The Greggs share price is too tasty for me to ignore!

I have been eyeing shares in baker Greggs (LSE: GRG) for a while. After a big fall in the Greggs share price this week following the company’s results, I decided to make a move and buy.

Why I like the investment case

To start with, let me explain what attracts me to the company.

It operates in an area with high, resilient consumer demand. People always need to eat and Greggs is an affordable, convenient option for many.

As the business has grown, it has built economies of scale. For example, centralised production plants mean that much of the food prepping can be done in bulk at more efficient, lower-cost locations than the chain’s high street sites.

The business has been quite innovative when it comes to product launches. It now has an offering that includes some unique items. I see that as giving it a competitive advantage over rivals.

The results were good – or were they?

Looking at the double-digit percentage fall in the Greggs share price following the release of annual results, it would seem that they were poor. Many commentators seemed unimpressed with the performance.

Personally, though, I saw lots to like.

Sales revenues grew 11%, pre-tax profit was up 8%, and diluted earnings per share were 8% higher than a year before. The annual ordinary dividend per share was increased by 11%, meaning that the FTSE 250 share now offers a dividend yield of 3.9%.

Sales in company-managed stores grew more slowly than sales overall (some of the sales growth came from opening new shops) and this year has started with only modest sales growth.

On balance, though, I did not think that the results undermined the investment case.

Waiting for value, then pouncing

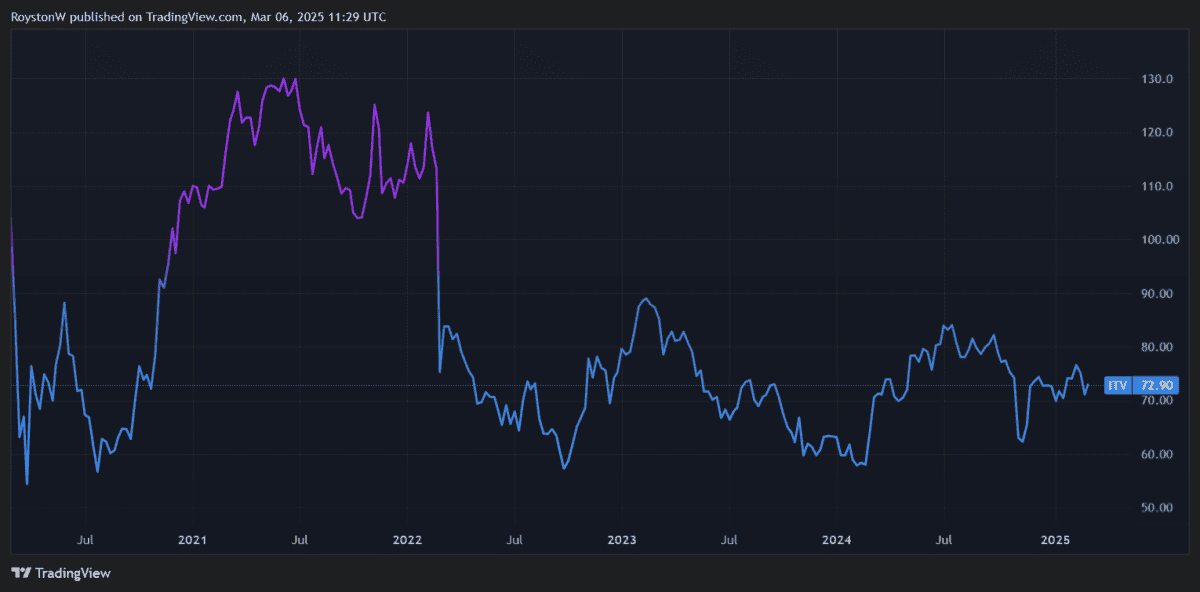

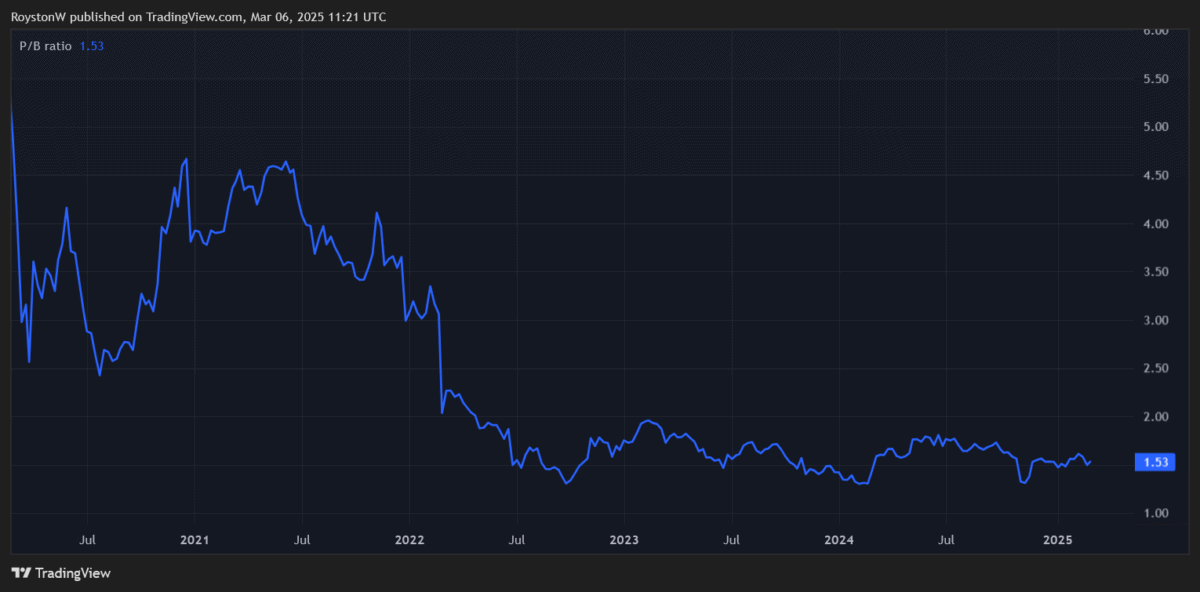

The current Greggs share price-to-earnings ratio is 12.

That is lower than it has been for a while and in my view looks like good value.

Sure, there are risks that help explain why the Greggs share price has been falling. Its cash pile fell last year. Costly capital expenditure requirements could continue to eat into it, as the chain keeps expanding its operations.

But when I look at the company I see a solidly profitably, cash generative business with a proven model and ongoing growth prospects.

I have been waiting a while for the share price to get to a level that I think offers an attractive buying opportunity. Now it has.

Like billionaire investor Warren Buffett, my stock market approach is to buy stakes in what I think are great businesses at attractive prices, with a view to holding them for the long term.

A tumbling Greggs share price has given me an opportunity to do just that – and I have seized it.