Investors with a more conservative desire might find the Ice style appealing. By focusing on businesses that have shown consistent financial performance and growing dividends, we seek to beat the market with a mix of income and steadily rising share prices. We consider this to be a lower-risk investing strategy than Fire, but company and industry specific risks mean diversification remains important.

Ice investing can generate large, short-term gains on occasion, but we’re primarily seeking steady gains over time, and shallower declines during wider stock market falls. These qualities are most commonly found in established firms, but the Ice approach does not focus exclusively on large companies. We often see ample opportunity to invest in medium-sized companies, with strong niche positions in their industry and the ability to grow their dividends for years to come.

“The company also commands a lower valuation than other businesses that have technological innovation as a cornerstone of their strategies – while the long-term dividend track record might offer assurance to Ice-style investors.”

Mark Stones, Share Advisor

February’s Ice recommendation:

Redacted

Want The Full Recommendation? Enter Your Email Address!

Billionaire investor Warren Buffett has delivered many words of investing wisdom over the past few decades. Often, his most powerful have been the simplest.

For instance, in his 2021 letter to Berkshire Hathaway shareholders, Buffett wrote these four key words: “Never bet against America.”

Since the aptly-named Oracle of Omaha said that, an artificial intelligence (AI) revolution has unleashed a tidal wave of innovation and investment. Nvidia alone has added nearly $3trn to its market capitalisation — more than the entire London Stock Exchange!

Any investor who had heeded Buffett’s words four years ago and bought into an S&P 500 tracker would be up over 60% with dividends. For the tech-driven Nasdaq 100 index, the return is around 70%.

And even though Buffett has been selling stocks in recent quarters, he says that the majority of Berkshire Hathaway’s portfolio will remain invested in the US market.

US dominance

Imagine the following workday — not totally out of the ordinary — for someone in the UK.

They are woken up by the alarm on their Apple iPhone, before rising to make a cup of Costa-branded coffee (owned by Coca-Cola) and a bowl of cereal (probably a brand from Kellanova, commonly known as Kellogg’s).

Munching their flakes, they scroll through social media — Instagram, Facebook (both owned by Meta), and X. Then they go to work (perhaps in a Ford, Tesla, or Uber rideshare).

In the office, they check their emails (Google or Microsoft), and probably use software and platforms from Workday, Salesforce, and Microsoft. Perhaps a couple of Zoom meetings will take place.

After work, they go home and order some food (via Uber Eats). Then they unwind with Netflix and YouTube — owned by Alphabet (NASDAQ: GOOG) — before doing a bit of shopping on Amazon.

Before turning in, they book a relaxing weekend away (through Booking Holdings or Airbnb).

Meanwhile, every single card/online payment they’ve made all day (and every day) is processed by Visa or Mastercard.

A cheap tech stock

Four years ago, Buffett also said: “In its brief 232 years of existence…there has been no incubator for unleashing human potential like America.”

When I look ahead to future potential mega-trends (space exploration, quantum computing, virtual reality, etc), it is US-listed firms that are in pole position to dominate.

Take Alphabet. Best known as the parent of Google and YouTube, it also owns robotaxi firm Waymo. Last year, the company provided over 4m driverless taxi rides, averaging 150,000 trips per week. Waymo is moving into Austin and Texas in 2025, as well as Tokyo, then Miami in 2026.

Then there is quantum computing, which Google has been working on for over a decade. That could be an utterly transformative technology, driving the US stock market even higher.

Admittedly, Alphabet does face regulatory scrutiny and competitive threats to its search empire. But currently trading at just 21 times forward earnings, I think this US stock is worth considering.

Diversification

Beyond Alphabet, there’s a risk that many US stocks are currently overvalued (which probably explains why Buffett has been selling). So I think some allocation to other shares — cheaper UK ones, for example — is a wise move.

Longer term though, I still want exposure to the US market due to its record of innovation and growth. Many of its top firms also have massive international operations.

For investors looking to build passive income, UK dividend stocks can offer a steady stream of cash.

The FTSE 100 index has an average dividend yield of around 3.5% right now. That’s pretty good, but there are some companies with payouts of 5% or more. That means a £20,000 investment could potentially generate over £1,000 in annual dividends.

Here are two well-known financial services companies that have strong yields and long records of steady dividend payouts.

