate Cash ISA, the pot would barely grow to above £200,000.

The above example shows how a lack of pension at 40 is not a life sentence. It’s never too late to start working towards a comfortable future. However, it will require a dedicated savings plan and a large monthly contribution.