I regularly invest in the stock market to build up a passive income stream for retirement. My strategy is to invest in high-yield income stocks until I reach a point where I can live off the dividends.

But how realistic is this goal?

Well, here’s my plan detailing what I need to do (and how much I have to invest) to achieve this goal.

Laying the groundwork

First, I would open a Stocks and Shares ISA. This allows me to invest up to £20,000 a year in any assets of my choice with the gains being tax-free.

There are many other ways to invest in assets but I can’t think of a more efficient option.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice. Readers are responsible for carrying out their own due diligence and for obtaining professional advice before making any investment decisions.

Then I need to figure out how much passive income I want and how much I need to invest to achieve it. I’m not aiming to spend my retirement in five-star hotels or on luxury yachts. I just want to be comfortable and carefree without having to count my pennies.

The average annual UK salary for a full-time position is currently around £35,000. It’s unlikely I’ll need that much in retirement as my pension will cover most of my living costs. However, I must also account for inflation.

To be safe, I should aim for a minimum of £24,000 a year. My current portfolio returns, on average, 10% a year with dividends, so I would need a pot of £240,000. But to account for bad years and economic slumps, 8% is probably a safer average to work with. That would require £300,000 in my pot.

How can I build up that much?

How do I get there? One word: slowly.

However, by making regular contributions to my ISA and reinvesting the dividends, I can compound the returns and speed things up.

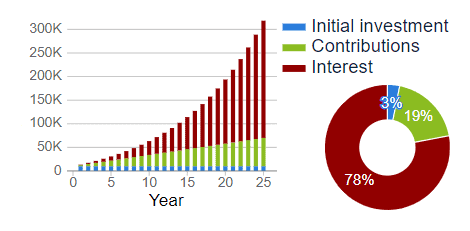

For example, a £10,000 initial investment combined with monthly contributions of £200 would reach only £60,000 in 10 years. But if I continue for another 10 years it could climb to over £180,000 and after 25 years, £300,000.

The stocks I’d choose

I’ve already added several high-yield dividend stocks to my passive income portfolio, including HSBC, BT and Aviva.

But there are still a few promising stocks I like the look of, one of which I plan to buy this month.

As the parent company of Standard Life and SunLife insurance, Phoenix Group (LSE: PHNX) is the UK’s largest long-term savings and retirement business. And with a 9.7% yield, it’s currently the second-highest on the FTSE 100. Although it only started paying dividends in 2010, they’ve increased 66% since then.

But I’ve been hesitant to buy for two reasons: I don’t know the company very well and it’s been unprofitable for several years. However, while the share price is down 30% since late 2020, it’s starting to show signs of recovery. Since hitting a 10-year low of 441p in October last year, it’s recovered 23% and it may become profitable again this year.

Naturally, years of losses have hurt the balance sheet. Now with £6.18bn in debt and only £3.54bn in equity, Phoenix’s debt-to-equity ratio is concerning, at 1.74. It’s probably not the highest on the FTSE 100 but I’d feel more comfortable seeing it decrease.

All things considered, it looks to me like a reliable, high-paying dividend stock on the road to a solid recovery.