Pensions and insurance giant

Legal & General (LSE: LGEN)is one of the UK’s biggest financial services firms, specialising in pensions, life insurance, and investment management. It has been a staple of the FTSE 100 for years and is well-known for its solid dividend policy.

The stock is yielding 8.8% as I write on 24 February — significantly above the Footsie average.

Over the past decade, the company has either maintained or increased its dividend. That consistency is a key reason why many income investors follow the stock closely.

In its most recent update, the company reaffirmed its commitment to paying out dividends, while acknowledging challenges including ongoing market volatility and low margins.

The share price has had a mixed performance lately, moving in line with broader financial sector trends. While it has recovered from some lows in 2023, it still remains below pre-pandemic levels.

Steady dividend payer

M&G (LSE: MNG) is another financial services giant. The company has a £5bn market cap and is best known for its investment management and savings products. Like Legal & General, it has built a reputation for steady dividend payouts.

The company currently boasts an even higher yield of 9.5%. That’s one of the highest in the Footsie and means a £20,000 investment could return nearly £2,000 in annual payouts.

However, there are some risks to consider. M&G’s share price fell by more than 10% in 2024, reflecting investor worries about economic conditions and potential pressure on profits.

While the company remains committed to maintaining its dividend, a yield this high sometimes signals uncertainty. Recent share price falls raise the risk of a ‘value trap’ where investors are lured by high yields only to see subsequent dividend cuts.

That being said, M&G has a history of rewarding shareholders, and it has stated that dividends are a key part of its strategy.

If the company can arrest recent outflows and continue to regain its long-term earnings stability, then the strong dividend payouts could continue.

Too good to be true?

When dividend yields climb this high, it’s often worth asking why. The market may be pricing in risks for both companies given they’re exposed to interest rate moves, regulatory changes, and market downturns.

If profits drop, dividends may need to be cut. This is just one reason why portfolio diversification is so important.

Investing a £20,000 lump sum into either of these two companies may be tempting, but I would much rather spread my risk across many shares in the market to avoid concentration risk and large portfolio movements driven by one or two names.

Of course, these are just a couple of high-yield stocks that investors should consider. Others within the Footsie may be able to offer £1,000 in potential annual dividends from the same investment while operating in different sectors and reducing overall portfolio risk.

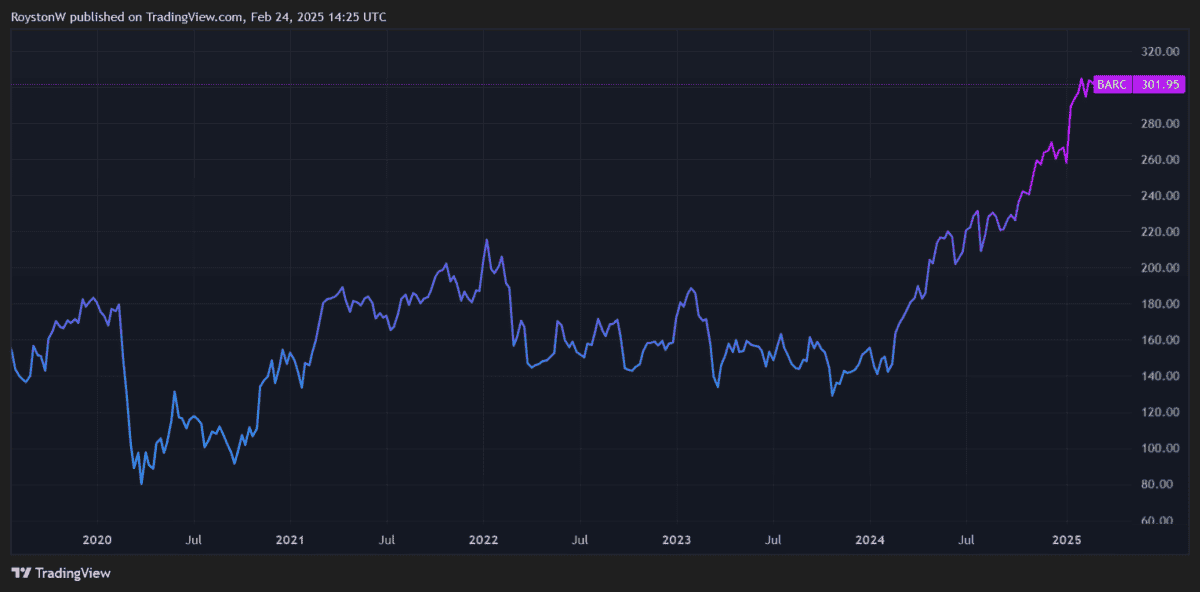

Demand for Barclays (LSE:BARC) shares hasn’t been dampened by alarm bells ringing for the UK economy and uncertainty in the US.

