Our monthly Ice Best Buys Now are designed to highlight our team’s three favourite, most timely Buys from our growing list of income-focused Ice recommendations, to help Fools build out their portfolios.

Data Centre electricity demand is forecast to double in four years, and electricity grids are one of the major bottlenecks of the energy transition. Meeting growing demand will require vast investments..

In December, National Grid submitted plans to invest up to £35bn in Britain’s electricity network over a five year period from April 2026. The plan would help develop and deliver major network reinforcement and expansion projects and the upgrade of around 3,500km of existing overhead lines.

We will see higher EPS growth in the long run from the company’s ambitious capital expenditure.

A significant portion of the growth will stem from alleviating constraints in the domestic grid. Capital expenditures on the high-voltage transmission network are expected to more than triple, driving a 10% annual increase in the asset base between 2025 and 2029.

Since 2021, National Grid has reshaped its portfolio to focus on electricity. CEO John Pettigrew expects the UK economy to be increasingly dependent on electricity with the growth of data centres and AI, as well as the higher domestic uptake of things like electric vehicles and heat pumps.

“Best Buys Now” Pick #2:

Redacted

Want All 3 “Best Buys Now” Picks? Enter Your Email Address!

According to data from AJ Bell and Hargreaves Lansdown, UK investors have been busy snapping up shares of Vodafone (LSE: VOD). Indeed, this was the most bought FTSE 100 stock on both platforms last week (based on the number of deals placed by customers).

Should I follow the crowd and invest too? Here are my thoughts.

Concerns

To form my decision, I’m going to look at a few key things. The first is the share price trend.

Now, this isn’t a dealbreaker one way or the other. But it does tell me whether investors have been bullish, bearish, or neutral on the stock.

Over the past year, Vodafone shares have been basically flat compared to the FTSE 100’s 13% rise. Over five years, Vodafone stock is down 57%.

I see a few obvious reasons why investors continue to be unconvinced here.

Firstly, Vodafone has not been growing. Revenue was €43.6bn in FY 2019, but only €36.7bn in FY 2024 (ended March). Looking ahead to FY 2026, the top line is expected to grow to €38.1bn.

Admittedly, the company has been actively divesting revenue-generating assets to streamline operations and focus on core markets. But the fact remains that overall growth has been disappointing.

Again, this doesn’t necessarily rule out the stock for me. I own shares of Legal & General and British American Tobacco for income, even though neither have been setting the world alight in terms of growth.

However, both firms have a tremendous record of increasing their payouts. In contrast, Vodafone’s dividend per share has gone from 9.24 euro cents per share in 2019 to a forecast 5.3 for 2025. That is expected to fall to 5.1 cents per share next year.

While that does put the forward dividend yield above 6%, the income prospects aren’t really tempting me.

Finally, there is the inescapable issue of debt. Building and operating telecoms infrastructure is notoriously capital-intensive. At the end of September, net debt was a hefty €31.8bn.

Even though that figure was down from €33.2bn in March 2024, the decrease was primarily driven by the €4.1bn sale of Vodafone Spain.

Some good bits

So why have investors been buying the shares en masse? Presumably it relates to the Vodafone UK-Three UK merger that was cleared in December.

This will create the UK’s largest mobile phone operator, with some 27m subscribers, and a plan to create one of Europe’s most advanced 5G networks. A new leadership team was announced last week for the future merged entity.

Perhaps these investors also turned bullish after the company’s recent Q3 results. Revenue increased 5% year on year to €9.8bn, with strong growth in Africa. And a mammoth €2bn has been earmarked for share buybacks following the €8bn sale of Vodafone Italy.

Meanwhile, the stock continues to look ultra-cheap, trading at just 10 times earnings. So there appears to be significant value on offer, at least on paper.

Should I invest?

Another worry I have though is that revenue is heading in the wrong direction in Vodafone’s key market of Germany.

Meanwhile, it is committed to investing £11bn to build out 5G in the UK. It could be a while before the benefits of that massive expenditure materialise.

Weighing things up, I’m going to give this value stock a miss.

