A general view of the GameStop logo on one of its stores in the city center of Cologne, Germany.

Ying Tang | Nurphoto | Getty Images

GameStop said Wednesday it has officially bought 4,710 bitcoins, worth more than half a billion dollars, as the video game retailer began its crypto purchasing plan in a similar move made famous by MicroStrategy.

The purchase, its first investment in bitcoin, was worth $512.6 million with bitcoin’s price of $108,837 Wednesday. The world’s largest cryptocurrency has been on a tear lately, hitting a record high near $112,000 last week, as easing trade tensions and the Moody’s downgrade of U.S. sovereign debt highlighted alternative stores of value like bitcoin.

Shares of GameStop rose nearly 3% in premarket trading following the news. The meme stock is up about 12% this year. As of February 1, the company had amassed a $4.76 billion cash pile, according to its annual report released in April.

CNBC first reported on GameStop’s intention to add cryptocurrencies on its balance sheet in February. The company confirmed its plan in late March, saying it has not set a ceiling on the amount of bitcoin it may purchase.

GameStop is following in the footsteps of software company MicroStrategy, now known as Strategy, which bought billions of dollars worth of bitcoin in recent years to become the largest corporate holder of the flagship cryptocurrency. That decision prompted a rapid, albeit volatile, rise for Strategy’s stock.

GameStop’s foray into cryptocurrencies marks the latest effort by CEO Ryan Cohen to revive the struggling brick-and-mortar business. Under Cohen’s leadership, GameStop has focused on cutting costs and streamlining operations to ensure the business is profitable.

Circle, the issuer of the popular USDC stablecoin, has launched its initial public offering, looking to raise about $624 million at a $5.65 billion valuation

The company plans to sell 24 million shares of Class A common stock at an expected price range of $24 to $26 apiece

Circle’s USD Coin (USDC) has roughly $62 billion in circulation, according to CryptoQuant, and its market cap has grown 40% this year.

Launched in 2018 by crypto firm Circle, USDC is now the second-biggest stablecoin globally, with more than $30 billion worth of tokens in circulation.

Nurphoto | Getty Images

Circle, the issuer of the popular USDC stablecoin, has begun its long-awaited initial public offering process, looking to raise about $624 million at a valuation around $6 billion.

The company, led by CEO Jeremy Allaire, said Thursday in a filing that it plans to sell 24 million shares of Class A common stock in total – 9.6 million to be sold by the company and another another 14.4 million by existing shareholders – at an expected price range of $24 to $26 apiece, which values the company at around $5.65 billion. Circle also said it will grant the underwriters a 30-day option to purchase up to 3.6 million additional shares.

Cathie Wood’s ARK Investment Management has indicated interest in purchasing up to $150 million of the shares, per the filing.

Circle’s USD Coin (USDC) has roughly $62 billion in circulation and makes up about 27% of the total market cap for stablecoins, behind Tether‘s 67% dominance, according to CryptoQuant. Its market cap has grown 40% this year, however, compared with Tether’s 10% growth.

The stablecoin sector specifically has been ramping up as the industry gains confidence that the crypto market will get its first piece of U.S. legislation passed and implemented this year, focusing on stablecoins. Last week, the Senate voted to advance the first crypto legislation, which would create a regulatory framework for stablecoins. Trump has said he wants to see crypto regulation on his desk and ready to sign by August before Congress goes into recess.

Circle’s IPO could have investment implications for Coinbase, a cofounder of USDC and major distribution vehicle for the stablecoin. The crypto services company and exchange has a 50% revenue sharing agreement with Circle and also makes 100% of the interest earned by USDC products on the Coinbase platform.

Historically, stablecoins have been used primarily for trading and as collateral in decentralized finance (DeFi), and crypto investors watch them closely for evidence of demand, liquidity and activity in the market. More recently, their ability to move dollars quickly and cheaply across borders has become more popular with banks and fintech companies.

Additionally, rhetoric around their ability to help preserve U.S. dollar dominance – by exporting dollar utility internationally and ensuring demand for U.S. government debt, which backs nearly all dollar-denominated stablecoins – has grown louder.

—CNBC’s Nick Wells contributed reporting

Don’t miss these cryptocurrency insights from CNBC Pro:

President Donald Trump could sign orders to support the nuclear industry as soon as Friday, sources told Reuters.

The orders would invoke the Defense Production and direct the Departments of Energy and Defense to help speed the construction of reactors.

Nuclear stocks are rallying in response.