At 302p per share, the Barclays share price is up 14% since the start of 2025. This takes total gains for the past year to a whopping 83%.

Source: TradingView

City analysts don’t believe the FTSE 100‘s bull run is finished yet either. They’re tipping more double-digit increases over the next 12 months.

Should I consider snapping up Barclays shares?

11% more to go?

First, it’s worth noting that there are some large variances across brokers’ current forecasts.

One particularly bullish analyst thinks Barclays’ share price will rise an extra 29% over the next year, to 390p. At the other end of the scale, one pessimistic forecaster has set a 12-month price target of 230p, down 24% from current levels.

Having said this, the overall picture painted by City brokers is pretty upbeat. The average price target among 17 brokers is 335.20p per share. That represents an 11% premium to today’s price.

Cheap on paper

One reason why analysts think Barclays shares will rise could be because of its relative cheapness.

The number crunchers think the bank’s annual earnings will jump 17% in 2025. This leaves it trading on a price-to-earnings-to-growth (PEG) ratio of 0.4.

Any reading below one indicates that a share is undervalued.

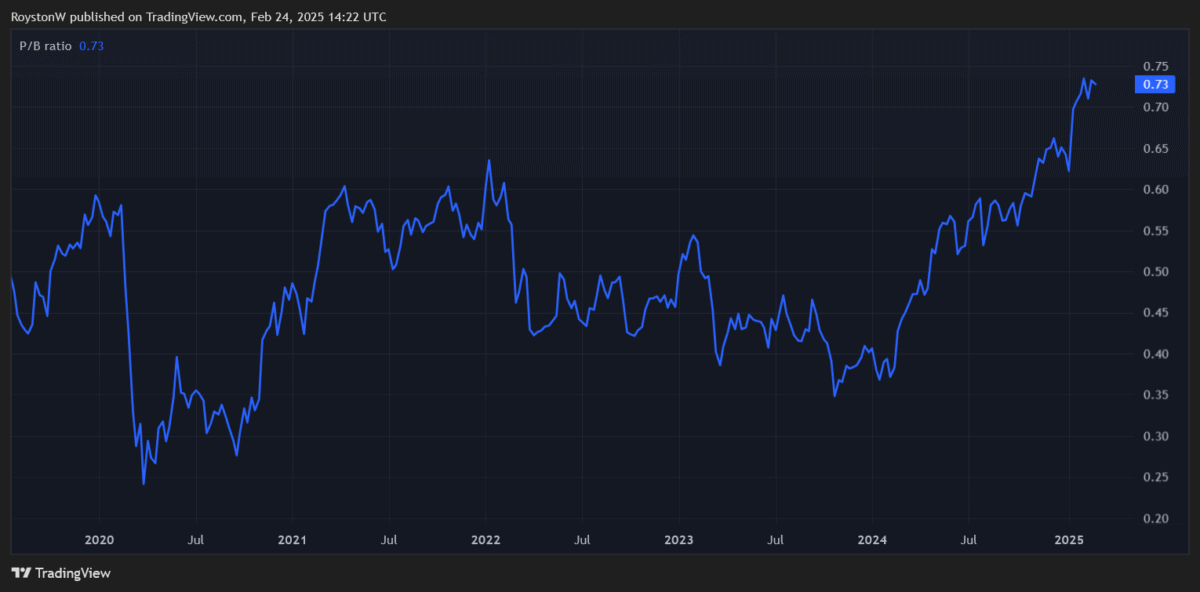

Furthermore, Barclays’ price-to-book (P/B) value is also below one, indicating it trades at a discount to the value of its assets.

Source: TradingView

Finally, the firm’s price-to-earnings (P/E) ratio of 7.1 times for this financial year is also extremely low, including relative to those of its peers.

Other UK-focused banks Lloyds and NatWest carry forward earnings multiples of 9.9 times and 8 times, respectively.