For a mature FTSE 250 stock to have a double-digit percentage move in a day, something big is usually going on. So when I saw the news this morning regarding Assura (LSE:AGR), it naturally caught my attention. Here’s what investors need to know and what I’m thinking about doing from here.

The long story short

Before we get into things, let’s run through the story with Assura. The real-estate investment trust (REIT) has been performing poorly over the past few years. Even though the stock is only down 7% in the last year, it’s down 37% over the past three years. The decline can be linked to rising interest rates, higher borrowing costs, and weaker property valuations over this period.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice.

In part due to the low valuation, the business has attracted potential suitors to buy the firm. US private equity firm KKR has already made multiple takeover offers, which have been declined.

The latest offer, which was submitted last Thursday (13 February), valued Assura at approximately £1.56bn. This works out at roughly a 28% premium over Assura’s closing share price prior to the offer. Even with the premium, Assura’s board unanimously declined the proposal again today. The share price jumped when investors heard the news.

Why the share price bolted higher

With the rejection of an offer, some might expect the stock to fall. Yet when you think it through, the jump is warranted. When declining the offer, the board spoke about having confidence in the company’s long-term prospects and its ability to deliver value to shareholders. In other words, the management team feel they can get the business going again by themselves.

The fact that companies are offering to buy the business at a premium to the current price indicates that Assura is undervalued. Even though the rally today still leaves it below the offer price, it makes sense that the stock would move close to this level in the short term.

The action plan

I’m seriously thinking about buying the stock for my portfolio. Part of the idea here is a potential recovery in the share price. This could be enhanced if interest rates fall this year and property values tick higher. Yet the other angle is the dividend income. The current yield is 7.60%, which is well above the index average. So even if the share price takes a long time to recover, I could pick up good income in the meantime.

A risk is that another company comes in and buys the business. Even though I might make a quick buck on the sale price, it would mean that I would have to sell my stock and try to find another opportunity. Another risk is if interest rates stay evelated for longer than I expect, putting further pressure on borrowing rates for Assura.

People probably view it as a ‘risk-free’ option, believing that a bank or building society is unlikely to go bust. And even if one did, the government’s Financial Services Compensation Scheme protects deposits up to £85,000.

I suspect these savers consider themselves to be risk-averse. But it’s undeniable that the real value of their cash is going down. Surely the point of investing is to try and grow your money?

Even if the £276bn was redeployed into interest-bearing accounts, savers would be better off.

However, with my spare cash, I prefer to buy UK shares.

For example, from 1 February 2020 to 31 January 2025, the FTSE All-Share index, which captures 98% of the value of UK equities, increased by 37.9%. This figure — equivalent to an average annual increase of 6% — is based on all dividends received being reinvested.

A tool on the Bank of England website shows that, over the same period, the purchasing power of the pound has been eroded by 24.6%.

However, this analysis comes with a few health warnings.

There’s no guarantee that history will be repeated. Just because the UK stock market grew in the past, it doesn’t necessarily mean it’ll grow again. As billionaire investor Warren Buffett once said: “If past history was all that is needed to play the game of money, the richest people would be librarians.”

And, as noted above, some of the growth of the FTSE All-Share index came from the reinvestment of dividends. But due to the volatility of company earnings, payouts can go down or be suspended.

Therefore, investing in stocks and shares isn’t risk-free.

The biggest and best?

My personal preference is for FTSE 100 stocks. In theory, due to their strong balance sheets and global reach, the profits of these companies should be more stable.

And most of them pay dividends.

National Grid (LSE:NG.) is a stock that a cautious saver could consider.

That’s because its share price tends to be less volatile than most. Over the past five years, its monthly beta has been 0.28. In other words, if the stock market changes in value by 1%, National Grid’s share price will – on average – rise (or fall) by 0.28%.

And it offers a healthy dividend. Over the past 12 months, it’s paid 54.96p a share. This means it presently (17 February) yields 5.7%. The average for the FTSE 100 is 3.6%.

However, the transmission and distribution of gas and electricity requires expensive infrastructure. The company surprised investors in May 2024, when it announced a £7bn rights issue.

