The BT (LSE: BT.A) share price has been steadily trending upwards in 2024. Year to date, it has climbed 11.6%.

But even with that, the stock is still down 30.7% over the last five years. Back then, I would have forked out 201.4p for a share. Today, its share price is significantly cheaper at 140p.

However, could that mean BT is now one of the best bargains on the FTSE 100? Its struggles in recent years are well-known. Nevertheless, could this be an opportunity for potential investors to consider snapping up a Footsie stalwart for a slashed price?

Price-to-earnings

While on paper BT shares look dirt cheap, I think it’s important we take a closer look at whether that’s really the case. To do this, I want to look at its price-to-earnings ratio.

As seen below, it currently sits at 16.6. That’s a lot higher than it was at the beginning of the year (6.8). It’s also above the Footsie average of 11. Based on that, while I’d argue BT isn’t overpriced, it may not be the bargain it looks like.

Created with TradingView

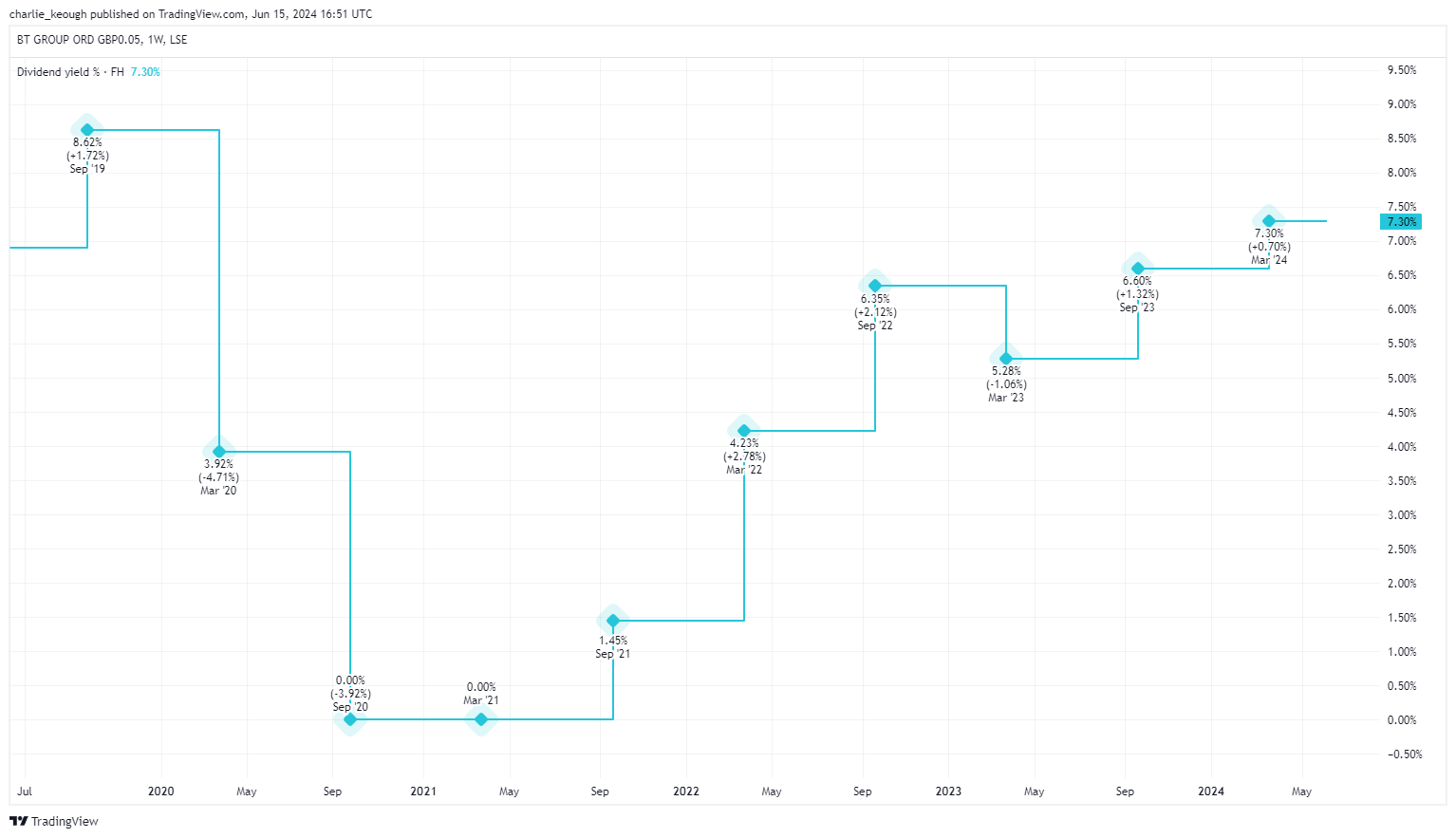

A silver lining

That said, there’s one major positive I see with BT. That’s its bulky dividend yield. As seen below, the stock yields 7.3%. That’s way above the Footsie average (3.6%). What’s more, it has been rising since March 2023.

Created with TradingView

Time to buy?

While I don’t think BT is an attractive investment as it looks on paper, I still see plenty to like about the business.

Its share price has been picking up pace recently largely due to its full-year results released last month. BT has been heavily investing in its fibre optic broadband and 5G rollout in recent years. Finally, it seems like we’re at the point where we could begin to see the positive impacts of this. That has shareholders excited.

There’s also the passive income angle. Its meaty yield is enticing. Management also seems keen to enhance shareholder returns, which is encouraging. Last year it hiked its dividend by 3.9% to 8p per share.

With the firm reaching its maximum capital expenditure for its rollout, this should help boost free cash flow in the years ahead. That could lead to management rewarding shareholders even further with the excess cash it has.

Large debt

But then again, there are factors that may hinder this. For example, looking at its balance sheet, I’m alarmed by the pile of debt the firm has on its books. It continued to rise last year. It now sits at £19.5bn. That’s a concerning amount. The main reason for the increase has been pension scheme contributions.

Another concern of mine is BT’s falling market share as new competitors continue to enter the space.

My move

BT may look cheap but it’s a stock I’ll be avoiding for now. Its debt is my largest concern. I reckon that could hinder growth moving forward.

I see plenty of other FTSE 100 value stocks that look like better buys for my portfolio. I’ll look to pick them up before I consider BT.