Time is running out for luxury watch collectors to get their hands on this coveted timepiece.

Luxury watchmaker Patek Philippe announced the final release of its popular Nautilus Ref. 5711 watch in a limited series with Tiffany & Co. on Monday.

The series will be limited to 170 timepieces running at almost $53,000 apiece in honor of the 170-year partnership between the Swiss watchmaker and the American jeweler.

The partnership started in 1851, when Antoine Norbert de Patek and Charles Tiffany met in New York. Tiffany signed an agreement with Patek Philippe in 1854 to become the first retailer in America to carry the exclusive timepieces. And the agreement has survived numerous ownership changes over the years, including Tiffany being acquired by the French luxury giant LVMH for $15.8 billion in January 2021.

The Nautilus Ref. 5711, first introduced in 2006, sprung to fame through social media influencers and celebrity watch enthusiasts flaunting the exclusive wrist trophy. But in January 2021, Patek Philippe announced that it was ending production of the Ref. 5711, saying the demand was overwhelming. So this limited-edition collection could be the last chance for Nautilus lovers to get their hands on one.

The Nautilus was always intended to be a status symbol. When the first model was released in 1976, it cost $3,100 — an enormous price for a steel watch at the time.

Here are the previous limited editions that Patek Philippe made for Tiffany: 2001 — Refs. 5150R, 5150J & 5150G – 450 watches 2009 — Refs. 4987G-001 & 4987G-010 – 100 watches 2012 — Refs. 4987G-001 & 4987G-010 – 50 watches 2012 — Ref. 5396G-012 – 100 watches

Today, the Nautilus usually sells for $34,890. But the new model — which will feature stainless steel and a Tiffany Blue dial — will be sold for $52,635 at Tiffany stores in New York, San Francisco and Beverly Hills.

In recent years, Tiffany has tried to attract younger consumers by collaborating with brands a lot younger than Patek Philippe, such as the streetwear maker Supreme.

Shares of Hertz Global Holdings Inc. surged Monday after JPMorgan recommended investors buy, citing strong industry tailwinds and a number of company-specific drivers that make the car rental company more attractive than its close peer, Avis Budget Budget Group Inc.

Analyst Ryan Brinkman at JPMorgan initiated Hertz at overweight and set a $30 stock price target, which implies about 16% upside from current levels.

Brinkman gave a number of reasons for his bullish stance on Hertz:

“A number of very strong industry and macro tailwinds,” including the “unprecedentedly strong” used vehicle pricing backdrop and supply/demand imbalance affecting rental cars, both with are products of the pandemic and its aftermath.

The above tailwinds are expected to “subside only gradually” over the next 12-to-18 months, as there is no quick or easy solution to the global semiconductor shortage that is holding back light vehicle production.

“A multitude of recently announced company specific initiatives,” including new partnerships with American Express Co. AXP, +3.66%,

Tesla Inc. TSLA, -0.74%,

Uber Technologies Inc. UBER, +6.89%

and Carvana Co. CVNA, +0.77%.

Those initiatives should help mitigate the eventual subsiding of macro tailwinds.

“A fully refreshed post-bankruptcy capital structure,” which features less corporate debt and substantially more liquidity, which reduces risk.

“What we see as relative value in comparison to shares of close peer Avis Budget,” which also benefits from the same macro factors as Hertz but trades at a “materially higher” valuation multiple.

Hertz’s stock has soared 56.6% over the past three months, including the time when it traded over the counter. But Avis Budget shares CAR, +3.11%

have nearly tripled over the same time, rocketing 194.4%, after they got the meme treatment in the wake of strong third-quarter results, which followed a big jump in bearish bets on the stock. For context, the S&P 500 index SPX, +1.35%

has edged up 1.6% the past three months.

Brinkman rates Avis Budget at underweight with a price target of $225, which is 17% below current levels.

FactSet, MarketWatch

Brinkman wasn’t the only analyst with a bullish call on Hertz on Monday. Deutsche Bank’s Chris Woronka reinstated coverage, following a period of restriction, with a buy rating and $34 stock price target.

That target, which implies 31% upside from current levels, makes Woronka Wall Street’s most bullish analyst on Hertz of the seven analysts surveyed by FactSet who cover the company.