It’s also regulated, which means it has to meet certain performance targets. Otherwise, it could face fines or other penalties.

But it doesn’t face any competition and — for over two decades — has consistently increased its dividend each year.

For those cautious savers who currently aren’t earning any interest on their cash, National Grid could be a UK share to consider.

The first earnings season of 2025 has offered an early glimpse into how America’s largest companies expect President Donald Trump’s policies to impact their businesses.

Words like tariff and immigration are popping up at a higher frequency on the earnings calls of S&P 500-listed firms as Trump prioritizes policies around these themes, a CNBC data analysis shows.

CEO of Meta and Facebook Mark Zuckerberg, Lauren Sanchez, Amazon founder Jeff Bezos, Google CEO Sundar Pichai and Tesla and SpaceX CEO Elon Musk attend the inauguration ceremony before Donald Trump is sworn in as the 47th US President in the US Capitol Rotunda in Washington, DC, on Jan. 20, 2025.

Saul Loeb | Via Reuters

During Mettler-Toledo‘s earnings call earlier this month, executives found themselves fielding a barrage of questions about one key topic: tariffs.

The Ohio-based maker of industrial scales and laboratory equipment had already opened the call by breaking down the expected impact from President Donald Trump’s still-evolving trade policy. But when the event transitioned to the question-and-answer portion, the inquiries from analysts seeking further detail about potential tariffs were constant.

“Uncertainty remains across many of our core markets and the global economy,” Finance Chief Shawn Vadala said on the Feb. 7 call. “Geopolitical tensions remain elevated, and include the potential for new tariffs that we have not factored into our guidance.”

Mettler-Toledo’s experience wasn’t unique. America’s largest companies are getting inundated with queries about how or if Trump’s salvo of promises on issues ranging from international trade to immigration and diversity will alter businesses.

A CNBC analysis shows multiple core themes tied to Trump’s policies are popping up on the earnings calls of S&P 500-listed companies at an increasing clip. Take “tariff.” Just weeks into the new year, the frequency of the word and its variations on earnings calls hit its highest level since 2020 — the last full year of Trump’s first term.

On top of that, new acronyms and phrases, like the “Gulf of America” or “DOGE,” have found their way into these meetings as the business community assesses what Trump’s return to power means for them.

Curiously, Trump himself wasn’t racking up mentions on these calls. Many uses of the word “trump” in transcripts reviewed by CNBC referred to the verb, rather than the president.

FILE PHOTO: A logo sign outside of a facility occupied by Mettler Toledo in Columbia, Maryland on March 8, 2020.

Kristoffer Tripplaar | Sipa USA | AP

Still, a review of call transcripts shows how key words tied to Trump’s policies have quickly become commonplace. With the first earnings season of 2025 more than 75% complete, the comments offer an early glimpse into how these companies view the new administration.

Tariffs

One of the most talked about policies has been Trump’s tariff plans. The president briefly implemented — and then postponed — 25% taxes on imports to the U.S. from Mexico and Canada. He also separately slapped China with a 10% levy and imposed aluminum and steel tariffs. Then, on Thursday, he discussed a plan to impose retaliatory tariffs on other trading partners on a country-by-country basis.

Given the uncertainty, it’s no surprise tariffs are a hot topic. The topic has come up on more than 190 calls held by S&P 500 companies in 2025, putting it on track to see the highest share in half of a decade.

The frequency picked up late last year as Trump’s return to the White House became clear. About half of calls in 2024 that mentioned forms of the word took place in the fourth quarter, according to a CNBC analysis of data from FactSet, a market research service.

“Studying tariffs has been at the top of the list of things that we’ve been doing,” said Marathon Petroleum CEO Maryann Mannen on the energy company’s Feb. 4 earnings call.

Several companies said they were not factoring potential impacts from these levies into their guidance, citing uncertainty about what orders will actually go into place. Others just aren’t sure: At Martin Marietta Materials, CFO James Nickolas said the supplier’s profits could either benefit or take a hit from tariffs depending on what form ultimately takes effect.

