Typically, I don’t expect a high-growth UK share to be good value as well. But I think meat, pastry and sandwich retailer Cranswick (LSE:CWK) fits both bills.

The stock is up just shy of 30% in the last year and a brilliant 237% over the last 10 years. As far as FTSE 250 companies go, I think this one could be a great addition to my portfolio.

Despite a price gain over the last decade that’s massively higher than the FTSE 250’s mere 19% growth over the period, Cranswick isn’t exactly a hot stock in the news. That’s a good thing in some ways because it means I can find a good deal before others catch on.

The meat business

Most of Cranswick’s revenue comes from the UK, with just another 2.2% coming from continental Europe and the rest of the world. Also, 99% of its money comes from selling food.

Crucially, the company is focused on sustainability in its farming processes. This increases its long-term prospects at a time when ethical production around animal products is under more scrutiny.

As of the last annual report, it mentioned it had “22 well-invested, highly efficient facilities in the UK”.

Of its major competitors, three stood out to me as particularly strong contenders for Cranswick’s market share:

- Boparan Holding Limited (2 Sisters Food Group)

- ABP Food Group

- Hilton Food Group

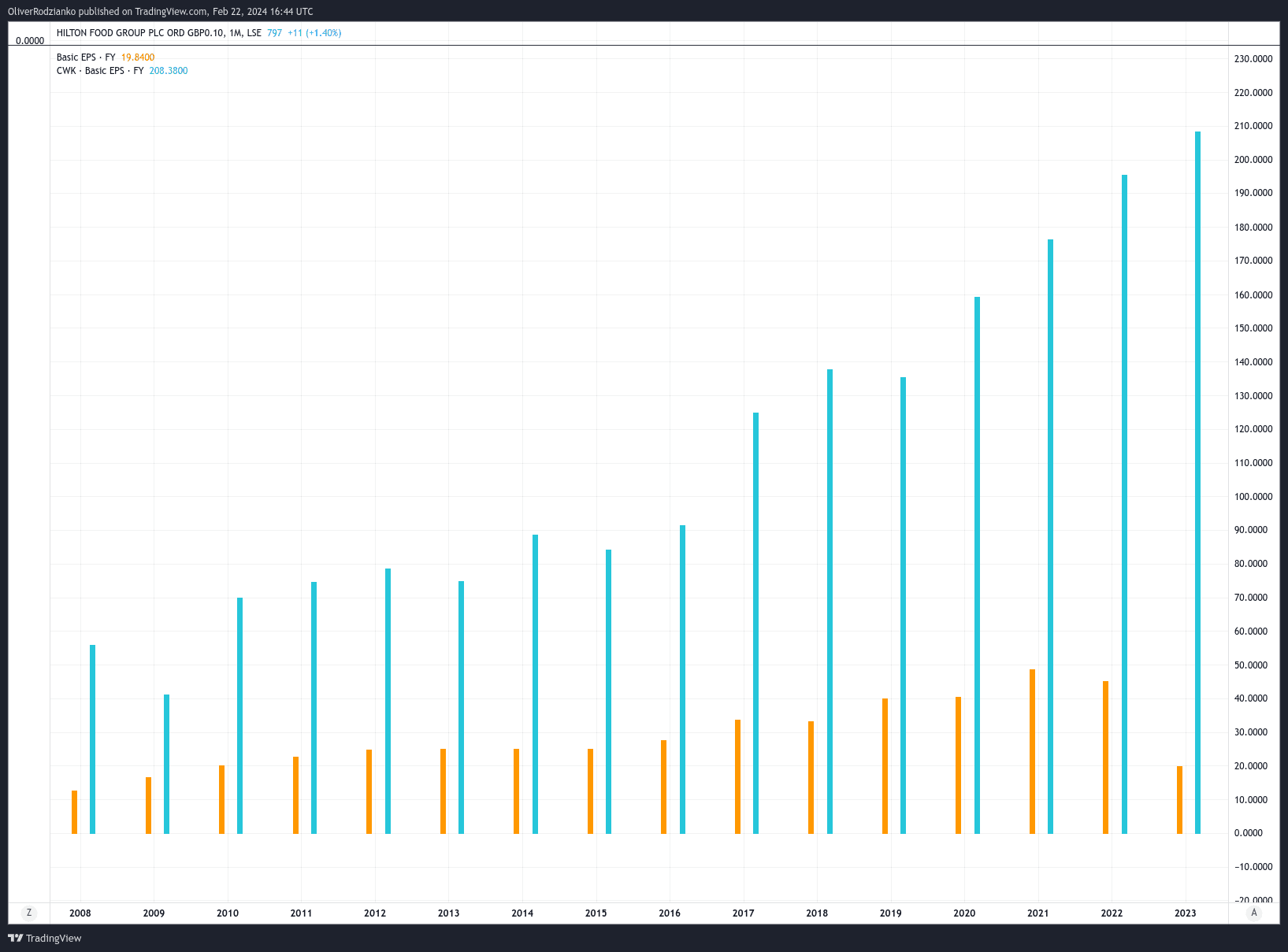

To focus on a company that’s publicly traded, Hilton Food Group seems a viable alternative investment option to Cranswick. So, I compared the two on earnings per share over time, a key indicator of profitability:

In Pence – Hilton, Yellow – Cranswick, Blue – Source: TradingView

Clearly, Cranswick provides more net income. But which of the two companies brings in the higher percentage of revenue as earnings?

Hilton, Yellow – Cranswick, Blue – Source: TradingView

Cranswick clearly wins on both fronts and by quite some way. Bear in mind, I think these are both great companies to have a stake in, so considering Cranswick is that much more profitable, it really stands out as a hot pick to me.

Every investment has risks

By looking deeply at the company’s annual reports and investor relations, I came across its risk management framework.

The firm has outlined one of its core risks as being subject to reputational damage. That would be as a result of adverse media. Largely, it attributes this to “alleged animal welfare incidents, protests, vigils or other operational challenges”.

Also, as almost all of its revenue comes from the UK, it notes that a “deterioration in the UK economy, or a change in food consumption patterns could lead to a fall in demand for the group’s products”. That’s a result of its low geographic diversification, something Hilton Food Group has much more of.

While these are just two risks of several Cranswick outlined in its report, I think it shows two crucial ones I need to consider if I invest.

Why I think it’s still cheap

At the moment, the shares have a price-to-earnings ratio of around just 16. That’s low considering how fast its stock price has been growing over the last year and its track record over the past 10.

Now, I don’t think there’s a massive safety net in price here, but Cranswick is cheap enough for me to put it on my watchlist.