Woronka said his buy rating was a “relative valuation call, above all else,” as he rates Avis Budget at sell.

“In our view, the current valuation gap between the two companies is illogically wide,” Woronka wrote.

Woronka said that while Hertz recently announced a $2 billion stock repurchase program, which at the time it was announced represented about 18% of the company’s market capitalization, he believes it is “highly unlikely” that Avis Budget is currently buying back stock given how much prices have run up following third-quarter results.

“Our sense is that it will likely take some time for many investors to reengage on the [Hertz] story, given that the stock was trading off of the major exchanges for nearly 18 months and the company was unable to be visible with the investment community,” Woronka wrote. “That said, the potential ability to broaden out the investor base in light of a larger market cap and forward-looking growth initiatives that can appeal to multiple investor groups, should be viewed as a positive catalyst.”

Securities and Exchange Commission Chairman Gary Gensler, and other regulators, want some details on the so-called “Trump SPAC.”

Digital World Acquisition Corp. DWAC, -3.16%,

the blank-check company looking to take Donald Trump’s startup media company public, closed on $1 billion in private equity funding over the weekend according to a Monday SEC filing, but the company also disclosed that it is under investigation by federal regulators who want to know about trading activity and communications centered around DWAC and the announcement of its plans to merge with Trump Media & Technology Group back in October.

In the weeks after that wild spike, reports surfaced that DWAC’s founder –Florida and Wuhan, China-based financier Patrick Orlando—had met with Trump early in 2021, well before DWAC’s listing on Sept 2. If the two did plan to take TMTG public via DWAC and didn’t disclose that information to investors, that would be a violation of securities regulations governing blank-check companies.

“It’s really not a surprise given all the media coverage of the SPAC and the way it traded,” said James Angel, a professor, at Georgetown University’s McDonough School of Business.

“When the SPAC goes public, it’s supposed to make full disclosure,” explained Angel. “If they went public without telling investors they’d been talking to Mr. Trump, then a regulator might have to ask some questions.”

According to Monday’s filing, the SEC requested “documents relating to meetings of DWAC’s Board of Directors, policies and procedures relating to trading, the identification of banking, telephone, and email addresses, the identities of certain investors, and certain documents and communications between DWAC and TMTG.”

But the filing also made it clear that “the investigation does not mean that the SEC has concluded that anyone violated the law or that the SEC has a negative opinion of DWAC or any person, event, or security.”

For at least one securities lawyer, that clarification seemed amiss.

“What the SEC is asking for; trading info, names of investors, calls with Trump, seems pretty detailed and specific,” said Francis Curran, a securities litigation attorney at Kudman Trachten Aloe Posner.

Monday’s filing was ostensibly about DWAC announcing that it had raised another $1 billion through a private investment in public equity deal, often referred to using the acronym PIPE. For SPACs, PIPEs are a way to raise more private capital.

For DWAC, the new funding means that instead of its announced deal to take the former president’s not-yet-launched media brand onto the public markets at an $875 million valuation, it will now be doing do at around $3 billion.

But the probes into DWAC also raise a larger question about its choice of TMTG, a company that –despite the promise of leveraging Trump’s brand to create a “non-woke” alternative media empire—is preparing to enter the public market without any concrete revenue-generating products at a $3 billion valuation.

“At this point, it’s vaporware,” Angel said of TMTG. “But our ex-president does have a certain amount of popularity in this country and some very real media savvy. This is a question of how much the Trump brand can be monetized.”

Based on how quickly DWAC and TMTG managed to get $1 billion raised for the PIPE, the answer seems to be that the brand can be monetized a lot, and it doesn’t seem like Gensler would have any recourse to stop the deal other than delaying the listing with more questions.

“One hundred years ago, this would have been a Blue Sky Law,” said Curran, referring to the early 20th century, state-by-state regulations designed to protect investors from fraud in the speculative frenzy that led up to the 1929 market crash.

For Angel, however, the controversial merger between DWAC and TMTG isn’t so much a new frontier in regulatory activism but an acknowledgment of a very American tradition.

“One of the beautiful things about the American system is that the way we head off actual corruption is to make it so easy for you to make money when you leave office,” he opined. “This is Mr. Trump’s big chance to cash out on his presidency.”