Cooling towers are seen at the nuclear-powered Vogtle Electric Generating Plant in Waynesboro, Georgia, U.S. Aug. 13, 2024.

Megan Varner | Reuters

Nuclear power stocks surged Friday on a report that President Donald Trump will sign executive orders to speed the construction of reactors and secure key materials for the industry.

Advanced reactor companies Oklo and NuScale jumped about 8% premarket. Constellation Energy, the largest nuclear operator in the U.S., was up 2%. Cameco Corp., one of the biggest uranium miners in the world, rose more than 4%.

Trump could sign the orders as early as Friday, sources familiar with the matter told Reuters. The president is scheduled to sign orders in the Oval Office at 1 p.m. ET, according to the White House schedule.

Trump will invoke the Defense Production Act to declare a national emergency due to U.S. dependence on Russia and China for enriched uranium, nuclear fuel processing and inputs for advance reactors, according to a draft summary viewed by Reuters.

The president is also expected to direct federal agencies to permit and site new nuclear facilities, according to Reuters. He will also order the Departments of Energy and Defense to identify federal land and facilities where nuclear can be deployed and streamline the process to build them, Reuters reported.

Optimism on dealmaking appears to be back now that President Donald Trump has suspended his highest tariffs and market jitters take a backseat.

U.S. deal activity plunged by 66% to $9 billion during the first week of April, according to Mergermarket data, after Trump’s “liberation day” tariff announcement.

Activity is rebounding this month and larger deals are taking place.

People walk by the New York Stock Exchange (NYSE) on June 18, 2024 in New York City.

Spencer Platt | Getty Images

Hopes for an active year of mergers and acquisitions could be back on track after being briefly derailed by the Trump administration’s sweeping tariff policies last month.

Dealmaking in the U.S. was off to a strong start this year before President Donald Trump announced tariff policies that led to extremely volatile market conditions that put a chill on activity. In a pre-tariffs world, dealmakers were encouraged by the Trump administration’s pro-business flavor and deregulatory agenda, as well as previously easing concerns about inflation. Those trends were expected to fuel an even stronger M&A comeback in 2025, after last year’s moderate recovery from a slow 2023.

This year’s appetite for dealmaking came back quickly after Trump suspended his highest tariffs and market jitters took a backseat. If borrowing costs remain in check, many expect activity could be brisk.

“More clarity on trade policy and rebounding equities markets have set the stage for continued M&A, even in sectors hit especially hard by tariffs,” Kevin Ketcham, a mergers and acquisitions analyst at Mergermarket, told CNBC.

The total value of U.S. deals jumped to more than $227 billion in March, which saw 586 deals, before suddenly slowing down in April to roughly 650 deals worth about $134 billion, according to data compiled by Mergermarket.

So far this month, activity is rebounding and the average deal has been larger. More than 300 deals collectively valued at more than $125 billion have been struck this month as of May 20, Mergermarket said.

That’s encouraging. After Trump’s “liberation day” tariff announcement, U.S. deal activity plunged by 66% to $9 billion during the first week of April from the prior week, while global M&A activity dropped by 14% week over week to $37.8 billion, according to the data.

Charles Corpening, chief investment officer of private equity firm West Lane Partners, anticipates M&A activity to pick up after the summer.

“The trade war has indeed caused a slowdown in the anticipated M&A boom earlier this year, particularly in the second quarter,” Corpening said.

Higher bond yields are also hurting activity in the U.S. given that higher rates translate into greater financing costs, which reduces asset prices, he said.

Corpening expects greater interest towards special situations M&A, or deals that involve a motivated seller and tend to be flexible with their structure and terms, as well as smaller transactions, which are easier to finance and generally face less regulatory scrutiny.

“We’re beginning to see signs of recovery and we’re getting some clarity on the types of deals that are likely to get into the pipeline soonest,” Corpening said. “We anticipate that these earlier transactions will lean toward special situations as the better-performing businesses will wait for more market stability in order to maximize sale price.”

Several major deals have been announced in recent months, with large transactions occurring in tech, telecommunications and utilities so far this year.

Some of the biggest include:

According to Ketcham, the Dick’s-Foot Locker deal “likely isn’t an outlier” given that Victoria’s Secret on Tuesday adopted a “poison pill” plan. Such a limited-duration shareholder rights plan suggests the lingerie retailer is concerned about the threat of a potential takeover, he said.