Reward vs risk

With brokers tipping an 11% price rise, and the Footsie bank also offering a 3% dividend yield, it’s easy to see why Barclays shares are so popular today.

The company’s forecast-beating results for 2024 and revised medium-term targets have also boosted investor appetite. The bank now expects to deliver a return on tangible equity (ROTE) of 11% and 12%-plus in 2025 and 2026, respectively, up from 10.5% last year.

This is thanks largely to impressive performances at the firm’s large investment bank.

But with inflationary pressures increasing, and other new hazards (like fresh trade tariffs) threatening the fragile economy, trading conditions here might become a lot tougher from this point.

At the same time, the threats to Barclays’ retail business are also considerable. Net interest margins (NIMs) could shrink sharply thanks to a double-whammy of rising competition and falling interest rates.

I’m also fearful of the prospect of weak loan growth and rising impairments if economic conditions remain tough. Worryingly, the bank incurred a forecast-topping £2bn worth of credit impairment charges last year, up 5% from 2023 levels.

Finally, Barclays risks facing substantial financial penalties if found guilty of mis-selling car finance. It’s set aside £90m to cover possible costs, though experts warn the actual figure could be far higher.

While City brokers are bullish on Barclays’ share price, I don’t plan to add the bank to my own portfolio. The risks are too great for my liking, even despite the cheapness of its shares.

The FTSE 100 is home to some big-name stocks, but not all of them are soaring right now. One company that’s caught my attention is easyJet (LSE: EZJ).

As I write on 24 February, shares in the budget airline are down 11.4% since the start of 2025. This is despite the Footsie gaining more than 5% in the same time.

The company is synonymous with budget travel in Europe and has been working hard to expand its flight network. I wanted to see if this well-known name with promising financials and a beefed-up dividend would be a good fit for my portfolio.

How has the easyJet share price been travelling?

easyJet had a strong 2024. The airline posted a 34% jump in pre-tax profits to £610m, driven by a record-breaking summer. Revenue climbed 14% to £9.3bn, with almost 90m passengers flying with the carrier.

The stock’s post-pandemic recovery was punctuated by management more than doubling the dividend from 4.5p to 12.1p per share.

Despite the impressive annual results, easyJet’s valuation has slid lower in the early part of 2025. Management pointed to this year’s timing of Easter as a key reason for the weaker-than-expected second quarter, as well as investments in new, longer routes that will take a while to reach full potential.

Valuation

Let’s talk numbers. At its current £4.93 share price, easyJet has a price-to-earnings (P/E) ratio of 8.3. This is similar to Ryanair (8.9) but pricier than Wizz Air (6.6). That to me says it is valued reasonably fairly compared to peers.

Of course, these figures are a lot lower than the Footsie average of around 14.5. That’s largely due to the fact that airlines are reliant on consumers spending on travel and leisure, which means their performance can be lower when the economy is in trouble.

The dividend yield is currently 2.5%, which isn’t the highest in the Footsie, but it’s a big improvement from previous years.

My verdict

There’s a lot to like about easyJet right now. Despite the second-quarter wobble, passenger numbers remain solid, while profits and revenues seem to be trending the right way.

Management appear confident in the outlook after more than doubling the dividend. The relative valuation doesn’t give me too much cause for concern.

However, it’s not all sunshine and rainbows. The inherent cyclicality of earnings driven by consumer spending is one reason why easyJet shares could suffer in a recession. Throw in rising geopolitical tensions and uncertain fuel costs, and there are plenty of potential downsides to owning the stock.

On balance, I think easyJet goes in the ‘to watch’ pile for me. There’s no compelling reason for me to buy right now so I think I’ll be investing funds in more defensive sectors like pharmaceuticals for the moment.

Tesla (NASDAQ: TSLA) stock is a strange case. Just when you think it’s grossly overvalued, it bounces back to hit new highs.

Just look at the incredibly volatile share price recently. It’s down 17% in a month and 29% since a December high of $479. Yet since Donald Trump’s election victory, it’s still up 34%. Over one year, the stock is 69% higher — similar to Nvidia!

In the past, all significant dips in the Tesla share price have proven to be buying opportunities. So, should I take this one? Here are my thoughts.