DWAC shares were trading down more than 2% at midday Monday.

Electronic Arts Inc. ticked higher Monday after one analyst upgraded the videogame publisher on the basis that risks were already priced in to the stock as the industry navigates a turbulent quarter.

EA EA, +0.99%

shares, which were up as much as 2% Monday, have declined 14% over the past three months. In comparison, Activision Blizzard Inc. stock ATVI, +0.65%

has suffered a 29% drop over that period and Take-Two Interactive Software Inc.’s stock TTWO, -1.37%

has gained 1%.

Citi Research analyst Jason Bazinet upgraded EA to a buy from a neutral rating but scaled back his price target to $150 from $160 in that “most of the downside risk may be priced into the equity at current levels.”

“We attribute most of the recent declines in the equity to concerns surrounding the company’s release of Battlefield 2042, as the title has been met with (mostly) negative reviews since the mid-November release,” Bazinet said.

“However, we believe concerns surrounding the company’s dispute with FIFA over its license renewal, potential IDFA headwinds, and concerns over a tougher Chinese regulatory environment may also be weighing on the equity,” the Citi Research analyst added.

Meanwhile, Benchmark analyst Mike Hickey notes that EA developer Dice has sent out satisfaction surveys to gamers trying “to find out what needs improving” with Battlefield 2042.

That follows news on last week that Vince Zampella, co-founder of Apex Legends and Titanfall developer Respawn Entertainment, would oversee the Battlefield franchise going forward, and that Dice head Oskar Gabrielson was leaving the studio.

Of the 30 analysts who cover EA, 22 have buy ratings and eight have hold ratings, along with an average price target of $174.20, according to FactSet Research.

A diplomatic boycott would involve the U.S. not sending any official representatives or diplomats to China to watch the Olympics, but would still allow American athletes to compete.

“The athletes on Team USA have our full support,” Psaki added.” We will be behind them 100% as we cheer them on from home.”

Prior to the announcement by the White House, China said a U.S. diplomatic boycott would be “outright political provocation,” and threatened to take “firm countermeasures” if the U.S. staged a diplomatic boycott of the Beijing Games.

Rep. Al Lawson (D-FL) recently proposed a piece of Social Security legislation, which has been scored by SSA’s Office of the Chief Actuary. The Lawson proposal is the second major Social Security bill in a month. following Rep. John Larson’s (D-CT) Social Security 2100: A Sacred Trust.

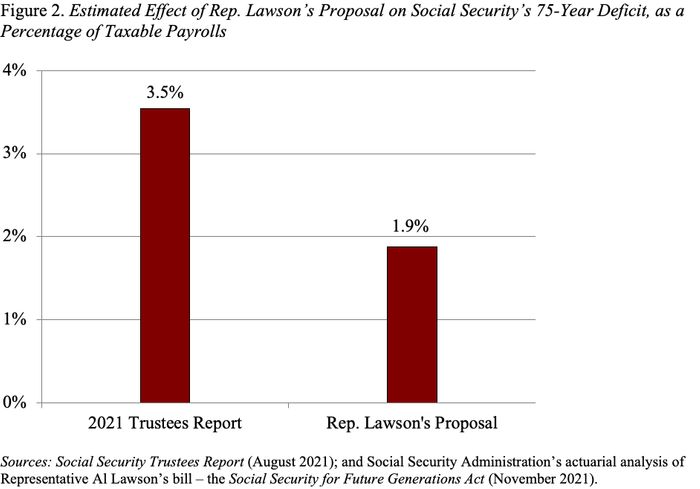

As a reminder, the Social Security actuaries project a program deficit over the next 75 years of 3.54% of taxable payrolls. This deficit reflects the combination of rising costs and constant levels of income (see Figure 1). The increasing costs are the result of a slow-growing labor force and the retirement of baby boomers, which raises the ratio of retirees to workers. Social Security’s deficit can be eliminated either by bringing up the income rate and/or lowering the cost rate.

Both the Lawson and Larson bills maintain current benefits — that is, they do not reduce the cost rate. Instead, they raise the income rate by lifting the cap on maximum taxable earnings. The area where the two bills differ the most is benefit enhancements. Whereas the Larson bill proposes a dozen enhancements for a five-year period, the Lawson bill offers four enhancements on a permanent basis.

