The Taylor Wimpey (LSE: TW) share price has been going gangbusters, it’s up a staggering 53.71% over the last year. I’d expect that kind of return from a FTSE 250 growth stock, rather than a FTSE 100 housebuilder in the middle of a cost-of-living crisis.

That’s good news for me, because I bought Taylor Wimpey shares on three different occasions last autumn, at an average price of 123.66p. Today, I’d have to pay 151.60p. I’ve also received two dividends, and reinvested both. Taylor Wimpey shares have much further to go, in my view. I’m not the only one who thinks that.

FTSE 100 growth hero

The shares jumped when Labour won the election, as markets expect the firm will be a key beneficiary of chancellor Rachel Reeves’ push to build more homes. Yet I think investors have slightly got ahead of themselves.

Taylor Wimpey has warned it will struggle to complete 10,000 homes this year. That’s down from 14,154 in 2022 and 10,848 in 2023. It will need some big incentives to turn that around in a hurry. Especially if it hopes to maintain build quality.

Also, while PM Keir Starmer has pledged to “bulldoze through” planning reforms, change won’t happen overnight.

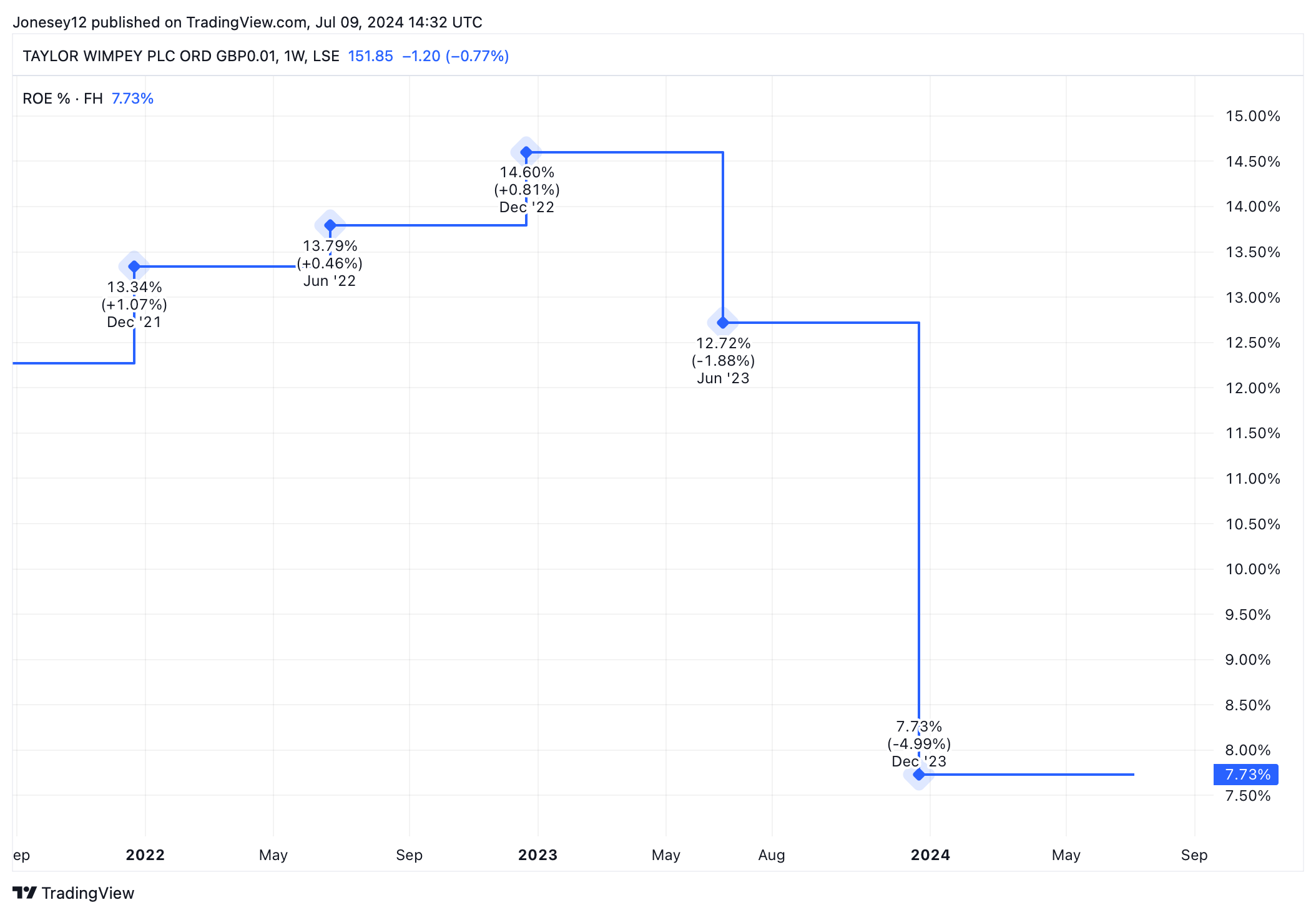

High interest rates, the rising cost of labour and materials, and the slowing economy have left their mark on Taylor Wimpey. Its return on equity has plunged. Let’s see what the charts say.