Mounting issues

Tesla has always given investors things to worry about, and today is no different. It’s facing rising competition from both cheaper Chinese electric vehicles (EVs) and traditional Western automakers. Consequently, Tesla’s market share is falling in both Europe and China.

Second, consumer spending remains weak, with many people avoiding big-ticket items like new cars. So the overall growth of the EV market has been decelerating. Long term, it seems certain to be much larger, but for now it’s hit a major speed bump.

Next, Elon Musk has vocally entered politics by backing Donald Trump. This has extended to supporting political parties in Europe, including Germany’s AfD. From a Tesla perspective, I have to imagine this is alienating many core potential customers. Indeed, reports say that the company’s market share in Germany has plummeted from 23% two years ago to just 4% in January.

Moreover, Musk has taken on the task of cutting US government spending. Between this and running X and several other companies (including SpaceX, the world’s most valuable private firm), it makes me wonder how much of Musk’s attention is focused on Tesla.

Most other CEOs would be pressured to leave their role to focus on politics. Yet Tesla’s $1trn market cap might implode if visionary Musk left the company. So this is a bit of a unique situation.

Finally, the company’s growth has ground to a halt. In Q4, revenue increased only 2% year on year to $25.2bn, with automotive revenue declining 8%. Operating profit slumped 23% to $1.6bn.

Remember, it wasn’t that long ago that Musk was projecting supercharged 50% annual growth for the years ahead. Such growth now appears firmly in the rear-view mirror.

Sky-high valuation

According to all conventional metrics, Tesla stock is currently very overvalued. It’s trading at 12 times sales and 113 times forward earnings.

Meanwhile, Tesla’s price-to-earnings-to-growth (PEG) ratio, based on its forecast five-year earnings growth rate, stands at 4.7. That’s a significant premium to the 1.6 average of the other six stocks in the ‘Magnificent Seven’ grouping.

My move

Despite all this, there are things to be excited about in future. One developing business that intrigues me is the Optimus humanoid robot (also known as the Tesla Bot). The company plans to have these working in Tesla factories by the end of this year.

On the Q4 earnings call, Musk said: “Optimus has the potential to be north of $10trn in revenue.” That’s trillions!

While Tesla thinks it could be selling them as early as next year, I’d take that with a pinch of salt. This business might not be producing any meaningful revenue until the 2030s.

As things stand, I’m not going to invest in the stock.

Traders work on the New York Stock Exchange (NYSE) floor on Feb. 20, 2025 in New York City.

Spencer Platt | Getty Images

Spend some time looking at trading volumes, and you’ll notice something interesting: A lot of investors recently are making outsized bets on the stock market.

Most of them are long bets, but some are short.

It’s easy to see this because there is a growing segment of the ETF business that caters to investors who want to make short-term outsized bets on the stock market.

These are leveraged and inverse ETFs. Leveraged ETFs amplify the daily returns of an index or stock using financial derivatives. For example, if an index rose by 1% in a day, a 2x leveraged ETF would deliver a 2% return, a 3x would deliver a 3% return.

An inverse ETF delivers the opposite daily performance. So a 2x inverse ETF would be down 2% on a day when the index rose 1%, and vice-versa.

These leveraged/inverse ETFs are not just growing in assets. They are becoming a greater part of the daily trading volume of the ETF universe, which is becoming a larger part of overall trading.

Who is using these products? It has a lot to do with the general rise in speculative behavior in the market. Trading in options, bitcoin, and other more speculative products has been rising.

“We’re continuing to see more investors lean into leveraged as a way to express short-term views on the market, and given all the volatility and daily market-moving headlines, it’s not surprising we are seeing higher volume and more assets entering the space,” Doug Yones, CEO of Direxion, one of the largest providers of leveraged/inverse ETFs, told CNBC.

Growing as a share of assets

The first leveraged/inverse ETFs in the U.S. started in 2006 and allowed long or short bets on indexes like the S&P 500 or the Nasdaq 100. Leverage and inverse single-stock ETFs came into existence in 2022, and they too have grown fast.

The largest, ProSharesUltraPro QQQ (TQQQ), which provides 3x leveraged exposure to the Nasdaq 100 (QQQ), has nearly $26 billion in assets. Single-stock ETFs that leverage Nvidia and Tesla also now have substantial assets.