While Generac didn’t calculate how these import taxes could affect future performance, CEO Aaron Jagdfeld said the generator maker is ready to mitigate the financial hit by reducing costs elsewhere and raising its prices. Camden Property Trust CEO Richard Campo said a company analysis shows proposed tariffs would push up costs for materials from Canada and Mexico like lumber and electrical boxes. These comments offer support to the idea that Trump’s tariffs may drive up consumer prices and fan inflation.

Aaron Jagdfeld, CEO, Generac

Scott Mlyn | CNBC

Zebra Technologies CFO Nathan Winters said price increases could help mitigate profit pressure. Auto parts maker BorgWarner, meanwhile, anticipates another year of declining demand in certain markets, which CFO Craig Aaron attributed in part to potential headwinds from these levies.

Cisco‘s R. Scott Herren agreed with other executives on the lack of clarity, describing the tariff situation as “dynamic” on the networking equipment maker’s earnings call last week. Still, the CFO said the company has planned for some variation of Trump’s tariff proposals to take effect and is expecting costs to increase as a result.

“We’ve game planned out several scenarios and steps we could take depending on what actually goes into effect,” he said.

Immigration

The topic of immigration, meanwhile, has already come up on the highest share of calls since 2017.

Trump has promised mass deportations of undocumented immigrants during his second term in office. Cracking down on immigration has been a core component of Trump’s political messaging since he ran in part to “build the wall” between the U.S. and Mexico for his first term. Critics assert that his plans would shock the labor market and could result in higher inflation.

Immigration mentions tend to tick up during the first year of a new administration, CNBC data shows. But 2025 has surpassed the first years of Joe Biden’s presidency and Barack Obama’s second term, underscoring Trump’s role in elevating the issue within U.S. businesses.

Some companies grouped immigration with tariffs as drivers of broader unpredictability within the economy. Nicholas Pinchuk, CEO of toolmaker Snap-On, described anecdotes of strong demand for repair services from its clients, but said they were still stressed by red flags in the economic backdrop.

“It’s clear the techs are in a good position. But that doesn’t make them immune to the macro uncertainty around them: ongoing wars, immigration disputes, lingering inflation,” Pinchuk said. “Although the election is in the rear mirror and the new team may be more focused on business expansion, there’s a rapid fire of new initiatives. … It’s hard not to be uncertain about what’s up.”

Firms in a variety of sectors took questions about what changes in the composition of America’s population would mean. AT&T, Verizon and T-Mobile all fielded questions about whether a slowdown in immigration would hurt demand for certain phone plans. Michael Manelis, operations chief at apartment manager Equity Residential, said in response to an immigration-related inquiry that it hasn’t seen any upticks in lease breaks from tenants being deported.

In the Southern California market, real estate developer Prologis CEO Hamid Moghadam said deportations can decrease the pool of workers and, in turn, drive up employment costs in the region. That can exacerbate pricing pressures already expected as the Los Angeles community rebuilds in the wake of last month’s wildfires.

Employees of Tyson Foods

Greg Smith | Corbis SABA | Getty Images

Other businesses insisted deportations wouldn’t create labor shortages for their operations because all of their workers are legally authorized. One such company, chicken producer Tyson Foods, said it hasn’t had factories visited by U.S. Immigration and Customs Enforcement or seen any declines in worker attendance.

“We’re confident that we’ll be able to continue to successfully run our business,” CEO Donnie King said on Feb. 3.

DOGE and the Gulf

Topics that gained newfound relevance with Trump’s return to office have also already started emerging.

DOGE — the acronym for the new Department of Government Efficiency led by Tesla CEO Elon Musk — has been mentioned on more than 15 calls, as of Friday morning. This department has put Wall Street on alert as investors wonder if contracts between public companies and federal agencies could be on the chopping block with Musk’s team slashing spending.

Iron Mountain‘s mine that stores government retirement records was ripped as an example of inefficiency by Musk during a visit to the Oval Office. But surprisingly, CEO Bill Meaney said the push for streamlining can actually benefit other parts of its business.