Chart by TradingView

There’s a danger the share price has raced ahead of fundamentals. I bought Taylor Wimpey at a valuation of around six or seven times earnings. Today, it’s valued at 15.22 times. So it’s not the bargain it was.

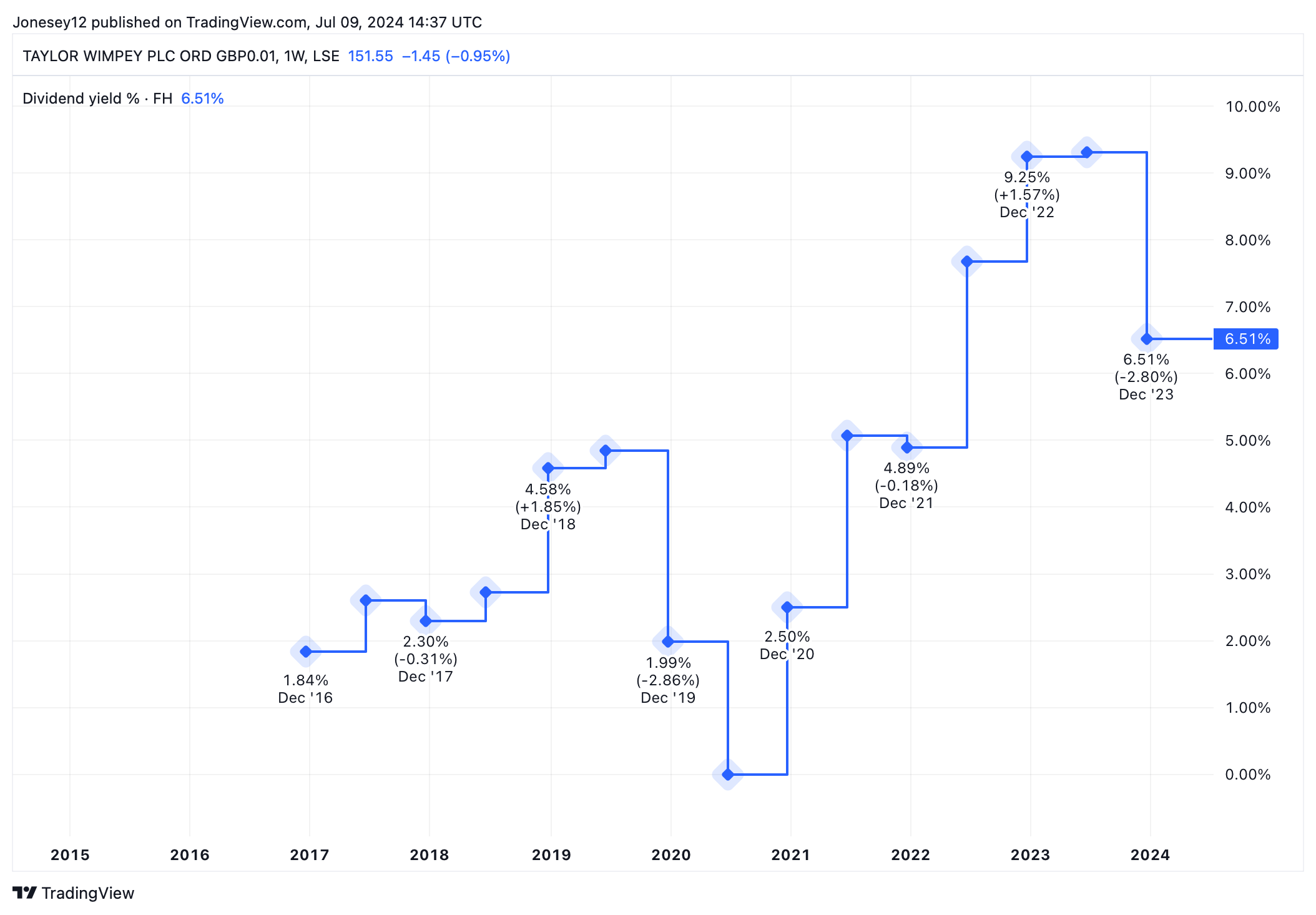

Solid dividend income

While the yield has retreated from the blockbuster 9.25% we saw in December 2022, it still looks pretty solid. Let’s look at another chart.

Chart by TradingView

Markets are forecasting income of 6.11% in 2024 and 6.25% in 2025. While marginally lower, at least it’s slowly climbing. The board has pledged to maintain dividends at every stage of the house market cycle, and return around 7.5% of net assets to shareholders annually, worth at least £250m a year. With £837m in net cash, today’s high yield looks sustainable.

When interest rates finally start falling, savings rates and bond yields will follow. With luck, Taylor Wimpey dividends will continue to rise, making the stock look even more attractive and drawing in new investors.

Naturally, there are risks. Interest rates may not fall as much as we would like. Taylor Wimpey may struggle to boost completions, with labour in short supply. If Starmer does manage to get 1.5m homes built in five years, increased supply could hit prices.

Obviously, the ideal time to buy Taylor Wimpey shares was a year ago. But I think today is pretty tempting too. The only thing stopping me from buying more is that I already have a big chunk of my pension tied up in this stock.