Ketcham added that some consumer companies are adapting to the new macroeconomic environment instead of pausing dealmaking. He cited packaged food giant Kraft Heinz confirmation on Thursday that it has been evaluating potential transactions over the past several months as an example. Kraft Heinz said it would consider selling off some of its slower growing brands or buying a brands in some of its core categories such as sauces and snacks.

This kind of trend would lead to smaller deals, which has already been seen this year. For example, PepsiCo scooped up Poppi, a prebiotic soda brand, for $1.95 billion in March.

Empire Wind 1 will be the first offshore wind project to deliver electricity directly to New York City.

Interior Secretary Doug Burgum ordered construction on Empire Wind to stop on April 16, despite the fact that it had been approved in 2024.

New York Gov. Kathy Hochul said the White House has agreed to allow the project to move forward.

Burgum said he was encouraged Hochul’s willingness to move forward on natural gas pipeline capacity.

File: The wind farm in the Baltic Sea 35 kilometres northeast of Rügen is a joint venture of the Essen-based energy group Eon and the Norwegian shareholder Equinor.

Bernd Wüstneck | Picture Alliance | Getty Images

Norwegian energy company Equinor will resume construction on its offshore wind farm in New York, after the Trump administration lifted its order to halt work on the project.

Empire Wind 1 will be the first offshore wind project to deliver electricity directly to New York City. The Interior Department under the Biden administration approved the project last year after Equinor signed a lease issued by the Department of Interior in 2017.

But Interior Secretary Doug Burgum ordered construction on Empire Wind to stop on April 16, alleging that the Biden administration rushed the project’s approval “without sufficient analysis or consultation among the relevant agencies as relates to the potential effects.”

The stop work order had raised fears among investors that the White House might target other wind projects that had already been permitted and approved.

New York Gov. Kathy Hochul said Monday evening that Burgum and President Donald Trump agreed to lift the stop work order and allow the project to move forward “after countless conversations with Equinor and White House officials.” Empire Wind supports 1,500 union jobs, Hochul said.

Equinor said it aims to execute planned installation activities this year and minimize the impact of the stop-work order in order to reach its goal of starting commercial operations in 2027.

Apparent natural gas compromise

Burgum said he was encouraged by Hochul’s “willingness to move forward on critical pipeline capacity.”

“Americans who live in New York and New England would see significant economic benefits and lower utility costs from increased access to reliable, affordable, clean American natural gas,” the Interior Secretary said in a post on social media platform X.

Hochul did not mention natural gas in her statement, though she “reaffirmed that New York will work with the Administration and private entities on new energy projects that meet the legal requirements” under state law. New York has a history of opposing new natural gas pipelines.

Trump has targeted the wind industry, despite his agenda calling for the U.S. to achieve energy dominance. The president issued an executive order on his first day in office that barred new leases for offshore wind in U.S. waters and ordered a review of leasing and permitting practices.

Trump has a long history of attacking wind turbines dating back to at least 2012, arguing that they kill birds and cost more than they generate in revenue.

Empire Wind 1 started construction in the spring of 2024 and is more than 30% complete. Equinor has invested $2.5 billion in the project so far. The company is planning to build 54 turbines that are up to 910 feet tall. Empire Wind 1 will generate 810 megawatts of electricity, which is enough to power half a million homes, according to Equinor.

Equinor Chief Financial Officer Torgrim Reitan called the Trump administration’s order to stop work unlawful, extraordinary and unprecedented during the company’s first-quarter earnings call April 30.

“We have complied with this order. However, the order did not include any information about the alleged deficiencies in the approval,” Reitan said.

Three other offshore wind projects are under construction in the U.S. all located on the Eastern Seaboard. They are Revolution and Sunrise Wind in New England and Coastal Virginia Offshore Wind.

Dominion Energy is confident Coastal Virginia Offshore Wind will continue to move forward, CEO Robert Blue said on the company’s May 1 earnings call. It is 55% complete and will deliver electricity in early 2026, Blue said.

Orsted remains fully committed to Revolution and Sunrise Wind, CEO Rasmus Errboe said on the company’s May 7 earnings call. Revolution and Sunrise are about 75% and 35% complete respectively, Errboe said.

Volatile markets call for stability within portfolios, and investors are shopping for dividend stocks to provide a combination of upside potential and solid income.

While the U.S. and China’s recent agreement to slash tariffs for 90-days provided some relief to investors, the threat of steep duties under the Trump administration continues to be a concern.

Recommendations of top Wall Street analysts can help investors pick attractive dividend stocks that are supported by solid cash flows to make consistent payments.