Part of this is a bull market effect: Stocks are up meaningfully in the last few years, so overall assets are higher. However, these leveraged/inverse ETFs are not just growing assets, they are becoming a larger part of the ETF universe.

In 2016, when ETFs had about $2 trillion in assets under management (AUM), leveraged/inverse ETFs were about 2% of that AUM, according to Strategas.

Today, ETFs have about $11 trillion in assets under management, but leveraged/inverse ETFs make up about $81 billion of that, or almost 8% of total AUM.

Why are these products growing?

“I do believe there is a generational effect at play, I think there is major appetite among younger traders wanting to play with leverage due to the gains it can provide,” Todd Sohn, head of ETFs at Strategas, told CNBC. “The barriers to entry are extremely low, you can buy these products on your phone.”

Yones estimated that 75% of the ownership of these products were retail traders, and 25% institutional, which included hedge funds, trade desks, large brokerage firms, and “anyone who has a book of positions that wants to be neutral the market.”

He estimated that a small but significant percentage of the retail traders (12%-15% of the total) were from outside the U.S., which aligns with previous reports about growing demand for 24-hour trading coming in part from retail traders in South Korea, Japan, and Europe.

Growing part of daily trading volume

Leverage and inverse ETFs, including leveraged and inverse single-stock ETFs, now routinely show up among the most heavily traded ETFs on a daily basis.

A simple way to look at this is by average daily dollar volume, the total amount of money traded in the ETF on a daily basis.

The top ETFs by daily dollar volume are still ETFs tied to the biggest indexes, mainly the S&P 500, Russell 2000, and Nasdaq 100.

Top ETFs by average 3-month daily dollar volume

SPDR S&P 500 (SPY) $27.7 billion

Invesco QQQ (QQQ) $15.3 billion

iShares Russell 2000 (IWM) $5.7 billion

iShares Core S&P 500 (IVV) $3.9 billion

Source: Strategas

However, the fifth-largest ETF by average daily dollar volume in the last three months is the ProSharesUltraPro QQQ, which provides three times leveraged exposure to the Nasdaq 100.

Altogether, five of the top 20 ETFs by average daily dollar volume are leveraged/inverse.

Leveraged/inverse ETFs: largest avg. 3-month daily dollar volume

These products are bets on short-term momentum, but they have one additional feature that has proven difficult for investors to wrap their head around: they reset on a daily basis.

Because of compounding effects, it can be fiendishly difficult to figure out what actual returns will be on anything more than a daily basis. This means that holding a 2x leveraged product for anything more than a day may result in making substantially less than a 2x return, depending on the direction of the market.

Here’s an example: Suppose the S&P 500 was up 10% one day, then down 10% the next day.

A $100 investment would look like this:

S&P 500: hypothetical $100 investment

Day 0 $100

Day 1 (up 10%): $110

Day 2 (down 10%). $99

After two days of this, you have $99, so you are down 1%. If you had a leveraged product over those two days, it would seem like you would be down 2%, or that you would have $98.

But because of the daily reset, that’s not what happens.

S&P 500: hypothetical $100 investment in 2x leveraged

Day 0 $100

Day 1 (up 10%, leveraged up 20%): $120

Day 2 (down 10%, leveraged down 20%) $96

You actually have $96, instead of $98, and bear in mind this excludes fees.

As time goes on, these calculations get progressively more complex.

As a result, those offering these products routinely state that they are not meant for buy-and-hold investors.

These funds have very large daily turnovers, so most investors seem to understand the risk of holding these products on anything more than a daily basis.

But Sohn told CNBC that all investors in leveraged products needed to be very careful.

“At some point though, it helps to take stock of the risks involved whenever the market takes a turn south,” Sohn told CNBC.

Doug Yones, CEO of Direxion, will be on the ETF Edge portion of Halftime at 12:35 PM ET on Monday, and will also livestream on ETF Edge from 1:30 PM ET. He will be joined by Todd Rosenbluth, Head of Research at Vettafi.

My Stocks and Shares ISA portfolio took a bit of a pounding on Friday (21 February). This was after the US market sold off heavily due to concerns about growth and inflation.

Among the sea of red in my portfolio, however, there was one valiant riser: MercadoLibre (NASDAQ: MELI). Shares of the Latin American e-commerce and fintech giant rose 7% to $2,260, bringing the year-to-date return above 33%.

