It’s been a good year for the Aviva (LSE: AV) share price and about time too. The shares have been idling for yonks and loyal investors deserved a bit of fun.

Aviva shares are up 20.16% over the last 12 months, easily beating the FTSE 100, which rose 11.48% over that time. Yet at 475p they’re still lower than they were a decade ago when they traded at 500p. It’s been a long wait.

Long-term investors shouldn’t feel too hard done by, though, because they will have picked up bags of income along the way. Today, the trailing yield is 7.11%. That’s impressive given the recent share price spurt. So is the trailing price-to-earnings ratio of 12.74.

It’s a brilliant FTSE 100 income stock

Low valuations and high yields seem to be the default setting for FTSE 100 financial services companies at the moment. That may reflect the turbulent period we have been through, with the pandemic and cost-of-living crisis hitting sales and stock prices.

As inflation falls and interest rates potentially follow, I’m hoping this will change. I think big yielders like Aviva will look more attractive to income seekers once savings rates and bond yields start to fall.

I’ve been saying that for some time, but with central bankers still wary of cutting rates, it hasn’t really been put to the test yet. Goldman Sachs reckons UK base rates could fall from 5% today to 2.75% this time next year. If it’s right, that to be good for Aviva, surely.

Lower borrowing costs should boost stock markets, which will increase the value of its assets under management and make customers feel better off, too.

The 14 analysts offering 12-month price targets for Aviva plc have a median target of 546.5p per share. If they’re right, investors can look forward to another 15% growth over the next year. With the yield forecast to hit 7.3%, their total return could top 20% again.

I’d like to see more dividend cover

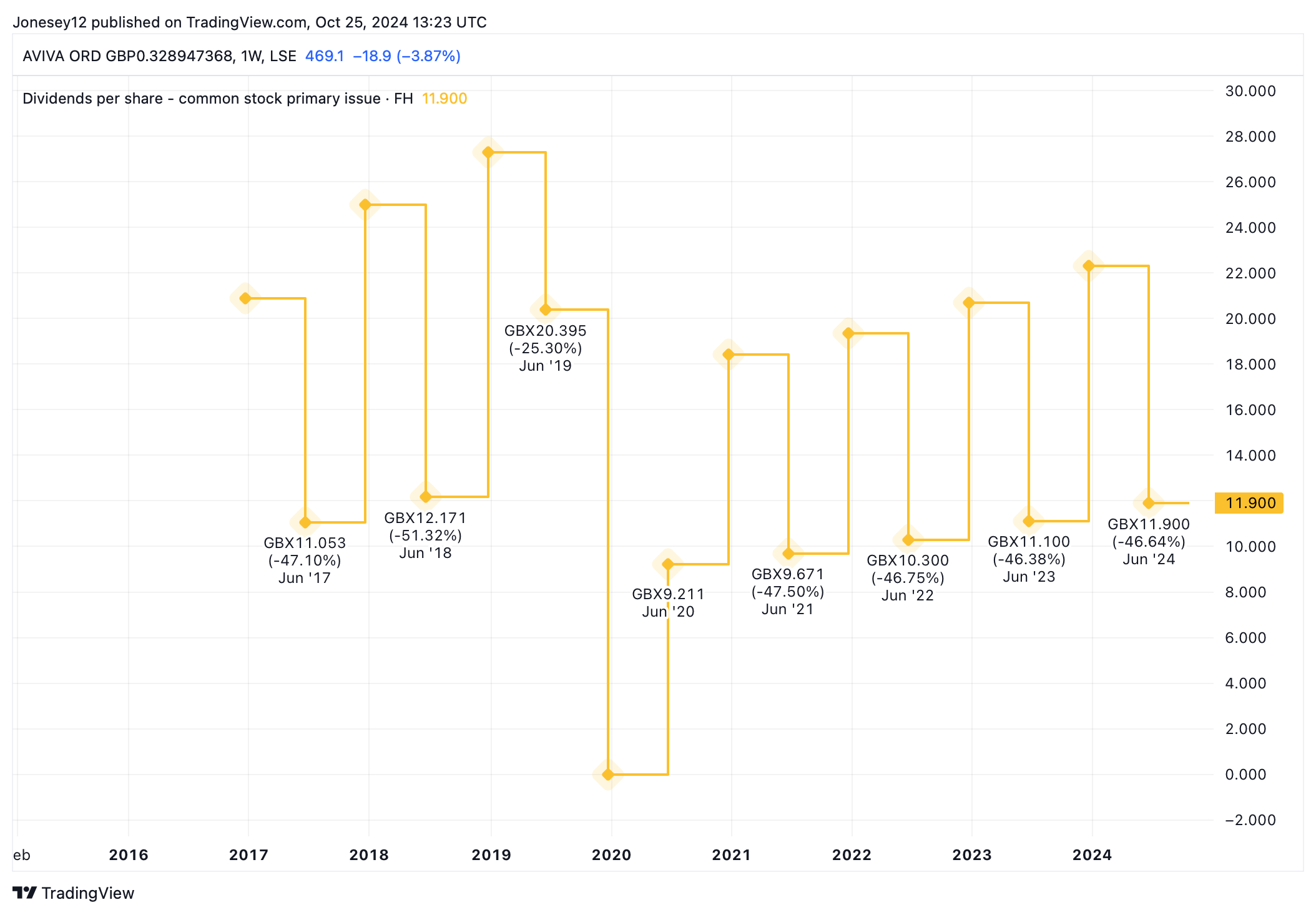

I’m a little concerned that Aviva’s forecast dividend is only covered 1.3 times by earnings. I’m comforted by the recent track record of steady dividend growth, although the board took the opportunity to rebase it after the pandemic year. Let’s see what the chart says.

Chart by TradingView

Also, the board felt sufficiently confident to declare a 7% increase in its interim dividend to 11.9p, announced in its first-half results on 14 August.

Aviva has set high standards for itself. First-half statutory profits jumped 58% to £645m, but it will need to maintain the pace of growth to keep investors happy. The shares are likely to drop if it falls short.

Aviva has a growing role in workplace pensions, something CEO Allison Kirkby has highlighted. There’s a risk that employers will scale back contributions if Labour makes them pay national insurance on top in the Autumn Budget.

Personally, I’m overexposed to the insurance sector, as I hold shares in both Legal & General Group and Just Group. If it wasn’t for that, I’d buy Aviva like a shot.