Of the many forms you can expect to complete when applying for an SBA loan, SBA Form 413—also referred to as the “SBA personal financial statement”—is one of the most essential. This form factors into how the SBA determines your ability to repay an additional debt and, by extension, your eligibility for an SBA loan.

Although at first glance, SBA Form 413 may seem intimidating, it becomes much more manageable when you break it up into individual steps.

In this guide, we’ll walk you through the SBA personal financial statement—explaining what is needed for each section and ultimately, how to complete the form for your SBA loan application.

What is SBA Form 413?

SBA Form 413, also called the “personal financial statement,” is a required document in applying for most of the SBA loan programs. In short, the SBA uses this form to evaluate your personal finances and determine your ability to repay a potential loan.

At the top of Form 413, the SBA writes: “SBA uses the information required by this Form 413 as one of a number of data sources in analyzing the repayment ability and creditworthiness of an application for an SBA guaranteed 7(a) or 504 loan or, with respect to a surety bond, to assist in recovery in the event that the contractor defaults on the contract.”

So, if you’re applying for a business loan, you might be wondering why the SBA is interested in your personal finances.

According to Alex Goldklang, a strategic sales lead at Fundera, “The SBA needs to look at your business’s debt service coverage ratio (DSCR) as well as your global DSCR, and your personal finances factor into your global DSCR. To be approved for an SBA loan, you need to pass both.”

Put simply, these metrics indicate how well a business owner can service their debt. Goldklang says that the best way for the SBA to calculate that ability is by evaluating an applicant’s monthly debt obligations.

Along these lines, although it’s important to accurately report all of your liabilities and assets on your SBA personal financial statement, you’ll also want to take care in providing information on any installment accounts that you pay monthly—like car loans, student debt, and your rent or mortgage payments.

Who needs to fill out SBA Form 413?

Most SBA loan programs—including the 7(a) loan and 504/CDC loan, two of the agency’s most popular loan programs—require that you complete SBA Form 413 as part of your application.

Additionally, depending on your business entity, the following individuals will also need to fill out and submit their own versions of the SBA personal financial statement:

-

-

Each limited partner with 20% or more interest and each general partner

-

Each stockholder owning 20% or more of voting stock

-

Any guarantor of the loan

It’s important to note that if you’re married and file a joint tax return, your spouse will need to be included on SBA Form 413. Similarly, any applicable spouse from the list above will also need to sign off on their versions of Form 413.

What information is needed to fill out SBA Form 413?

All in all, completing an SBA loan application is extremely time-consuming. Therefore, to help streamline the process, you’ll want to gather supplementary documentation and information ahead of time, especially when filling out SBA Form 413.

On the whole, the SBA won’t necessarily request photocopies of these documents, but you can consult these documents to accurately provide current valuations and additional details about all your relevant assets and liabilities. This being said, you’ll want to ensure that any documents you consult—and will potentially need to provide—should be dated within 30 days of your listed “as of” date (which we’ll explain below).

With this in mind, here are some of the documents you’ll want to gather ahead of time to help you fill out the SBA personal financial statement:

-

Personal checking and savings account statements

-

IRA statements and statements from other retirement accounts

-

-

Documents concerning any personal investments such as stocks or bonds

-

Pay stubs showing your annual salary

-

Documents showing any additional income information

-

General market data about your cars, homes, and other personally owned property

-

Mortgage statements, auto loan statements, credit card statements, and documentation of any other personal debt

As we’ll do in our steps below, you’ll want to review SBA Form 413 before you start filling it out. This way, you’ll know exactly what information you’ll need to provide, and the supporting documents you might need to consult to fill in this personal financial statement.

How to fill out SBA Form 413

With all of this background information in mind, let’s start breaking down exactly how to complete SBA Form 413.