“As the government continues to drive to be more efficient, we see this as a continued opportunity for the company,” he said last week.

A man exits the Iron Mountain Inc. data storage facility in Boyers, Pennsylvania, U.S., on Tuesday, Feb. 13, 2018. The underground data center, located in a former limestone mine, stores 200 acres of physical data for many clients including the federal government.

Stephanie Strasburg | Bloomberg | Getty Images

Executives at Palantir, the defensive technology company that was a top performer within the S&P 500 last year, are similarly hopeful. Technology Chief Shyam Sankar described Palantir’s work with the government as “operational” and “valuable,” and is hopeful that DOGE engineers will be “able to see that for a change.”

“I think DOGE is going to bring meritocracy and transparency to government, and that’s exactly what our commercial business is,” Sankar said during the company’s Feb. 3 call. “The commercial market is meritocratic and transparent, and you see the results that we have in that sort of environment. And that’s the basis of our optimism around this.”

He noted some concerns among other government software providers, and called those agreements “sacred cows of the deep state” during the call.

Elsewhere, the so-called Gulf of America has been a point of divergence after Trump’s executive order renaming what has long been known as the Gulf of Mexico. Chevron used the moniker Gulf of America repeatedly in its earnings release and on its call with analysts late last month. But Exxon Mobil, which held its earnings call the same day, opted instead to refer to the body of water as the Gulf of Mexico.

Nvidia (NASDAQ: NVDA) stock took a bit of a bruising in January, falling 13% at one point. However, it’s bounced back and is now 3.4% higher in 2025. Over five years, it’s up by a scarcely believable 1,817%!

The AI chip king is due to release its Q4 2025 earnings on 26 February. Here, I’ll take a look at the latest forecasts heading into the results report.

Incredible growth

Since ChatGPT was released in late 2022, Nvidia’s quarterly results have blown away Wall Street’s estimates.

The table below shows the revenue and earnings per share (EPS) figures, along with the surprise outstripping of EPS expectations.

Quarter*

Revenue

Revenue surprise

EPS

EPS surprise

Q1 24

$7.2bn

10.1%

$0.11

18%

Q2 24

$13.5bn

20.7%

$0.27

29.7%

Q3 24

$18.1bn

11.2%

$0.40

18.5%

Q4 24

$22.1bn

8.4%

$0.52

12.3%

Q1 25

$26bn

5.8%

$0.61

9.2%

Q2 25

$30bn

4.4%

$0.68

5.4%

Q3 25

$35.1bn

5.8%

$0.81

8.3%

* Nvidia’s fiscal year starts in February.

As we can see, Nvidia was crushing estimates by double digits around a year ago. However, as the AI revolution has matured and analysts have a better grip on demand for chips, these surprises have understandably fallen into the single digits.

Of course, that’s still impressive, and it means Nvidia has beaten estimates on both the top and bottom lines every single quarter since the start of 2023. And over the period, it has added a mind-boggling $2.8trn in market capitalisation!

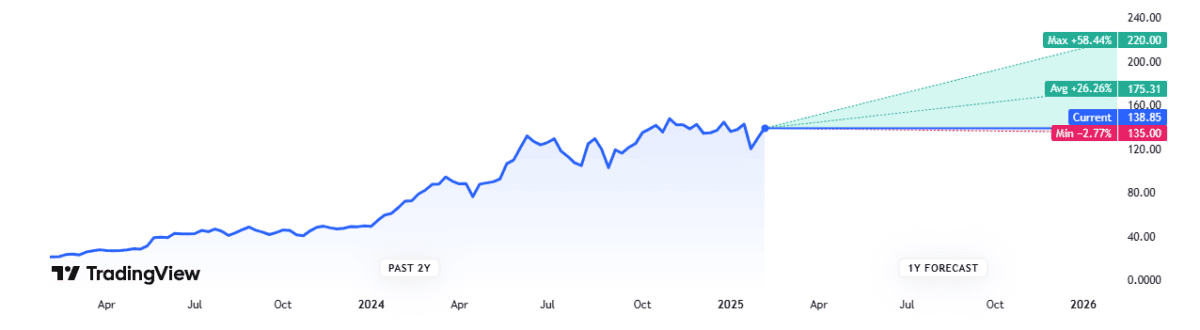

For Q4 25, Wall Street expects revenue of $38bn and EPS of $0.84. That would represent exceptional respective growth of 72% and 64%.