This week’s first dividend pick is Chord Energy (CHRD), an independent exploration and production company with long-held assets primarily in the Williston Basin. The company recently reported solid results for the first quarter of 2025, which it attributed to better-than-modeled well performance, strong cost control, and improved downtime.

Chord Energy returned 100% of its adjusted free cash flow (FCF) to shareholders via share repurchases after declaring a base dividend of $1.30 per share. Based on the total dividend paid over the past 12 months, CHRD stock offers a dividend yield of 6.8%.

Calling CHRD a top pick, Siebert Williams Shank analyst Gabriele Sorbara reiterated a buy rating on the stock and raised the price target to $125 from $121. While no energy stock is immune to weaker commodity prices, Sorbara thinks that his top picks are best positioned on a relative valuation basis due to their attractive assets with low breakeven levels, strong free cash flow and the potential for superior capital returns.

In a research note following the results, Sorbara noted that the company reduced its 2025 capital expenditure outlook by $30 million, while maintaining its total production guidance, supported by improved operational efficiencies.

Nonetheless, CHRD is monitoring the macro situation and has the required operational and financial flexibility to further reduce activity if conditions remain unfavorable or weaken, emphasized the analyst. Further, Sorbara highlighted that Chord Energy reaffirmed its capital returns framework, targeting to return more than 75% of its free cash flow to shareholders through dividends and opportunistic share repurchases.

“We reaffirm our Buy rating on valuation, underpinned by its strong FCF yield providing the capacity for superior capital returns while maintaining low financial leverage (0.3x at the end of 1Q25),” said the analyst.

Sorbara ranks No. 143 among more than 9,500 analysts tracked by TipRanks. His ratings have been profitable 55% of the time, delivering an average return of 20.4%. See Chord Energy Hedge Fund Trading Activity on TipRanks.

Chevron

We move to oil and gas giant Chevron (CVX), which recently reported first-quarter results that reflected the impact of lower oil prices on its earnings. Chevron’s outlook indicated a slowdown in the pace of its stock buybacks in Q2 2025 compared to the prior quarter amid tariff woes and the decision of OPEC+ to boost supply.

Meanwhile, Chevron returned $6.9 billion of cash to shareholders during the first quarter through share repurchases of $3.9 billion and dividends of $3.0 billion. At a quarterly dividend of $1.71 per share (annualized dividend of $6.84 per share), CVX stock offers a dividend yield of 4.8%.

Following the Q1 results, Goldman Sachs analyst Neil Mehta trimmed his price target for Chevron stock to $174 from $176 and reaffirmed a buy rating. The analyst said that despite macro uncertainties and moderated stock buyback assumptions, he continues to see an attractive long-term value proposition in CVX stock, with about a 5% dividend yield.

“We additionally highlight expectations for strong free cash flow generation driven by major projects including Tengiz, US Gulf and the Permian,” said Mehta.

Regarding the Tengiz (Tengizchevroil or TCO) project, the analyst highlighted management’s commentary that it reached name-plate capacity ahead of schedule. The company reiterated expectations for robust cash flow generation from the TCO project, including cash distributions and fixed loan repayments. Mehta also noted that CVX remains constructive on the operating outlook in the Gulf of Mexico and expects to increase production in the region to 300,000 boe/d in 2026. About Permian, he stated that Chevron boosted production by about 12% in Q1, thanks to continued efficiencies.

Mehta ranks No. 535 among more than 9,500 analysts tracked by TipRanks. His ratings have been profitable 59% of the time, delivering an average return of 8.8%. See Chevron Ownership Structure on TipRanks.

EOG Resources

Finally, let’s look at EOG Resources (EOG), a crude oil and natural gas exploration and production company with proved reserves in the U.S. and Trinidad. Earlier this month, EOG reported market-beating earnings for the first quarter of 2025.

The company returned $1.3 billion to shareholders, including $538 million in dividends and $788 million via share repurchases. EOG declared a dividend of $0.975 per share (annualized dividend of $3.90 per share), payable on July 31, 2025. EOG stock offers a dividend yield of 3.4%.

In reaction to the Q1 results, RBC Capital analyst Scott Hanold reaffirmed a buy rating on EOG stock with a price target of $145. The analyst noted that the company announced macro uncertainty-led cuts to its activity plans, reducing the capital budget by 3% and organic oil production by 0.6%. Consequently, Hanold boosted his free cash flow (FCF) estimates by 6% to 7%.