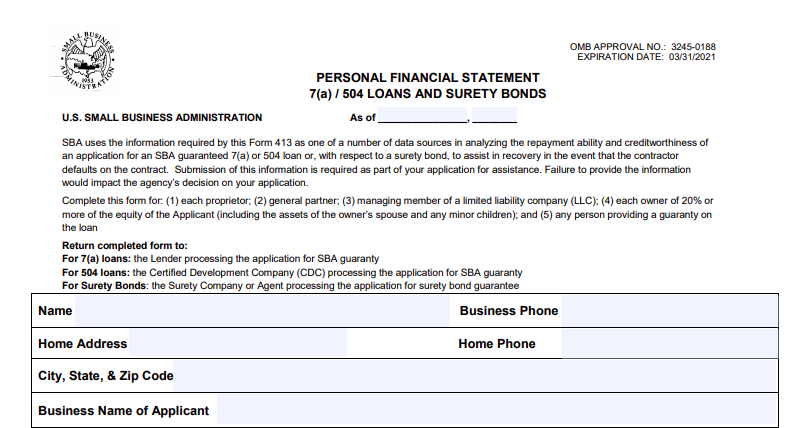

Step 1: Fill in basic business information.

The first step to complete SBA Form 413 (shown below) is the most straightforward—you’ll just need to provide your personal contact information. If you’re married and will be providing information about your spouse’s personal financial information, you’ll want to include their name in this field as well.

In the middle of this part of the form, toward the top, you’ll see a field called “As of.” This field does not necessarily refer to the current date—rather, this conveys to the SBA the date up to which your provided information is accurate. The “As of” field is especially important with regard to valuations, which need to be as up-to-date as possible.

Therefore, it’s best practice to enter the last day of the month preceding the month in which you’re applying (e.g. September 30 if you’re applying in October). You’ll also want to keep in mind that your SBA Form 413 needs to be dated within 90 days of your business loan application.

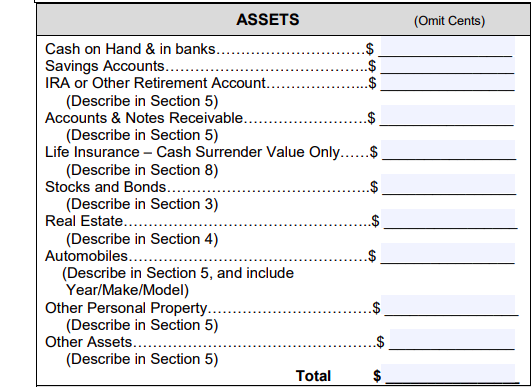

Step 2: Add information about your assets.

After you’ve completed the basic information at the top of your SBA personal financial statement, you’ll move along to the “Assets” section, shown below.

In filling in this section, you’ll add the following pieces of information, rounding your valuations to the nearest dollar amount.

-

Cash on hand and in banks: The amount in your and your spouse’s checking accounts.

-

Savings accounts: Include the amount in any money market and CD accounts too.

-

Retirement accounts: The value of your IRA or any other retirement accounts in your name, as well as your spouse’s name (if applicable).

-

Accounts and notes receivable: You’ll only need to fill this out if you’ve personally loaned money and that amount is still owed to you.

-

Life insurance—cash surrender value only: If your life insurance has a cash payout, list the dollar amount you would receive if you canceled it. This only applies to whole life insurance policies, not term life insurance. You’ll describe this in detail in section 8.

-

Stocks and bonds: List the current value of all stocks and bonds owned by you and your spouse.

-

Real estate: List the current fair market value of all commercial or residential real estate you and your spouse own. You’ll describe this in detail in section 4.

-

Automobile: The current fair market value of all cars, boats, planes, or other automobiles you and your spouse own (not the automobiles you’re leasing).

-

Other personal property: Estimate the combined worth of all the valuable material items you own and could sell for cash but that don’t fall into any of the above categories. (Think your home, jewelry, electronics, and antiques.) You’ll describe this further in section 5.

-

Other assets: Estimate the value of any other assets you own that don’t fall into the above categories, including the value of your interest or equity in your business. It’s best to contract a professional valuation for this; but if that’s not possible, you’ll want to undervalue your estimate to avoid fraud charges. You’ll also describe this in detail in section 5.

-

Total: Add up the total value of your assets.