Use the Consumer Price Index for the Elderly (CPI-E), which historically has risen faster than the CPI-W price index currently used for Social Security, to adjust benefits for inflation.

Extend student benefits up to age 23 if full-time students.

Increase the special minimum benefit for workers with very low earnings and index it by the growth in average wages.

Establish an alternative benefit for surviving spouses equal to 75% of the couple’s benefit (subject to an upper limit).

To pay for these benefit enhancements and, more important, to reduce the 75-year deficit, the Lawson legislation would apply the payroll tax on earnings above $250,000 and on all earnings once the taxable maximum reaches $250,000. The legislation would apply a 2% benefit factor on average earnings above the current law maximum.

Enactment of these benefit and revenue provisions would cut Social Security’s long-range deficit roughly in half, from 3.54% of taxable payroll to 1.88% (see Figure 2).

Both bills have some favorable aspects: they maintain current benefits and they raise additional revenues, although at least the Larson bill appears limited in the revenue-raising efforts by President Biden’s pledge not to raise taxes on households earning less than $400,000.

In terms of benefit enhancements, both “spend” a lot of future revenue switching from the CPI-W to the CPI-E for indexing benefits. Personally, I wouldn’t bother. The other benefit changes in the Lawson bill are relatively small and positive. Most important, they are permanent, avoiding the chaos likely to be created by the temporary enhancements in the Larson bill.

In the end, however, any solution is likely to involve a modest increase in the payroll tax rate, a change that would raise taxes on those with less than $400,000.

Americans have long devoured more than their fair share of the Italian favorite. But pizza sales skyrocketed during the pandemic for a variety of reasons. And while the fervor may have leveled in recent months — industry giant Domino’s DPZ, -0.50%

recently reported a slight sales dip, according to The Wall Street Journal, after seeing notable gains in 2020 — some pizza businesses say they find themselves on solid ground and looking to expand.

Even Google GOOGL, +1.22%

is getting in on the pizza game — literally. On Monday, the internet search giant unveiled a pizza-themed interactive challenge as part of its regular series of Google Doodles. Google officials explained that it was tied to the fourth anniversary of UNESCO, the United Nations organization, recognizing the art of Italian pizza-makers as part of the world’s “intangible cultural heritage.”

But pizza is not just about heritage. It’s about big business.

Just ask Brandon Hoy, one of the owners of Roberta’s, an acclaimed, New York City-based pizza establishment that is growing in several directions. Hoy said his company’s sales have been strong during the pandemic — in particular, sales of Roberta’s line of frozen pizzas nearly doubled in 2020. In addition, Roberta’s has opened new locations everywhere from New York to Nashville, with plans to add more in the coming years.

“The marketability of pizza is so huge,” said Hoy.

Others in the industry are similarly bullish. Little Caesar’s, the national chain, recently said it was looking to add more than 100 locations. “The pizza industry is obviously doing quite well, so we’ve taken advantage of that,” said Craig Sherwood, the chain’s vice president of U.S. development, in an interview with QSR, a trade publication for the restaurant industry.

There’s no real mystery as to why pizza is popular, culinary professionals and experts say. It’s a food item that has an intrinsic appeal and checks what restaurant-industry consultant Stephen Zagor calls the three 3 C’s for food-business success — namely, it’s cheap, comforting and convenient.

Moreover, Zagor says it’s an item that’s easily adaptable in terms of different toppings — Thanksgiving pizza, anyone? — or regional approaches.

“There’s an incredible canvas for creativity,” said Zagor.

Consider just one trending pizza style — the Detroit pie, with cheese that goes all the way to the crust. It’s now offered throughout the country. Pizza Hut YUM, +4.41%,

another industry giant, has put it on its menu as well.

Pizza establishments did especially well during the pandemic, culinary pros say, for one basic reason: These businesses were adept at offering delivery and takeout for many years prior to the health crisis. So, when the pandemic prompted more consumers to order from home, pizzerias were able to easily rise to the challenge.

“They didn’t have to reinvent the wheel. They already had the platform and the technology,” said Arlene Spiegel, a New York-based restaurant consultant.