These are the headline figures that investors should look out for. Though the thing that will probably decide the direction of the share price afterwards is forward guidance for Q1 26. Investors will want to know that AI chip demand is going to remain strong this year.

Right now, analysts are forecasting revenue of $41.7bn and EPS of $0.91 for the current quarter (Q1). If the company revises this upwards, the stock could jump higher, and vice versa.

Price target

Broker share price targets should always be taken with a pinch of salt, especially when it comes to a volatile stock like Nvidia. Having said that, they can provide valuable insight into potential market disparities.

So, what’s the latest on this front for Nvidia? Based on 52 analysts covering the stock, the average 12-month price target is $175. That’s around 26% higher than the current share price of $138.

Created at TradingView

Valuation

Finally, we have the valuation. Based on current FY26 estimates, the stock is trading at roughly 31 times forward earnings. That doesn’t look too demanding to me, given the company’s rapid growth.

Combining this with the $175 price target, a convincing case could be made that this is a growth stock to consider buying.

What could go wrong?

However, as Stanford computer scientist Roy Amara once said: “We tend to overestimate the effect of a technology in the short run and underestimate the effect in the long run.”

In other words, transformative new technologies have rarely avoided early speculative bubbles throughout history. The internet was the most famous example, though there have been others.

Moreover, around 36% of Nvidia’s sales came from just three customers in the last quarter. If these customers scale back their AI infrastructure spending after initial build-outs, the chipmaker could experience an immediate slowdown in revenue growth.

Given this medium-term uncertainty, I’m not going to buy the stock at today’s price.

There have been ups and downs, but over time America’s S&P 500 has proved itself a top destination for investors seeking tremendous returns.

Since 2010, the share index has delivered an average annual return of almost 14%. Returns during this time have been supercharged by its large contingent of high-growth tech stocks like Nvidia, Microsoft and Tesla.

But doubts are creeping in as to whether the S&P 500 can maintain its record. This follows plans by US President Donald Trump to impose potentially crushing trade tariffs on major trading partners.

What does this mean for investors?

Stark warning

Scanning the financial pages this morning (17 February), I was drawn to an interview in The Guardian with Nobel prize-winning economist Joseph Stiglitz.

Discussing potential US tariffs and reciprocal taxes from trade partners, he said that “it risks the worst of all possible worlds: a kind of stagflation.”

Stiglitz said that uncertainty related to Trump’s trade plans would slow economic growth, while new tariffs could also push up costs for business and consumers.

He commented that “how much it will increase prices is a little bit affected by the magnitude of the appreciation of the exchange rate, but all economists think that the extent of the appreciation of the exchange rate won’t be anywhere near enough to compensate for the tariffs.“

Don’t panic yet

Investors need to be extra careful in this climate. However, I feel there’s also no need for them to panic.

First, there’s no guarantee that new trade rules will come into place. Trump’s decision to delay tariffs on Mexico and Canada last month indicates room for manoeuvre.

There’s another important thing to remember. While economists like Stiglitz deserve attention, we’ve seen many times before that predictions of doom and gloom can be overstated.

So, is the S&P 500 still an attractive place to consider investing? I think so, which is why I plan to continue holding US shares, trusts and funds.

Spreading risk

While the outlook is more uncertain today, there are still good reasons to expect S&P shares to outperform over the long term. These include:

The robustness of the US economy.

Further rapid growth in the digital economy that powers tech profits.

Dominance by S&P 500 companies in major sectors like healthcare, finance and technology.

The S&P’s large global footprint providing added earnings opportunities.

It’s also important to remember the robustness of the US stock market over time. Since its inception in 1957, the S&P 500 has overcome multiple crises — including wars, recessions, pandemics and political turmoil — and has hit new record highs in 2025 despite tariff worries.