Why did it spike?

Latin America-based MercadoLibre is a mash-up of Amazon, eBay, PayPal, and Shopify. Last year, gross merchandise volume (GMV) on its e-commerce marketplace surpassed $50bn for the first time, while its logistics arm (Mercado Envios) handled almost 1.8bn items.

Meanwhile, there are now over 61m monthly active users on its fintech app (Mercado Pago). As well as being able to transfer money and pay bills and services, customers using Pago get attractive yields on deposits and access to credit.

The reason for the stock’s jump last week was the firm’s blowout Q4 results. Revenue grew 37% year on year to $6bn (96% on a constant-currency basis), which was slightly higher than Wall Street’s expectations. But earnings per share (EPS) of $12.61 demolished estimates for around $8.

In its shareholder letter, MercadoLibre said: “Retention and frequency on our marketplace are at record levels,as are payments and deposits per user in our digital account, and the number of merchants borrowing from us is higher than ever.”

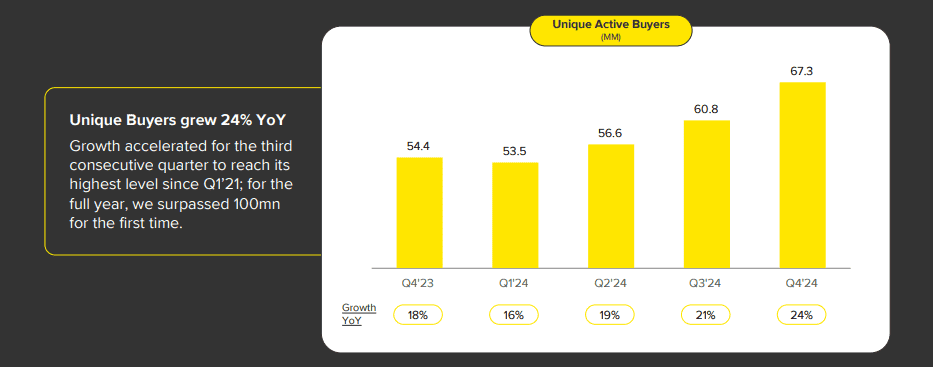

One figure that impressed me was that the number of people going to shop on its e-commerce platform is accelerating. Unique active buyers grew 24% to 67.3m in Q4, which was the third consecutive quarter of accelerating growth.

As bullish as I am on the future of the company, there are risks to bear in mind here. An inescapable one in the region is semi-regular economic instability. Argentina, for example, is still recovering from its crippling inflation crisis.

That said, MercadoLibre just keeps on getting stronger despite all the political and currency crises thrown its way. And despite the vast infrastructure challenges across Latin America, nearly half of its shipments in Q4 were delivered on the same or next day.

Another potential concern is the company’s rapidly expanding credit portfolio. It lends to both merchants and individuals, raising the possibility of rising non-performing loans if economic conditions worsen. As the firm scales its digital banking ambitions over the next decade, this will be something I’ll be keeping an eye one.

Of course, the company is aware of this risk. Last week, it said: “We will closely monitor the health of our credit portfolio, and if we detect any signs of deterioration, we will swiftly adjust and scale back as needed — just as we have done in the past.”

Valuation

The company is still in growth mode, so I prefer to look at the price-to-sales (P/S) ratio to quickly judge valuation. Right now, the P/S multiple is 5.5, which I don’t see as outrageous. Therefore, I think the stock is still worth considering for investors.

MercadoLibre is currently my second-largest holding. But I expect to keep holding for many more years as e-commerce and digital payments mushroom across Latin America. The firm is at the epicentre of these mega-trends.

IAG (LSE:IAG) shares have surged 112% over the past 12 months. That means a £10,000 investment then would now be worth £21,200. That’s a phenomenal return. This remarkable performance stems from three key drivers: resilient travel demand, strategic fuel cost management, and improved investor sentiment toward undervalued aviation stocks.

The airline group, which owns British Airways, Iberia, and Aer Lingus, capitalised on strong post-pandemic demand for travel. This trend has continued well into the 2024 financial year, as consumers prioritised travel experiences over goods. Q3 results show revenue increased by 7.9% year on year and operating profit jumped 15.4%.