When kids 5 to 11 arrive at a movie theatre, after-school sports leagues or an indoor restaurant in New York City, they’ll have to show proof that they’ve received at least one dose of Pfizer-BioNTech’s PFE, -4.03%

BNTX, -16.52%

COVID-19 starting Dec. 14, the city’s Mayor Bill de Blasio announced on Monday.

So far more than 125,000 children in New York City ages 5 to 11 have already received at least one dose, according to the city’s Department of Health. Nationally, nearly 5 million kids in that age group have received at least one dose, according to data published by the U.S. Centers for Disease Control and Prevention.

On Monday, de Blasio also announced the first city-wide vaccine mandate for all private employers, which will take effect on Dec. 22.

Even before de Blasio made the vaccine mandate announcement, some parents jumped at the opportunity to vaccinate their kids.

Samantha Levin, pictured, with her two children after they got their first doses of Pfizer’s COVID-19 vaccine on Nov. 8.

Elisabeth Buchwald

Samantha Levin, a New York City mother of a six-year-old son and a 10-year-old daughter, told MarketWatch on Nov.8 that getting her children vaccinated “means freedom.”

“They don’t get quarantined anymore in school,” Levin said outside of the Natural History Museum, which is being used as a city vaccination site.

Immediately after CDC gave its official stamp of approval for kids to start getting vaccinated against COVID-19 on Nov. 2, San Francisco health officials announced that 5 to 11-year-olds would soon be required to show proof of vaccination for indoor activities.

That wouldn’t take effect until the beginning of next year, at the earliest so that children have ample at least two months to get vaccinated, San Francisco Health Officer Dr. Susan Philip said last month.

Kids 5 and up will also be required to submit proof of vaccination or a negative COVID-19 test taken 72 to 24 hours before boarding a Disney Cruise DIS, +2.85%

starting Jan. 13.

Hydrogen fuel manufacturer Plug Power Inc. PLUG, +2.24%

will build a new “green energy technology facility” at a currently vacant site in Genesee County, with the intention of creating 68 new jobs. The company is expected to invest millions in the area, while receiving many millions in tax breaks and reduced electricity costs.

“This is extremely expensive,” said Greg LeRoy, executive director of Washington, D.C.-based Good Jobs First, which maintains a “Subsidy Tracker” that follows taxpayer dollars flowing to corporations.

Genesee County is sandwiched between Rochester and Buffalo, and the site where the plant will sit is approximately 35 miles from Niagara Falls. In an interview with MarketWatch, LeRoy also noted the “tragedy” of giving so much of the area’s electricity to one company. “You’re limiting the benefits, which is risky because you’re creating a disincentive for companies to become more energy efficient, and you’re not distributing the benefits broadly.”

In contrast, Jim Krencik, spokesperson for the Genesee Country Economic Development Center, says the project enjoys broad community support and will bring big regional benefits, including well-paying professional jobs that may attract additional employers to the area. Krencik said some of those positions could pya roughly $70,000 annually, about $25,000 more than the area’s average salary, and include benefits.

The Rochester Institute of Technology and the University of Buffalo turn out nearly 10,000 STEM graduates every year, Krencik told MarketWatch. Historically, “upstate New York is an exporter of talent to the semiconductor industry and to precision manufacturing.”

Plug Power’s investments in the region, including spending $55 million on a power substation, will likewise attract other companies, Krencik predicts. “These are incentives, these are advantages that play into the region’s strengths.”

Plug Power did not respond to multiple requests for comment for this article.

Credits: Genesee County Chamber of Commerce, Genesee County Economic Development Center

In contrast to boondoggles like Wisconsin’s Foxconn deal, the Genesee County deal has “at least a little thought and strategy put into it,” said John Buhl, a spokesperson for the nonpartisan Tax Policy Center in Washington. In the once-Trump-heralded Wisconsin deal, the Taiwan electronics manufacturer by early 2021 had slashed its planned investment to $672 million from $10 billion and cut the number of new jobs to 1,454 from 13,000.

The Plug Power partnership taps resources from the local and state level, and the public and private sectors, Buhl noted, and it’s part of “a broader strategy to build out a green-energy area.”

