Lloyds Banking Group (LSE:LLOY) has enjoyed some impressive share price gains over the past month. The FTSE 100 stock has risen an impressive 16% in that time, making it one of the index’s top-five performers.

Yet at 49p per share, the Black Horse Bank still looks dirt cheap. Could this give it scope for further meaty price gains?

Today, Lloyds shares trade on a forward price-to-earnings (P/E) ratio of 7.3 times, well below the Footsie average of 10.5 times. Meanwhile, its 7.3% dividend yield blasts past the 3.8% FTSE 100 average.

Yet I’m still not convinced. As a long-term investor, I remain concerned about how the share price will perform over the next decade.

3 risks to the price

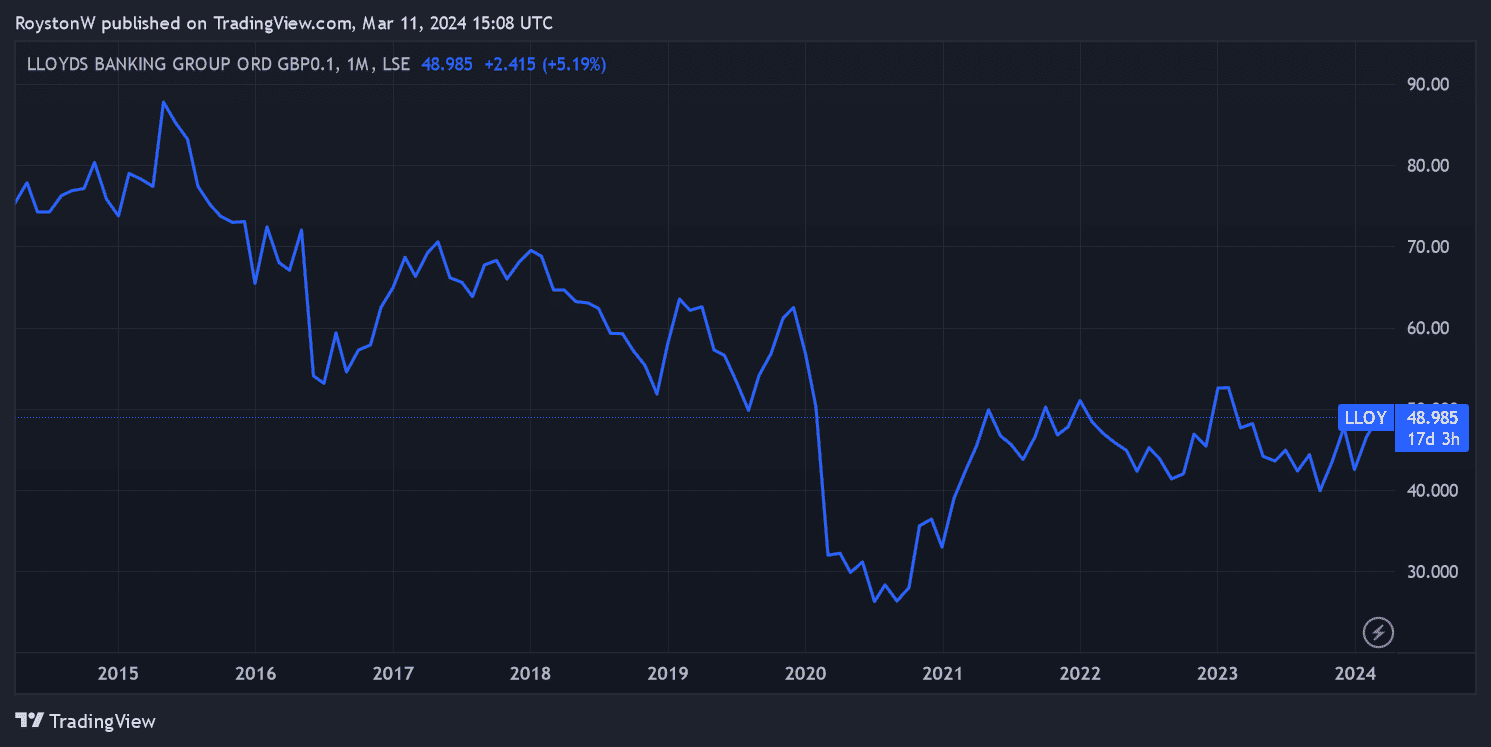

Even after its recent gains, Lloyds shares are 34% cheaper than 10 years’ ago. And it’s more than 10p cheaper than it was before the Covid-19 crisis.

Chary by TradingView

Past performance is not a reliable indicator of the future. But the problems that have depressed the bank’s shares over the past decade look set to endure looking ahead. These include:

Low interest rates

As mentioned, banks’ profits were boosted from a series of interest rate hikes from late 2022. But with inflationary pressures abating, the Bank of England could start slashing rates again in the coming weeks, putting severe downward pressure on their net interest margins (NIMs).

NIMs are the difference between the interest banks charge borrowers and what they offer savers. It’s a key profitability metric that disappointed following the 2008 financial crisis when interest rates were slashed. Could history repeat itself?

Weak economic growth

A period of prolonged economic weakness has hit high street bank profitability in recent history. Unfortunately for Lloyds et al this looks set to remain the case. The British Chambers of Commerce, for instance, expect sub-1% growth over the next two years, and a 1% increase in 2026.

Enduring (and significant) structural problems like low productivity, labour shortages, and high public debt mean this economic stagnation could be set to endure too.

And unlike peers such as Barclays, HSBC and Santander, Lloyds doesn’t have exposure to foreign markets to help it grow earnings in this tough climate.

Rising competition

The mature nature of the UK banking market makes it difficult for established banks to grow earnings. And their task is made all the more difficult by the intense competition they face from challenger and digital banks, many of whom are expanding their product ranges.

Things could get even tougher too, if the tie-up between Nationwide and Virgin Money sparks fresh bouts of industry consolidation.

Here’s what I’m doing now

On the plus side, owning Lloyds shares could remain a good way to source passive income in the years ahead. Despite having to cut dividends during the pandemic, the FTSE bank has a brilliant record of delivering large shareholder payouts over the past decade.

The FTSE 100 share has a strong balance sheet to help it carry on this path too. Its CET1 capital ratio was 13.7% as of December.

However, I’m still not tempted to buy the bank for my portfolio. There are plenty of top FTSE 100 and FTSE 250 shares that offer the possibility of solid capital gains and hefty dividend income during the next 10 years.