The analyst highlighted that EOG is able to revise its planned activity by reducing activity in areas with ample scale, which would not slow or degrade its operational efficiencies. Hanold observed that in total, 550 wells (net) are now planned in the core U.S. onshore basins, which is 30 fewer compared to the original guidance.

Hanold pointed out that EOG again returned at least 100% of its free cash flow back to shareholders in Q1 2025. He expects this trend to continue, supported by the company’s balance sheet optimization strategy announced last year, current cash balance of about $7 billion and EOG’s stock price. “We expect management to flex buybacks to above 100% and think there is a path to over $1 billion resulting total returns at ~150% of 2Q25 FCF,” said Hanold.

Overall, the analyst views EOG as best positioned to handle the ongoing oil price volatility, backed by its best-in-class balance sheet, growing natural gas volumes and low-cost structure.

Hanold ranks No. 11 among more than 9,500 analysts tracked by TipRanks. His ratings have been successful 68% of the time, delivering an average return of 30%. See EOG Resources Insider Trading Activity on TipRanks.

President Donald Trump has ordered his Cabinet to find coal resources that can be used to power artificial intelligence data centers.

Miners argue that coal plants need to ramp up power generation to the meet the demand from data centers and maintain grid reliability.

The tech companies are unlikely to invest in new coal generation due to their climate commitments.

President Donald Trump wants to revive the struggling coal industry in the U.S. by deploying plants to power the data centers that the Big Tech companies are building to train artificial intelligence.

Trump issued an executive order in April that directed his Cabinet to find areas of the U.S. where coal-powered infrastructure is available to support AI data centers and determine whether the infrastructure can be expanded to meet the growing electricity demand from the nation’s tech sector.

Trump has repeatedly promoted coal as power source for data centers. The president told the World Economic Forum in January that he would approve power plants for AI through emergency declaration, calling on the tech companies to use coal as a backup power source.

“They can fuel it with anything they want, and they may have coal as a backup — good, clean coal,” the president said.

Trump’s push to deploy coal runs afoul of the tech companies’ environmental goals. In the short-term, the industry’s power needs may inadvertently be extending the life of existing coal plants.

Coal produces more carbon dioxide emissions per kilowatt hour of power than any other energy source in the U.S. with the exception of oil, according to the Energy Information Administration. The tech industry has invested billions of dollars to expand renewable energy and is increasingly turning to nuclear power as a way to meet its growing electricity demand while trying to reduce carbon dioxide emissions that fuel climate change.

For coal miners, Trump’s push is a potential lifeline. The industry has been in decline as coal plants are being retired in the U.S. About 16% of U.S. electricity generation came from burning coal in 2023, down from 51% in 2001, according to EIA data.

Peabody Energy CEO James Grech, who attended Trump’s executive order ceremony at the White House, said “coal plants can shoulder a heavier load of meeting U.S. generation demands, including multiple years of data center growth.” Peabody is one of the largest coal producers in the U.S.

Grech said coal plants should ramp up how much power they dispatch. The nation’s coal fleet is dispatching about 42% of its maximum capacity right now, compared to a historical average of 72%, the CEO told analysts on the company’s May 6 earnings call.

“We believe that all coal-powered generators need to defer U.S. coal plant retirements as the situation on the ground has clearly changed,” Grech said. “We believe generators should un-retire coal plants that have recently been mothballed.”

Tech sector reaction

There is a growing acknowledgment within the tech industry that fossil fuel generation will be needed to help meet the electricity demand from AI. But the focus is on natural gas, which emits less half the CO2 of coal per kilowatt hour of power, according the the EIA.

“To have the energy we need for the grid, it’s going to take an all of the above approach for a period of time,” Kevin Miller, Amazon’s vice president of global data centers, said during a panel discussion at conference of tech and oil and gas executives in Oklahoma City last month.

“We’re not surprised by the fact that we’re going to need to add some thermal generation to meet the needs in the short term,” Miller said.

Thermal generation is a code word for gas, said Nat Sahlstrom, chief energy officer at Tract, a Denver-based company that secures land, infrastructure and power resources for data centers. Sahlstrom previously led Amazon’s energy, water and sustainability teams.

Executives at Amazon, Nvidia and Anthropic would not commit to using coal, mostly dodging the question when asked during the panel at the Oklahoma City conference.

“It’s never a simple answer,” Amazon’s Miller said. “It is a combination of where’s the energy available, what are other alternatives.”

Nvidia is able to be agnostic about what type of power is used because of the position the chipmaker occupies on the AI value chain, said Josh Parker, the company’s senior director of corporate sustainability. “Thankfully, we leave most of those decisions up to our customers.”