Still, local “good-government” advocates, like Tom Speaker of Reinvent Albany, are skeptical. The facility where Plug Power will locate its plant, the Western New York Science & Technology Advanced Manufacturing Park, has been in the works for over a decade.

“They’ve invested millions into the site and just have not managed to lure many companies to the area,” Speaker told MarketWatch. “Our view is that these types of subsidies don’t ultimately benefit New York’s economy and that much better things could be done with the money that’s being dedicated.”

How exactly to evaluate the usefulness of public subsidies remains an open question.

“With these kinds of incentives there’s always tradeoffs,” said the Tax Policy Center’s Buhl. “Just looking at it as a pure job creation opportunity, it’s not a home run.”

Among economic development analysts, a claim of $1 back for every $1 spent is “normal, 2:1 is good, anything beyond that you’d have to question the methodology,” he added. That makes this project’s claims of a 4.3:1 ratio “a little high.”

“The goal of any incentive project is to get economic activity that wouldn’t have come otherwise, but it’s not either/or most of the time,” Buhl said. “They often have some amount of talent locally, but bring in some as well.”

LeRoy, of Good Jobs First, agrees. “Cost-benefit analysis in economic development in America is the wild, wild west.”

“The only honest comparison is public dollars in versus public dollars back. But the problem is, people give exaggerated answers back. None of those are valid. The state doesn’t tax 100% of payroll or capital spending.”

The best way to spur economic development in an area isn’t always by attracting companies, LeRoy said. It may mean fostering “a cluster of” start-ups, knowing that some will survive and some will not. Or it could involve tapping existing state programs for distribution of energy, developing stronger ties with local universities, and so on. Those are the strategies that have helped create the “Research Triangle” in Raleigh-Durham, North Carolina, the biotech ecosystem of Cambridge and Boston, Massachusetts, and others.

That’s the vision Genesee County officials seem to have for the facility where Plug Power will locate. This “is a big project, no doubt about it,” Krencik said. “We’re optimistic that these assets are very attractive.”

Optimism continues to build for Micron Technology Inc., with a Cowen & Co. analyst dubbing the stock his “best idea” among large chip stocks heading into next year.

Cowen’s Karl Ackerman thinks that investors are misunderstanding Micron’s MU, +0.98%

story. While DRAM spot prices have been falling, channel inventory is improving, according to Ackerman. Perhaps more important, Micron now derives about 75% of its business from long-term agreements, he said, compared with 20% four years ago, which makes the company less beholden to changes in spot prices.

Long-term agreements “coupled with more stable supply should lessen historical cycle volatility and drive more predictable growth,” Ackerman wrote, while boosting his price target on Micron’s stock to $99 from $80 and maintaining an outperform rating.

Micron’s stock rallied 1.0% in midday trading Monday. While it has lost about 14% from its 21-year high of $95.59 reached on April 12, 2021, it has surged 24% since closing at a one-year low of $66.38 on Oct. 13.

Ackerman also disagrees with what he says is another bearish argument on Micron shares—that memory could lag in 2022 if the semiconductor industry is “driven by inventory restocking.” He is more bullish, writing that memory integrated circuits are becoming more critical to data centers, automotive applications, and networking system architectures. Growth in those categories has helped memory companies boost their share of semiconductor industry demand.

The FactSet consensus is still ahead of Ackerman’s new fiscal 2022 earnings estimate of $8.22 a share, but he said that some buy-side expectations call for earnings as low as about $6.75 to $7.00 a share, which he considers “too pessimistic.” The FactSet EPS consensus for fiscal 2022 is $8.80. Micron’s stock has the potential to outperform the broader semiconductor industry during calendar 2022, in Ackerman’s view.

Ackerman joins Evercore ISI analyst C.J. Muse, who tapped Micron as a semiconductor “top pick” a few weeks back, pointing to “green shoots” in the memory sector as well as opportunities for Micron to play into hot themes like the build out of the metaverse.

Micron shares have gained 13.0% over the past month, while the PHLX Semiconductor Index SOX, -0.84%

has edged up 0.2% and the S&P 500 SPX, +1.39%

has declined 2.2%.

Financial News

Daily News on Investing, Personal Finance, Markets, and more!