However, cautious investors may wish to consider buying an index-tracking exchange-traded fund (ETF) as well as purchasing individual shares today. The HSBC S&P 500 ETF (LSE:HSPX) is one I hold in my own portfolio.

By investing in hundreds of different companies, the fund helps investors manage a low-growth scenario through holdings in cyclical and non-cyclical businesses. It also includes industries that are less vulnerable to inflationary pressures, like consumer staples and healthcare.

Finally, the fund limits exposure to sectors that could be directly impacted to a large degree by trade tariffs, such as the car industry and agriculture.

This HSBC product isn’t immune to economic volatility. But over the long term, I still believe it could continue delivering excellent returns.

Back in November, I noted that Warren Buffett’s investment company, Berkshire Hathaway, had been buying shares in Domino’s Pizza (NASDAQ: DPZ). I’d been looking at 13F regulatory filings (which show the trades of large money managers in the US), and these had shown that the stock market guru had snapped up 1.27m shares in the pizza chain in the third quarter of 2024.

It seems that these 1.27m shares in Domino’s were just the start for Buffett and Berkshire, however. Because the latest 13F filing (published in the last few days) shows that in Q4 2024, he bought a lot more shares.

Half a billion worth of stock

The latest 13F reveals that in Q4, Berkshire Hathaway bought another 1.1m shares in Domino’s. This increased his position size by 86.5% (which is significant).

We don’t know exactly what price Buffett (or his investment assistants) paid for these shares. However, at today’s share price of $477, we’re talking about approximately $525m worth of stock.

Now, a lot of investors like to copy Buffett’s trades. And it’s easy to see why – over the last half century he’s generated huge returns from the stock market.

However, I’m not convinced that buying shares in the US-listed version of Domino’s Pizza here is the best move. While the company does have a great brand and long-term track record, it currently trades at 27 times this year’s forecast earnings (which is high) and offers a dividend yield of just 1.4% (low).

To my mind, the risk/reward setup is not great at those metrics. If revenue or earnings were to come in below forecasts for some reason (like lower levels of consumer spending), the stock could take a hit.

Does Domino’s UK offer more value?

It’s a different story with the UK-listed version of Domino’s Pizza (LSE: DOM) though. Currently, this stock trades on a price-to-earnings (P/E) ratio of just 14. And the dividend yield is a healthy 3.8%. At those metrics, the risk/reward set-up looks quite compelling, in my view.

I’ll point out that while the two companies share the Domino’s Pizza name (which is one of the most powerful fast food brands in the world), they are different businesses. Whereas the US-listed stock offers exposure to the US market (which is huge) and international franchises, the UK-listed stock offers exposure to the brand in the UK and the Republic of Ireland (much smaller markets).

Given that the UK-listed Domino’s is focused on smaller markets, there’s less long-term growth potential. There is probably also more risk of something going wrong (such as a shift in consumer preferences).

However, I reckon a lot of this is factored into the valuation. A P/E ratio of 14 seems very reasonable to me given this company’s strong long-term track record (revenue climbed from £289m in 2014 to £680m in 2023).

Given the low valuation and healthy yield, I believe that shares in the UK-listed version of Domino’s are worth considering for a portfolio today. Taking a long-term view, I think they have the potential to deliver solid returns.

It’s often confusing to decide what sort of equities to put in a Stocks and Shares ISA. In truth, there’s no definitive answer. The right selection relies on each individual investor’s objectives and risk tolerance. However, for those aiming for passive income, dividend shares are often found to be one of the best methods of securing stable and regular returns.

With a Stocks and Shares ISA, UK residents benefit from tax free gains on any investments up to £20,000 a year.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice. Readers are responsible for carrying out their own due diligence and for obtaining professional advice before making any investment decisions.

With that said, let’s investigate ways to kick off and investment journey that could lead to a £100-a-month steady income stream.

