The Nvidia (NASDAQ:NVDA) share price is up 2,000% over the last five years. But can the underlying business grow fast enough to justify the increase?

The company has been at the centre of the artificial intelligence (AI) revolution. But a price-to-earnings (P/E) multiple of 69 implies investors are expecting more over the next few years.

Growth

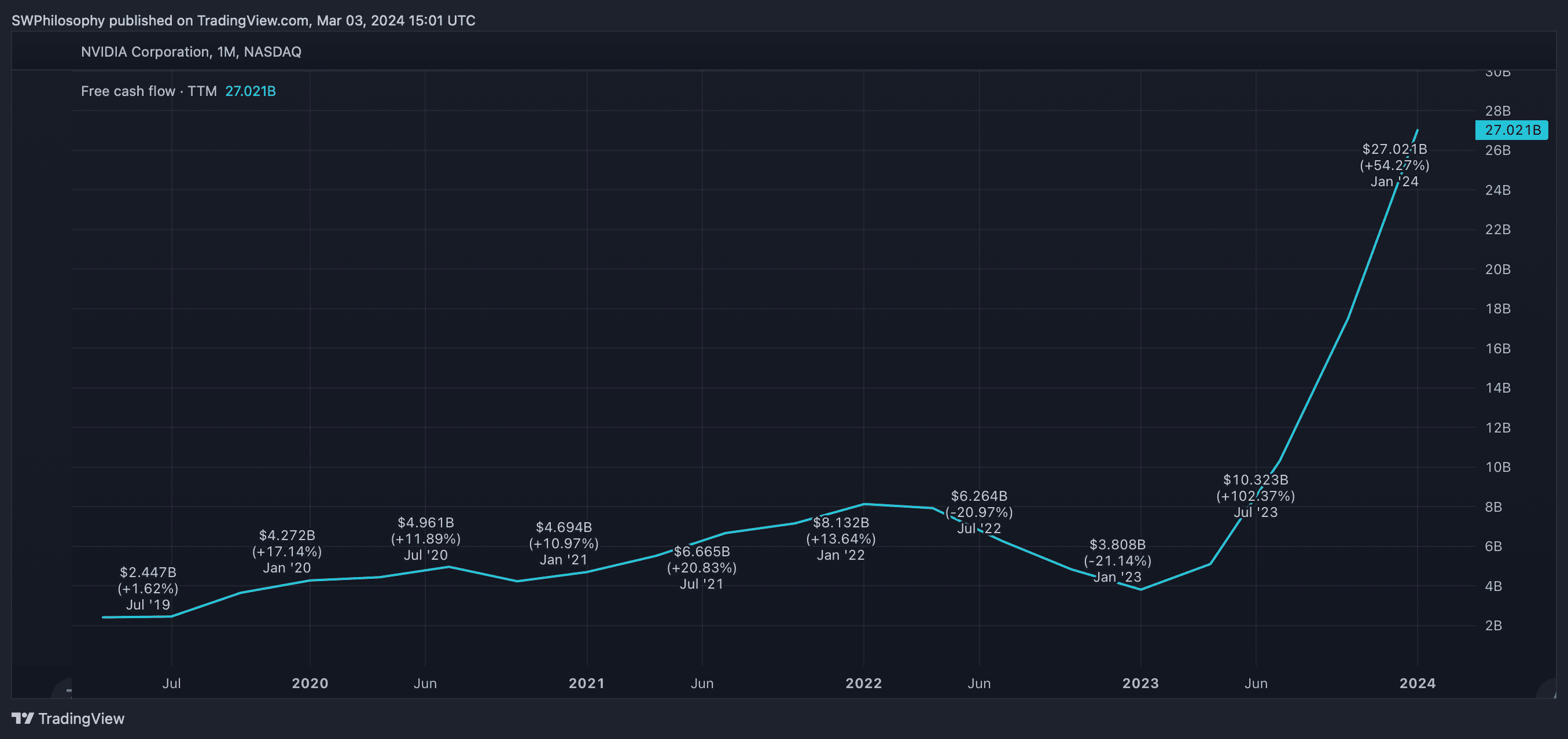

Over the last five years, the firm’s free cash flows have grown at an average of 50% per year. That includes a 232% increase since 2022.

Nvidia Free Cash Flow 2019-24

Created at TradingView

The Nvidia share price, however, has been going up faster. As a result, the stock trades at a higher cash flow multiple than it did in 2019.

Nvidia Price-to-Free-Cash-Flow 2019-24

Created at TradingView

By itself, this isn’t a problem. Five years ago, AI wasn’t attracting the kind of investment it is today.

The trouble, though, is that interest rates are higher than they were before. And this makes buying shares at higher multiples less attractive.

Cash flows

Right now, 10-year government bonds come with a yield of 4.2%. That means Nvidia is going to have to earn enough to offer investors a better return.

With a $2trn market cap, a 4.2% return involves an average of over $80bn in free cash per year. That’s more than Meta Platforms ($43bn), Visa ($19bn), and McDonald’s ($7bn) combined.

Despite its recent growth, Nvidia is some way short of this. In 2023, the company managed $27bn, meaning investors are expecting some significant growth.

To get to the required average, the company will need to increase its cash flows by around 20% per year for the next decade. Otherwise, investors should perhaps expect to do better elsewhere.

Picks and shovels

Nvidia has established itself as a ‘picks and shovels’ company in the AI revolution. Businesses that want to incorporate artificial intelligence into their products need the company’s chips.

This is a big positive, but it isn’t a guarantee either of investment success or of the kind of cash flows that might justify the current share price. The story of Cisco Systems is a good illustration of this.

Cisco was one of the picks and shovels businesses of the internet boom. But investors who bought the stock at its peak in 2000 have had a dreadful time since.

Cisco Systems Free Cash Flow 2004-24

Created at TradingView

Moreover, the company’s cash flows are only just reaching the kind of level that might justify an investment at those levels. And 24 years is a long time to wait for the business to catch up.

Is the Nvidia share price a bargain?

Right now, I think Nvidia’s share price is a bargain if the business can grow its cash flows by 20% per year for the next decade. And while that’s not impossible, it’s also not straightforward.

The business is growing impressively at the moment and has consistently surpassed expectations. But this gets more difficult as the company’s market cap gets bigger.

It’s easy to think Nvidia’s position in the artificial intelligence market makes future success inevitable. Anyone who thinks this though, should consider the story of Cisco.

For my portfolio, I’ve got other ideas for investing in the AI revolution. Nvidia is a really impressive company, but the price doesn’t offer enough margin of safety for me at the moment.