Anthropic co-founder Jack Clark said there are a broader set of options available than just coal. “We would certainly consider it but I don’t know if I’d say it’s at the top of our list.”

Sahlstrom said Trump’s executive order seems like a “dog whistle” to coal mining constituents. There is a big difference between looking at existing infrastructure and “actually building new power plants that are cost competitive and are going to be existing 30 to 40 years from now,” the Tract executive said.

Coal is being displaced by renewables, natural gas and existing nuclear as coal plants face increasingly difficult economics, Sahlstrom said. “Coal has kind of found itself without a job,” he said.

“I do not see the hyperscale community going out and signing long term commitments for new coal plants,” the former Amazon executive said. (The tech companies ramping up AI are frequently referred to as “hyperscalers.”)

“I would be shocked if I saw something like that happen,” Sahlstrom said.

Coal retirements strain grid

But coal plant retirements are creating a real challenge for the grid as electricity demand is increasing due to data centers, re-industrialization and the broader electrification of the economy.

The largest grid in the nation, the PJM Interconnection, has forecast electricity demand could surge 40% by 2039. PJM warned in 2023 that 40 gigawatts of existing power generation, mostly coal, is at risk of retirement by 2030, which represents about 21% of PJM’s installed capacity.

Data centers will temporarily prolong coal demand as utilities scramble to maintain grid reliability, delaying their decarbonization goals, according to a Moody’s report from last October. Utilities have already postponed the retirement of coal plants totaling about 39 gigawatts of power, according to data from the National Mining Association.

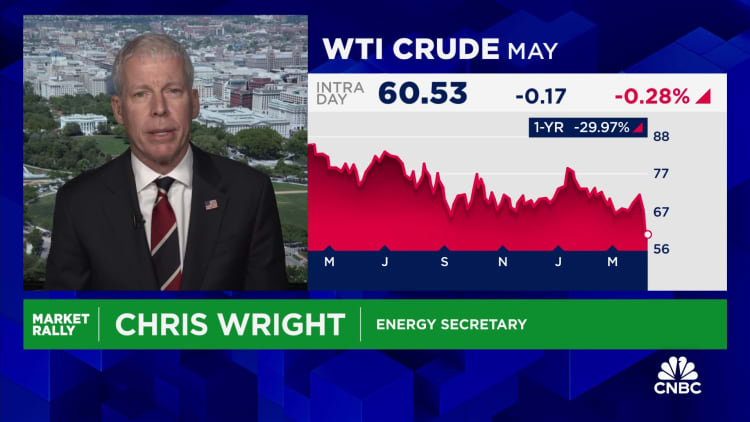

“If we want to grow America’s electricity production meaningfully over the next five or ten years, we [have] got to stop closing coal plants,” Energy Secretary Chris Wright told CNBC’s “Money Movers” last month.

But natural gas and renewables are the future, Sahlstrom said. Some 60% of the power sector’s emissions reductions over the past 20 years are due to gas displacing coal, with the remainder coming from renewables, Sahlstrom said.

“That’s a pretty powerful combination, and it’s hard for me to see people going backwards by putting more coal into the mix, particularly if you’re a hyperscale customer who has net-zero carbon goals,” he said.

The price of spot gold has surged more than 20% this year, with most of those gains coming in the first quarter.

Einhorn told CNBC’s Scott Wapner that his long-term case for gold is still intact and that the commodity can continue to go higher.

The comments came on the sidelines of the Sohn Investment Conference in New York, where Einhorn had earlier unveiled his new investment in a German chemical company.

A hot streak for gold helped fuel a strong start to the year for Greenlight Capital, and hedge fund manager David Einhorn said Wednesday he still sees more upside for the yellow metal.

The price of spot gold has surged more than 20% this year, with most of those gains coming in the first quarter. Einhorn, the president of Greenlight, told CNBC’s Scott Wapner that his long-term case for gold is still intact and that the commodity can continue to go higher.

“Gold is about the confidence in the fiscal policy and the monetary policy. And since we bought gold in 2008 or so, it’s been very clear to me that the U.S. fiscal and monetary policies are both too aggressive and create a risk,” Einhorn said.

Stock chart icon

Gold has outperformed stocks in 2025.

Einhorn pointed to the meager cost-cuts from the so-called Department of Government Efficiency, relative to the size of the federal government’s budget, as a sign that the fiscal situation is unlikely to change any time soon.

“There’s a bipartisan agreement to do nothing about the deficit until we actually get to the next crisis,” Einhorn said.