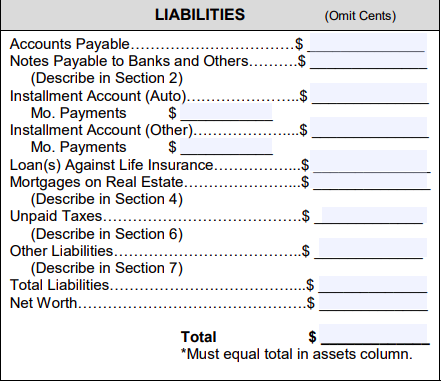

Step 3: Add information about your liabilities.

Next, on the right-hand side of the “assets” section, you’ll find the liabilities box. Here, the same rules apply as they do for your assets—you’ll list the liabilities on your books as an individual (separate from your business’s), and if you’re married, you’ll include the liabilities you hold jointly with your spouse.

Again, in this section of SBA Form 413, you’ll round your valuations up to the nearest dollar amount.

-

Accounts payable: Essentially, this field refers to any debts you owe to another party other than banks, usually on a short-term basis (i.e. 30, 60, or 90 days). Most applicants can leave this section blank.

-

Notes payable to banks and others: This is where you’ll list all outstanding balances on your personal credit cards, lines of credit, and business installment loans. You’ll describe this information further in section 2.

-

Automobile installment account: Provide the total and monthly payment amount of your balance for any outstanding automobile loans.

-

Other installment accounts: List the total and monthly payment amount of any outstanding personal installment loans on your books, including student and personal loans.

-

Loan against life insurance: Provide the balance of any loans you’ve taken out for which you’ve pledged your life insurance policy as collateral (only if it was whole life insurance).

-

Mortgages on real estate: The balance of mortgages on your owned real estate. You’ll describe this in detail in section 4.

-

Unpaid taxes: List any due but unpaid taxes since your most recent filed tax return. You’ll describe this further in section 6.

-

Other liabilities: Provide the total amount of any other outstanding debt not listed in the previous sections. Most applicants don’t have any additional liabilities; but if you do, you can describe them in detail in section 7.

-

Total liabilities: Add up the total amount of your liabilities.

-

Net worth: Subtract your total liabilities from your total assets to determine your net worth.

-

Total: Add your “Total Liabilities” and your “Net Worth.” This value should be equal to your total assets.

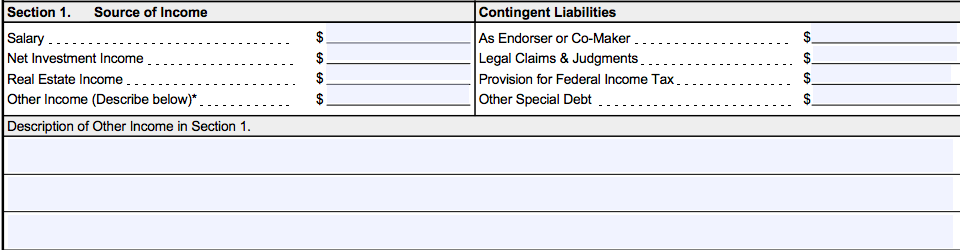

Step 4: Complete section 1 for your source of income and contingent liabilities.

Once you’ve filled in the assets and the liabilities sections, you’ll move on to the final piece of page 1 of SBA Form 413. This part, called “section 1,” will ask for your source of income and contingent liabilities, as shown in the image below.

Source of Income

Here, you’ll fill in the following:

-

Salary: Provide your and your spouse’s total annual salaries, as reported on your tax return.

-

Net investment income: List any income you earn as dividends and interest from your investments.

-

Real estate income: Provide the net income you receive from any of your owned real estate properties, i.e. through sale, lease, or rental. Be sure to list your net income, or the income you earn after expenses.

-

Other income: Provide the total amount of any income received through venues not listed above. This can include alimony, child support, pension, social security, etc. It’s important to note, however, that you should not include alimony or child support payments if you don’t want to have it counted toward total income. You’ll describe the sources of this income in the box below labeled “description of other income in section 1.”

Contingent Liabilities

Contingent liabilities refer to the debts you’re responsible for if certain conditions occur. You’ll estimate the amounts of your contingent liabilities if those conditions are likely to occur.

