B&M European Value Retail (LSE:BME) is on my list of stocks to consider buying right now. With the shares falling 29% since the start of the year, the dividend yield has reached 3.7%.

Furthermore, I think the stock market is underestimating the company’s growth prospects. While there are challenges, there are also clear opportunities.

Why is the stock down?

B&M isn’t an obvious choice, by any means. Compared to other FTSE 100 stocks, it has quite significant short interest and the share price reached a new 52-week low recently.

Competition is the main reason for this. The company aims to differentiate itself with low prices, but the likes of Tesco and Sainsbury have been competing hard in this area.

The bigger supermarkets also offer a wider range of products. That means unless B&M can meaningfully undercut them on price, customers have an incentive to go elsewhere.

With cost-of-living pressures starting to ease, finding discounts has become less important to shoppers. And this has been showing up in B&M’s results.

In its most recent update, the company reported a 3.5% decline in like-for-like sales. That means its stores generated less in the way of revenues than they did in 2023.

The risk of this continuing is why analysts at UBS have a ‘sell’ rating on the stock. But I think there’s another important metric that investors should pay attention to.

Store expansions

Individually, B&M’s stores might be less profitable than they were a year ago. But there’s a lot more of them and this has been more than offsetting the weak like-for-like sales.

Adjusting for currency fluctuations, the firm’s total sales were up 2.4%. This was the result of opening new stores over the year – and there are another 26 expected in the next nine months.

Ultimately, B&M is hoping to get to 1,200 outlets, which is a lot more than its current base of 741 stores. If it can achieve this – or anything like it – I think the stock is a bargain right now.

Over time, I expect an expanded store count to more than offset low like-for-like sales growth. And with the stock at a price-to-earnings (P/E) ratio below 11, it doesn’t need to grow much.

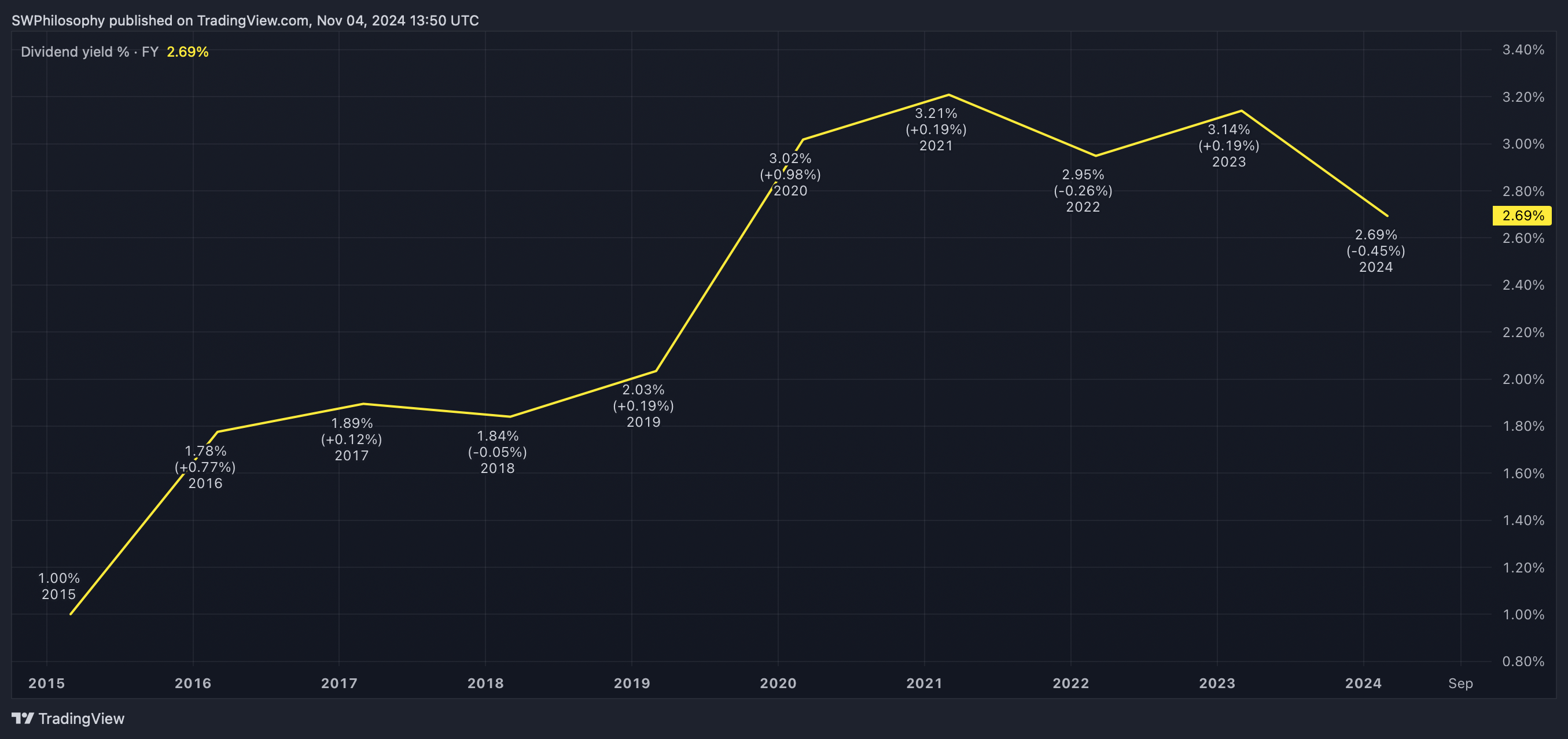

From a passive income perspective, a falling share price has led to a rising dividend yield. At 3.7%, the starting return for investors is the highest it has been at any point in the last 10 years.

B&M Value Retail dividend yield 2015-24

Created at TradingView

With B&M retaining more than 50% of its earnings, I think the chance of a dividend cut is low. That means there could be growth and income ahead – a powerful combination for investors.

Time to buy?

I’m not sure there’s been a better time to buy B&M shares than right now. Competition in the retail space will always be intense, but I think the current share price more than reflects this.

The company is set to report earnings later this month. I’ll be looking at those with interest before making a decision on adding the stock to my portfolio.