The hedge fund manager said that gold and other defensive positions have helped Greenlight have a strong start to the year. Reuters reported in April that Greenlight gained 8.2% in the first quarter, citing an investor letter. The S&P 500 fell more than 4% during the same period.

Einhorn did clarify that he does not view gold as an inflation bet. However, in a related trade, Einhorn said he has positions on long-duration inflation swaps, which serve as a bet that prices will rise faster than the market expects.

“All of these behaviors ultimately lead to inflation, and higher inflation,” Einhorn said.

The comments came on the sidelines of the Sohn Investment Conference in New York, where Einhorn had earlier unveiled his new investment in a German chemical company.

A logo of Meta is displayed during the Viva Technology startups and innovation fair at the Porte de Versailles exhibition center in Paris on May 22, 2024.

Julien De Rosa | Afp | Getty Images

The U.S. Federal Reserve recently announced its plan to keep interest rates steady, cautioning, “uncertainty about the economic outlook has increased further.” It noted that the risk of higher unemployment and elevated inflation have risen. Indeed, tariff wars have shaken global markets and knocked investor sentiment.

Nonetheless, investors looking for attractive picks amid the ongoing volatility can track the recommendations of top Wall Street analysts, who have the expertise to select stocks with the potential to thrive despite short-term challenges.

With that in mind, here are three stocks favored by the Street’s top pros, according to TipRanks, a platform that ranks analysts based on their past performance.

Meta Platforms

We start this week with Facebook and Instagram owner Meta Platforms (META), which surpassed analysts’ estimates for the first quarter of 2025, reflecting resilience in a tough macroeconomic backdrop. CEO Mark Zuckerberg said Meta is well-positioned to navigate any ongoing challenges.

In reaction to the strong Q1 print, JPMorgan analyst Doug Anmuth reiterated a buy rating on META stock and boosted the 12-month price target to $675 from $610, saying that Meta remains his firm’s top pick. Noting the company’s Q1 beat and Q2 outlook, Anmuth said he believed the company’s artificial intelligence (AI) ad enhancements, such as Andromeda and GEM, are having a significant impact on its ability to make money from the technology.

On the rise in Meta Platforms’ full-year capital expenditure guidance, the analyst said that he is OK with the increase, given that the company is delivering good results and tracking well on its AI roadmap. He added that Meta has a track record of generating returns on increased spending.

Anmuth said that AI is fueling huge early gains in Meta’s advertising and engagement, with the analyst expecting notable progress soon in business messaging/agents and Meta AI.

“We continue to believe that Meta is well positioned for a tougher macro environment given its scaled advertiser base, highly performant platform and vertical agnostic inventory,” Anmuth said.

Anmuth ranks No. 49 among more than 9,500 analysts tracked by TipRanks. His ratings have been profitable 62% of the time, delivering an average return of 20.1%. See Meta Platforms Options Activity on TipRanks.

Amazon

Anmuth is also bullish on e-commerce and cloud computing giant Amazon (AMZN). Following the company’s Q1 results, the analyst reaffirmed a buy rating on AMZN and raised the price target to $225 from $220. Amazon reported better-than-expected Q1 2025 results but issued soft guidance for the second quarter, citing tariff woes.

The analyst noted that the company’s Q1 revenue and operating income exceeded the higher end of prior guidance, while the second-quarter outlook reflected lower-than-feared macro and tariff-related impacts.

Though Microsoft’s Azure outperformed Amazon Web Services (AWS) in the March quarter and AWS is currently capacity-constrained, the analyst continues to believe that growth can move higher in the second half of the year as more supply comes online. He added that Amazon is not witnessing any visible change in demand.

Anmuth noted that the sequential deceleration in AWS revenue growth to 17% in Q1 2025 from 19% in the fourth quarter was offset by solid profitability. Notably, AWS’ operating margin touched an all-time high of 39.5% in the first quarter.

The analyst said that while Amazon did not discuss all its mitigation efforts related to suppliers and geographic sourcing of products, it has taken measures to pull forward inventory because of the tariff wars.

“Importantly, AMZN remains focused on broad selection, low pricing and fast delivery, and believes it typically emerges from uncertain macro periods with greater relative market share gains,” said Anmuth. See Amazon Insider Trading Activity on TipRanks.

Roku

Finally, let’s look at Roku (ROKU), a maker of streaming devices and other products, and a distributor of streaming services. While Roku delivered a modest revenue beat and reported a narrower-than-anticipated loss per share for the first quarter, shares declined as the company trimmed its full-year revenue outlook and issued lower-than-expected Q2 revenue guidance.