-

As endorser or co-maker: The total balance of any outstanding debts for which you or your spouse acted as guarantor or co-signer.

-

Legal claims and judgments: The total amount you might owe for any pending legal claims or judgments.

-

Provision for federal income tax: The amount of money you’re setting aside to pay federal taxes for an expected increase in income due to pending litigation, dispute, or asset sale.

-

Other special debt: The total amount of any other outstanding contingent debts not listed above.

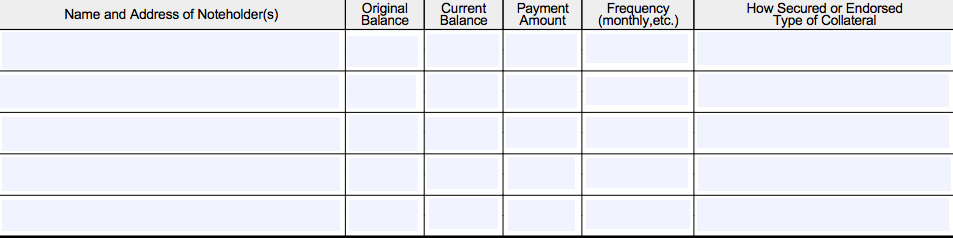

Step 5: Complete section 2 with your notes payable to banks and others.

Next, you’ll fill in section 2 by further explaining all the debts listed as your Notes Payable, as you entered in the Liabilities column above. You should use the table provided (as shown below), and include a separate sheet if you need more space. If you include attachments, you’ll want to make sure they’re identified as part of your SBA personal financial statement and signed.

This being said, you’ll include the following details per debt for this section:

-

Name and address of the noteholder: The name and address of your creditor.

-

Original balance: The balance owed when the credit was first established. This will be $0 for credit cards and lines of credit or the total amount of the loan for installment loans.

-

Current balance: The amount you currently owe.

-

Payment amount: The amount you pay for this debt each month. If it’s an installment loan, list your monthly repayment amount. If it’s a credit card or line of credit, you’ll list “varies.”

-

Frequency: How often you pay your loan bills, i.e. monthly or weekly.

-

How secured or endorsed/type of collateral: Explain the type of collateral you pledged to secure your loan. If it was unsecured (as most credit cards are), list “unsecured.”

Step 6: Complete section 3 with your stocks and bonds.

After you’ve completed section 2, you’ll move on to section 3. Just as you did for your Notes Payable, in section 3 you’ll provide more detail on every stock and bond you and your spouse own, as listed in the Assets column. Again, you can attach as many additional sheets as you need as long as they’re identified as part of SBA Form 413 and are signed.

As shown in the table below, you’ll include the following details for every stock and bond you own:

-

Number of shares: The number you own.

-

Name of securities: The name of this security.

-

-

Market value quotation/exchange: Its current market value.

-

Date of quotation/exchange: The date you calculated its current value.

-

Total value: Your number of shares multiplied by its current value.

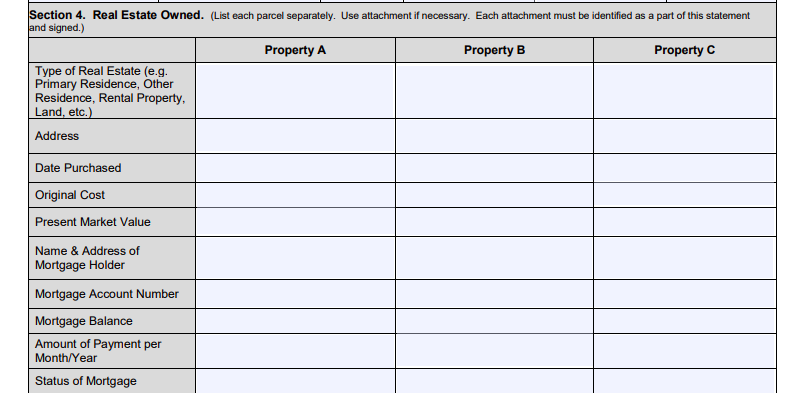

Step 7: Fill in section 4 with the real estate you own.