Crucially, IAG maintained capacity discipline. In Q3, the business noted modest increases in seating capacity, which appear to be broadly in line with demand. JP Morgan notes the industry’s “benign demand-supply balance” supported pricing power despite economic challenges.

Fuel hedging provides critical ballast

While Brent crude’s 2025 rally to $81/barrel briefly spooked investors, IAG’s fuel hedging strategy mitigated volatility. The company hedged “a proportion” of consumption for up to two years, locking in lower prices. This proved prescient as analysts forecast 2025 fuel costs to trend downward from 2024 levels. Oil prices are expected to stabilise around $70-$75/barrel. JP Morgan estimates this could boost earnings by 15%-20% across European airlines — fuel costs can represent up to 25% of operational costs.

Valuation signal more share price growth

Despite the rally, IAG trades at just 7.4 times forward earnings, marking a notable discount to US-listed peers. And with earnings growth of around 10% expected throughout the medium term, the stock appears to be trading with a price-to-earnings-to-growth (PEG) ratio of less than one. This would suggest that the stock continues to be undervalued as PEG ratio of one is the traditional benchmark for fair value. What’s more, the airline operator is expected to pay a dividend of around 2% in 2025 and 3% in 2026, adding to the notion that this stock is undervalued.

Moreover, bullish investors will point to IAG’s strong cash generation, supporting further debt reduction, and its dominant position in the transatlantic market. New fuel-efficient aircraft could also reduce costs by 10%-15% by 2026.

This has led to continually rising share price targets. While the stock only trades at a 10% discount to the average share price target, Deutsche Bank recently upgraded IAG to Buy, forecasting a 30% rise to their revised €5 price target.

Risks and alternatives

IAG’s business is flying, but that doesn’t mean there aren’t risks. The company remains exposed to shocks in fuel prices. Plus, the longer that Western airlines are banned from flying over Russia, the more likely that competitors will cement their positions within the market. Moreover, a stagnating UK economy, combined with additional National Insurance contributions, may also hurt margins.

Nonetheless, I’m continuing to hold IAG shares in my portfolio. I had considered buying more, but it’s grown to be a large part of my holdings. But I’ve actually bought shares in peer Jet2, which appears to be vastly undervalued.

While the global economy continues to be in a turbulent phase, Britain’s flagship FTSE 100index of leading shares has been doing well. This month, indeed, it hit a new all-time high.

So, would now be a good time for an investor to buy blue-chip UK shares?

Looking at individual trees, not the forest

The answer is potentially yes, no, and maybe!

An index of 100 shares contains shares that are doing well, ones that are doing badly, and some that are doing little of anything.

So, whether the FTSE 100 is at a high or low, individual shares within it may be overpriced or underpriced.

Hunting for bargains in today’s market

That explains why, in my opinion, the FTSE 100 still contains some bargains even after its recent strong performance.

So, how might an investor hunt for such a bargain?

My own approach is to stick to industries and companies I understand. I look for a business I think has a long-term sustainable competitive advantage in an area I expect to see ongoing strong customer demand.

As well as looking at that, I weigh up the balance sheet. I prefer not to invest in a firm that makes lots of profits but has to use them to service debt.

I also consider the valuation. A good business can be a bad investment if an investor overpays for its shares.

One UK share to consider

As an example of this approach in practice, one FTSE 100 share for investors to consider is Legal & General (LSE: LGEN).

The well-known financial services provider operates in a market that has high demand and I expect that will continue. Over recent years, it has become more specialised in retirement-linked financial services. I think that makes sense: it is a huge market with long-term demand.

Being seen more as a retirement expert than a generalist is a competitive advantage for the firm, in my opinion. Others include its strong, long-established brand and large customer base.

The business has been consistently profitable. The past several years have seen lower profits than in prior years, though.

Recently, it announced plans to sell a US business. In the short term that is good news. It could generate substantial cash that can be distributed to shareholders.

Longer term, however, it risks lower profits for Legal & General as well as tying its performance more closely than before to the UK economy.

I also see a risk that if the economy performs poorly, policy holders may take out more than they put in, hurting profits. Legal & General last cut its dividend during the 2008 financial crisis.

For now, though, the dividend continues to grow annually, and the current yield is 8.8%. No dividend is ever guaranteed to last, but that yield is well over double the FTSE 100 average.

Financial News

Daily News on Investing, Personal Finance, Markets, and more!