Wedbush Securities analyst Alicia Reese highlighted that while Roku lowered its 2025 revenue outlook, it maintained Platform revenue and adjusted EBITDA guidance, crediting enhanced profit from its initiatives and anticipated revenue from acquiring Frndly TV. Roku last week agreed to buy Frndly TV, an affordable subscription streaming service that offers live TV, on-demand video, and cloud-based DVR (Digital Video Recorder), for $185 million in cash in a deal espected to close in the second quarter.

Despite the impact of macroeconomic challenges, Reese believes that Roku is well-positioned within the relatively safe connected TV industry owing to increasing diversification of platform revenue. The analyst also highlighted that a more diversified business model is helping Roku deliver consistent results.

Reese thinks that investors will appreciate Roku for its balanced approach as it grows internationally, improves its platform and enhances The Roku Channel’s ad capabilities, while focusing on expense discipline to drive free cash flow.

“We expect Roku to benefit from its DSP (demand-side platform) partnerships, high-quality inventory, improved targeting sports-adjacent ads, and various price points across its platform to meet advertisers’ needs,” said Reese, reiterating a buy rating on ROKU stock with a price target of $100.

Reese ranks No. 830 among more than 9,500 analysts tracked by TipRanks. Her ratings have been profitable 61% of the time, delivering an average return of 14.5%. See Roku Ownership Structure on TipRanks.

Brian Armstrong, CEO and Co-Founder, Coinbase, speaks during the Milken Institute Global Conference on May 2, 2022. in Beverly Hills, California.

Patrick T. Fallon | AFP | Getty Images

Coinbase CEO Brian Armstrong said the crypto platform aims to become one of the biggest financial services companies in the world in a few years, aided by traditional players who continue adopting crypto at an accelerating rate.

Asked on the company’s call with analysts this week if Coinbase plans to enter traditional finance, Armstrong said that rather than look backward, he “wants to look forwards and skate to where this opportunity is going.”

“Today, we’re primarily focused on trading and payments … across our major customer groups: retail, small [and] medium sized businesses, institutions and developers,” Armstrong said on the quarterly earnings call Thursday.

“In five- to 10 years, our goal is to be the number one financial services app in the world across those customer segments because we believe that crypto is eating financial services, and we are the number one crypto company,” he added. “All these asset classes – money market funds, real estate, securities, debt – these are all coming on chain.”

Expanding platform

Coinbase operates primarily as a cryptocurrency exchange. Over the years it has added other products and services focused on non-trading aspects of crypto for retail and institutional users alike – including payments via stablecoins, rewards through stablecoins and staking and custody for institutions. BlackRock, Stripe and PayPal are among more than 200 institutional customers for those services.

As the Trump administration loosens regulatory constraints on crypto and Congress stands on the verge of passing stablecoin legislation later this year, traditional institutions have shown more interest in expanding into crypto-related services. In February, Bank of America CEO Brian Moynihan said the Charlotte-based lender could introduce a stablecoin if regulation allows.

“We think that every major bank is going to be integrating crypto at some point … it’s technology to update the financial system,” Armstrong said. “We can power a variety of things for them. [For] some of them, it’s a custodial solution. Others are interested in having a stablecoin solution.”

“We’ve seen some interest where banks and other companies will want to create their own stablecoin,” he continued. “Our view is that that’s not necessarily the best path because stablecoins have network effects. You want interoperability with other financial institutions to be able to settle payments and do all kinds of things.”

Biggest driver

Stablecoins have become Coinbase’s biggest driver of revenue after trading. In the first quarter, revenue tied to stablecoins soared 50% from the year-earlier period and 32% from the fourth quarter. Coinbase is a cofounder of the popular USDC stablecoin, has a 50% revenue sharing agreement with issuer Circle and also makes 100% of the interest earned by USDC products on the Coinbase platform.

Armstrong has said Coinbase has a “stretch goal” to make USDC the number 1 stablecoin in the world, a position ccurrently held by Tether’s USDT.

“If you can get shared economics, I don’t see why we wouldn’t see more of these banks partnering with USDC,” Armstrong said. “Regardless, we at Coinbase can help power infrastructure for all these folks that are coming into the industry … that’s a big part of our plan.”

Don’t miss these cryptocurrency insights from CNBC Pro:

Financial News

Daily News on Investing, Personal Finance, Markets, and more!