Once you’ve finished section 3, you’ll continue to section 4 (shown below), which asks for your real estate owned. Here, you’ll explain in greater detail all the property you own, as listed in your Assets and Liabilities.

-

Type of real estate: This may be your primary residence, an investment property, or an undeveloped lot.

-

Address: The property’s address.

-

Date purchased: The date listed on your mortgage.

-

Original cost: The property’s purchase price.

-

Present market value: Ask your broker for a current valuation of the property.

-

Name and address of mortgage holder: The name and address of the bank that holds your mortgage.

-

Mortgage account number: Find this number on your mortgage statement.

-

Mortgage balance: The amount you still owe on your mortgage.

-

Amount of payment per month or year: The amount of your monthly or yearly mortgage bill. If you’ve paid off your mortgage, list “N/A.”

-

Status of mortgage: Write “current,” “foreclosure,” or “paid in full.”

Step 8: Fill out sections 5 through 8 with personal property, unpaid taxes, other liabilities, and life insurance.

Next, you’ll complete sections 5 through 8 on this essential SBA form. As you’ll see below, these sections are all description-based.

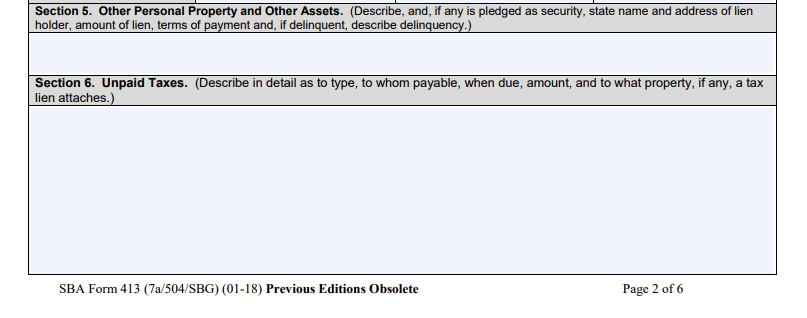

Section 5: Description of Personal Property and Assets

Here, you have the opportunity to go into greater detail about the “Other Personal Property” and “Other Assets” you listed in the Assets column, which will include the value of your stake in the business.

You’ll want to provide as much detail as possible about these items, and you should be prepared to provide documentation to prove their value, if possible. This being said, you may not have a receipt for every piece of property that applies here, like your grandmother’s diamond necklace, for example, and that’s OK. You should just try to make an educated guess as to how much you’d get if you sold your valuables—you shouldn’t, of course, intentionally undervalue or overvalue anything.

If you’ve pledged any of these assets as collateral to secure another type of loan, you’ll need to provide details about that loan, as well. You can use the Notes Payable section as a guide for what information to include. Additionally, if there’s a lien on any of these assets, you’ll need to provide the name and address of the lienholder, the amount of the lien, and the terms and payment. If the loan is delinquent, you’ll need to explain the circumstances of that delinquency.

Section 6: Description of Unpaid Taxes

In section 6, you’ll provide additional information about any unpaid taxes you have, as you specified in the Liabilities section. If you still owe taxes to your state or local government, you can still be eligible for an SBA loan—you just need to prove that you’re on a repayment plan. Here, therefore, you’ll explain to whom you owe taxes, when they’re due, the amount you owe, and whether any of your assets have a tax lien attached.

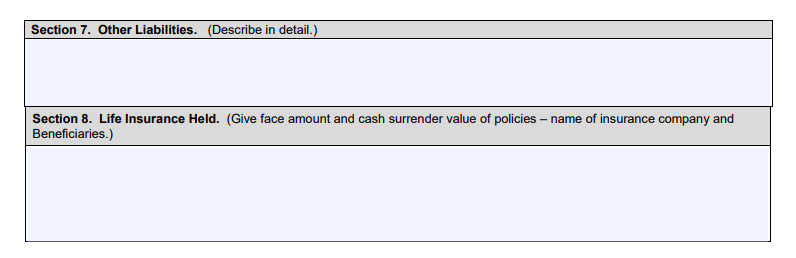

Section 7: Description of Other Liabilities

Once you’ve completed section 6, you’ll move on to the third page of SBA Form 413, starting with section 7. In this section, you’ll explain any “Other Liabilities” you listed in the Liabilities column, if you have them. These are the liabilities that don’t quite fit into the provided categories, such as debts owed to foreign governments or as a result of private agreements. Here, you should provide details such as the type of debt it is, to whom you owe payments, how much you owe, and your repayment plan.

