The Vodafone (LSE: VOD) share price is a disaster more than two decades in the making. Shares in the FTSE 100 telecoms giant peaked at 550p in March 2000. Today, they trade at just 73.84p.

That’s a total fall of 86%, although to be fair, it’s a little misleading. Global share values were inflated across the board in March 2000, thanks to the dotcom boom. The tech bubble burst that month and continued to deflate for two years, losing half its value.

We should probably praise Vodafone for surviving that debacle. Many similar companies went the way of the dodo.

Tech crash victim

It’s the last decade that worries me. Vodafone shares have dropped 60% over 10 years, as the board battled to get the global behemoth into shape. It looks like the worst is now over. The stock is up a modest 1.51% over 12 months. However, over six months it’s up 14.86%. That’s dizzying by its standards. Is there more to come?

I love a supersized dividend yield as much as any investor. Yet I’ve never been tempted by Vodafone. There’s not much joy in getting a 10% income if my capital is taking a regular beating.

Worse, that mighty yield was primarily a product of the falling share price. Shareholder payouts were slashed by half in 2019 then frozen at €0.09 for five years. In its 2025 year, dividends will be slashed in half. Today’s trailing yield of 10.37% is misleading. It’ll be roughly half that.

Vodafone did slightly better than expected in FY24 as organic service revenues rose 6.3%, with Europe, Africa and its Business division all on the up.

It’s also made a heap of disposals, including the sale of Vodafone Spain, Italy, Hungary and Ghana, and sales of its stakes in Vantage Towers and Indus Towers. But the battle to simplify its sprawling operations is far from won.

FTSE 100 income stock

Total first-quarter revenues rose 2.8% year on year to €9.04bn, but it’s still a case of one step forward, two steps back. Growth in Africa and Turkey was undermined by a slowdown in Europe and falling sales in Vodafone’s key German market.

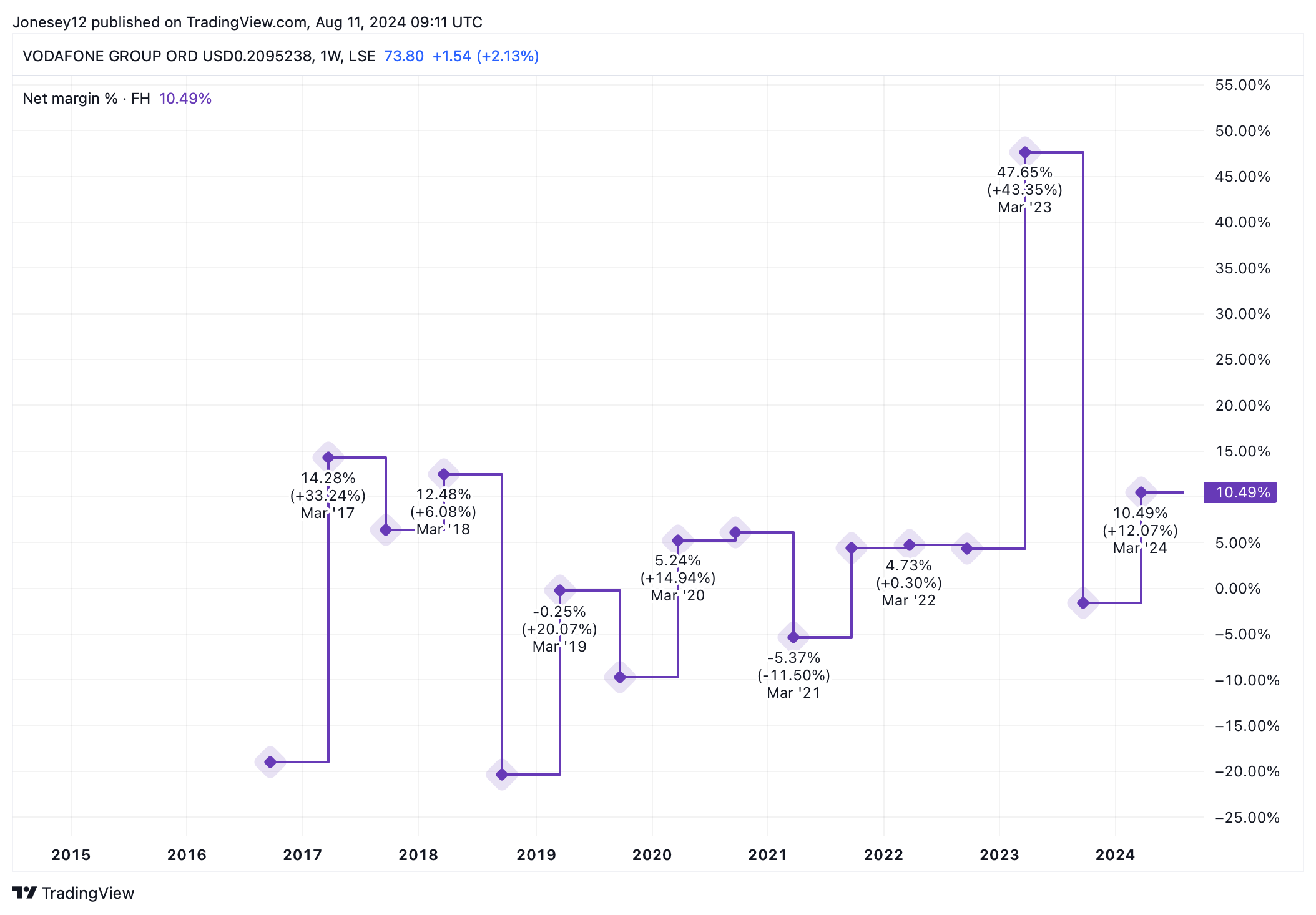

It’s been a similar story for years, which is often the case for large companies with their fingers in too many pies. Net margins have been patchy too, as this charts shows.

Chart by TradingView

The board expects to generate adjusted EBITDA of €11bn in 2025, but that’s broadly in line with last year. Forecast adjusted free cash flow of “at least” €2.4bn is actually down from €2.6bn in 2024 and €4.14bn in 2023. However, disposals play a part in this.

Despite its troubles, Vodafone is still a huge global brand, and its relatively new CEO Margherita Della Valle seems to be getting a grip. Trading at 11.51 times earnings, the shares don’t look that expensive, either. And on Wednesday (7 August), it announced a share buyback programme of up €500m.

I wouldn’t say it’s in deep value territory, because I think the board will take a long time to unleash that value. But for me, Vodafone is back in play. I won’t buy it today, as I can still find better prospects on the FTSE 100. But I’m no longer ruling it out.