An ISA income strategy

The UK stock market tends to deliver slightly less than 8% on average per year, with dividends included. That’s based on the performance of the FTSE 100 and FTSE 250 over the past few decades. It’s common practice to draw down only 4% from an income portfolio each year, so as to avoid disrupting the growth trajectory.

We know that an investor would need to bring in £5,200 a year to equate to £100 a week. That works out to 4% of £130,000.

That’s a lot of money to have in an ISA. It’s way above the yearly tax-free allowance, which in itself is a lot to save per year. Suffice to say, it’ll take some time to build up.

Let’s assume the average investor can afford to contribute £300 per month (£3,600 a year). It would take over 17 years to get there based on the 8% average return (with dividends reinvested). That’s a long time! However, optimal stock selection could help reduce this time. It’s not impossible for a well-formulated UK stock portfolio to achieve annual returns upward of 10%.

Picking top stocks

To beat the average market returns, it’s important to pick the right stocks. A few financial factors to consider are profit margins, debt levels and cash flow. Additionally, it’s important to assess the long-term viability of its products or services versus competitors and its particular advantages — also known as the ‘moat’.

Finally, an experienced management team with transparent practices and strong corporate governance is a plus.

One top UK share investors may want to consider is London Stock Exchange Group (LSEG).

The company provides financial data about the UK’s stock market. With a wide moat and solid market position, the growing demand for market analytics puts the company in good stead for future growth. After acquiring data analytics firm Refinitiv in 2021, it’s gone from strength to strength.

It’s been performing almost too well lately, up 32% in the past year. Meanwhile, earnings have lagged behind, leading to a price-to-earnings (P/E) ratio near 100. If the next earnings call falls short of expectations, there’s a high risk the share price will drop in the short term.

Long-term prospects look solid though, supported by strong management and a growing demand. Revenue for 2024 is expected come in at £8.6bn, up 8% from 2023. With a growing subscription service, cash flows are increasing and driving shareholder returns. Over the past 10 years, it’s delivered annualised returns of 16.78%.

Last Thursday (13 February), Alibaba confirmed it would be partnering with Apple (NASDAQ:AAPL) with regards to artificial intelligence (AI) features for iPhones in China. Both stocks rose as a result, with Apple up 6% in the past week. I don’t think the news got enough attention, as this could be a really big deal for both companies. Here’s why.

The background

Apple’s been struggling in China over the past couple of years. For example, it experienced a 17% decline in annual smartphone shipments in China in 2024. This was the largest fall since 2016. Apple hasn’t been able to keep up with domestic competitors in this space, and has been further hamstrung when trying to launch new AI features in hardware such as iPhones.

In line with local regulations, Apple has to collaborate with domestic firms for AI implementations. That’s where Alibaba comes in. In working together on this project, it means that Apple can add the features.

While technical details haven’t been publicly released yet, the integration’s expected to enhance applications such as voice recognition, natural language processing, and personalised user experiences.

Why this is big for Apple

In partnering with Alibaba, Apple’s pretty much solved the issue of getting AI features onto iPhones in the country. That in itself is big win, as I’m sure consumers there are currently buying competitor products with these AI features as a key consideration to purchase. So if Apple can rectify this, sales should increase.

Interestingly, the language model for AI that Alibaba uses is specifically trained for the Chinese culture and user behaviour. I believe this is a better fit than Apple’s own in-house AI model for the local market. Therefore, it’ll be able to benefit from this tailored model without having to have spent time or effort in developing it.

Finally, the move to choose Alibaba, which is a government-backed company, is important. It certainly pays to stay on the right side of regulators. So with this move, aligning with Alibaba could help Apple maintain favour with Chinese regulators in the future.

Action from here

Apple shares are up 33% over the past year. It’s true that with the stock close to all-time highs, there’s a risk things are a little overvalued. Another specific risk is that Apple might struggle to take market share in China even with the new partnership. It could take time before we see a material increase in sales.

However, I think that for long-term investors, it’s still a good opportunity to consider right now. The size of the market that could be opened up with this new tie-up, along with the implications of working with a local business, could be a large win in coming years.

Financial News

Daily News on Investing, Personal Finance, Markets, and more!