Section 8: Description of Life Insurance

Finally, section 8 will be the last section you need to fill in to complete the main portions of the SBA personal financial statement. In this section, you’ll explain all life insurance policies you hold, including the death benefit, cash surrender value (if applicable), the names of your beneficiaries, and the name of your life insurance company.

Step 9: Review the completed form.

At this point, the hardest pieces of SBA Form 413 are complete. Now, you’ll want to thoroughly review all of the information you’ve provided on this form.

You’ll want to make sure, to the best of your ability, that all of the information you’ve completed is accurate—after all, this statement will be used to determine your loan eligibility. Plus, if you knowingly make false statements on this form, you could be subject to criminal prosecution.

This being said, it may be helpful to ask a third party—like your business attorney, accountant, or loan specialist—to review the form before you complete the final steps. Having a second, or even third, pair of eyes on this document will help you ensure that everything is filled in completely and correctly and, hopefully, will allow you to catch mistakes (if there are any) ahead of time.

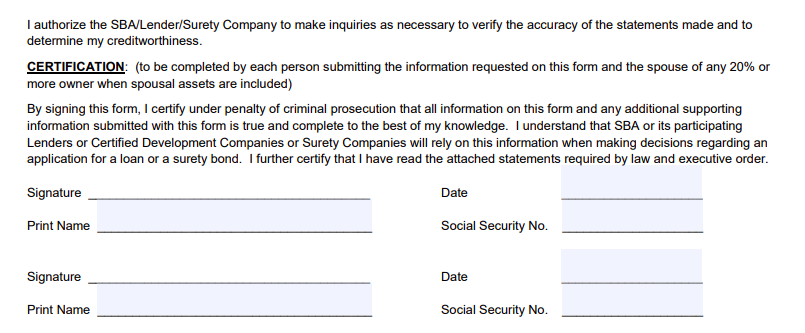

Step 10: Sign and date.

Once you’ve reviewed the information included in your SBA personal financial statement, you’ve reached the last step. Before completing the “certification,” however, you’ll want to make sure you read through the information provided by the SBA on pages three through six of the form.

On these pages, the SBA outlines the penalty for knowingly false statements, as well as statements required by law. If you have any questions about what’s written on these pages, you’ll want to consult your business attorney for clarification.

This being said, after reviewing this information, you’ll want to return to the certification section, where you’ll provide your signature, printed name, date, and social security number. Your spouse will also complete this information for themselves as well.

The bottom line

Many business owners are intimidated by the prospect of filling out their SBA personal financial statements. It can be hard to know which of your assets and debts you should include, which you should leave out, how best to reach their values, and exactly how granular to get in your descriptions.

But Goldklang insists that the process isn’t as intense as it might seem:

“I tell people not to drive themselves crazy here. A lot of people think of their businesses as an extension of themselves or vice versa, and I admire that. But what I tell business owners when I hear their anxiety about the PFS is that this is your opportunity to tell us about your personal assets and liabilities—not your business’s.

So, that car you told me about—is the business paying that off, or are you? Put simply, that’s how you should fill out this form. If you think about it as your item, then put it on the form. If you think of it as the business’s debt, then leave it off.”

This being said, when in doubt, you should be transparent. Ultimately, the SBA needs accurate information to make an informed lending decision. If you’re concerned about a particular debt, you should try to provide as many details as possible to back up the numbers.

One of the greatest advantages of working with a loan specialist on your SBA application, therefore, is that they can advocate for you and help your lender look past those cut-and-dry numbers to understand aspects of your application that need additional explanation.

Plus, if this doesn’t work, then your loan expert can help you come up with an alternative plan if excessive personal debts are precluding your loan eligibility right now, so you can increase your chances of approval in the future.

This article originally appeared on Fundera, a subsidiary of NerdWallet.