Calling a FTSE 100 stock a no-brainer buy’s quite an honour. I wouldn’t extend it to many companies. Yet I think I can use that phrase to describe consumer goods giant Unilever (LSE: ULVR). It’s one of my core portfolio holdings.

This doesn’t mean I think it will always outperform. In fact, it’s struggled in recent years. Stock markets go through cycles, and so do individual companies. Yet Unilever has tremendous resilience.

It’s been doing the business for more than a century. Today, it sells its products across 190 countries, with a staggering 3.4bn people using them every day. Most people will recognise dozens of its food, hygiene and beauty brands, which include Ben & Jerry’s, Domestos, Dove, Hellmann’s, Sunsilk and many more.

I hope to hold Unilever forever

Unilever has a massive presence in emerging markets, which make up 58% of its turnover, giving it access to growing army of consumers.

Yet success brings its own problems. Management’s desperately been trying to streamline its overly complex operation. Sprawling is the word often used.

It also faces a battle attracting young talent who can be dazzled by whizzier sectors like tech and finance. Sustainability is another challenge, given the amount of plastic packaging it requires. Former CEO Alan Jope’s efforts to find a new direction by making brands stand for something “more important than just making your hair shiny, your skin soft, your clothes whiter or your food tastier” also didn’t connect.

The inflation shock didn’t just make consumers feel poorer, it also drove up the cost of raw materials, squeezing margins on both sides.

So there’s a fair bit to exercise the brain power here. But as I said, there will always be good times and bad times. New CEO Hein Schumacher has enjoyed a solid start, but he must go further to get Unilever flying again.

It’s still at the recovery stage

Things are looking up though. The Unilever share price is up 19.27% over the last year.

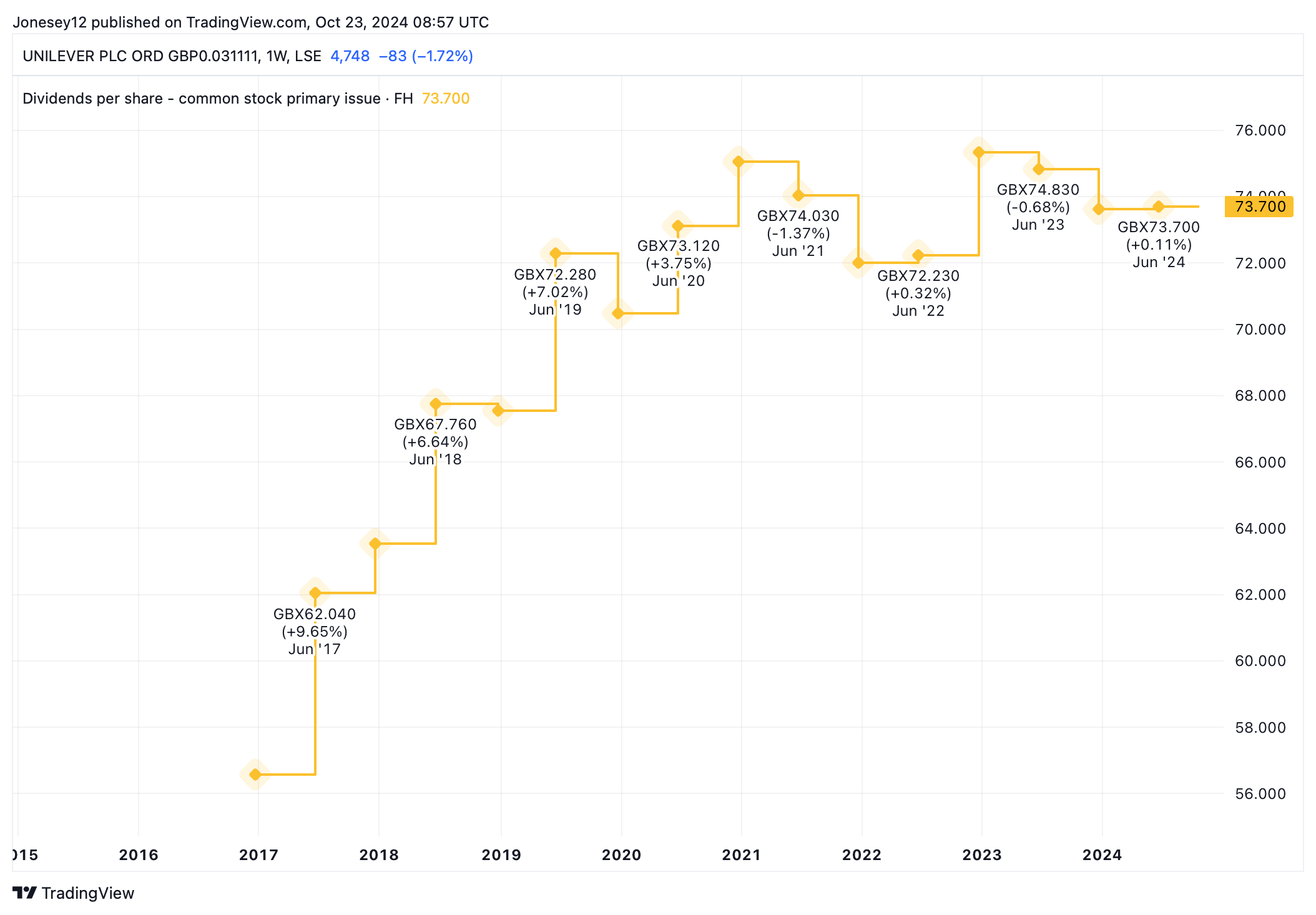

Investors will have got dividends on top. A trailing yield of 3.12% may be below the FTSE 100 average of 3.5%. Dividend growth has slowed since the pandemic but the board recently hiked the quarterly payout by 3%, as this chart shows. It also launched a whopping €1.5bn share buyback.

Chart by TradingView

I believe that with a long-term view, this £118bn company’s a no-brainer buy and hold. It has tremendous defensive characteristics as it sells the type of products people buy in bad times as well as good.

The board’s been focusing its marking spend on its 30 Power Brands to good effect. They posted 5.7% underlying sales growth in the six months to 30 June. Operating margins are forecast to jump from 16.4% to 18% this year. Unilever’s return on capital employed is a thunderous 67%.

As interest rates fall, and (with luck) the US economy engineers a soft landing, I expect Unilever’s recovery to continue, albeit at a slower pace. I’ve got a pretty big holding, so won’t buy more. I’ll just let my shares do their thing for a decade, and maybe even two.