Junk-rated companies in the U.S. have “meaningful exposure” to interest rate hikes by the Federal Reserve, raising concerns over defaults as a potential recession looms, according to Jim Reid, head of thematic research at Deutsche Bank.

In an emailed note Tuesday, Reid looked at companies’ exposure to floating-rate debt. “While the overall US and EU corporate exposure is low, junk-rated US & European corporates have substantially higher exposure,” he wrote.

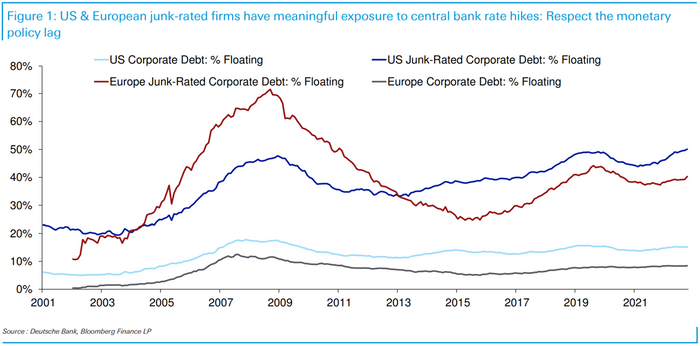

“US junk-rated debt is now 50% floating-rate today, an all-time high,” Reid said in the note. “The rapid growth of the leveraged loan market is the root cause of this vulnerability,” he said, pointing to the chart below.

DEUTSCHE BANK RESEARCH

Leveraged loans are a form of floating-rate debt that can be considered risky as they’re typically used to finance companies rated below investment-grade, or in junk territory. Private-equity firms use leveraged loans to help finance their buyouts of companies, with the acquired businesses taking on the debt burden.

Companies with a heavy debt load risk having a tougher time meeting their debt obligations in an economic downturn.

While “maturity walls” make a difference, “leverage is up to two times more important in our models explaining historical defaults,” Reid said. “High debt to sales ratios will expose very high leverage when profits margins compress (assuming a recession), leading to distressed exchanges and missed interest payments.”

The U.S. loan market is “most exposed,” due to lower ratings, sector composition and greater exposure to higher rates, he warned.

Read: This isn’t a ‘close your eyes and buy anything’ kind of market

Investors have been worried that the Fed’s rapid pace of rate hikes to cool the economy in an effort to tame high inflation risks tipping the U.S. into a recession. The central bank’s tightening of monetary policy works with a lag.

Deutsche Bank has forecast that U.S. high-yield corporate bond defaults could climb to 4.5% by the end of 2023, with U.S. leveraged loans potentially seeing a higher rate of 5.6%, according to Reid’s note. But by the second half of 2024, “we forecast peak defaults” of 9% in U.S. high yield and 11.3% in U.S. loans, he wrote.

The SPDR Blackstone Senior loan ETF

SRLN,

which provides exposure to non-investment-grade, floating-rate loans, has lost around 5% so far this year on a total return basis through Tuesday, FactSet data show. That compares with an almost 16% drop for the S&P 500

SPX,

on a total return basis over the same period.