Passive income is crucial for anyone looking to achieve financial freedom. As Warren Buffett says, those who don’t find a way to make money while they sleep will work until they die.

Investing in dividend stocks are a great way of earning cash without having to work for it. And there are some opportunities at the moment, but I don’t think they’ll be around forever.

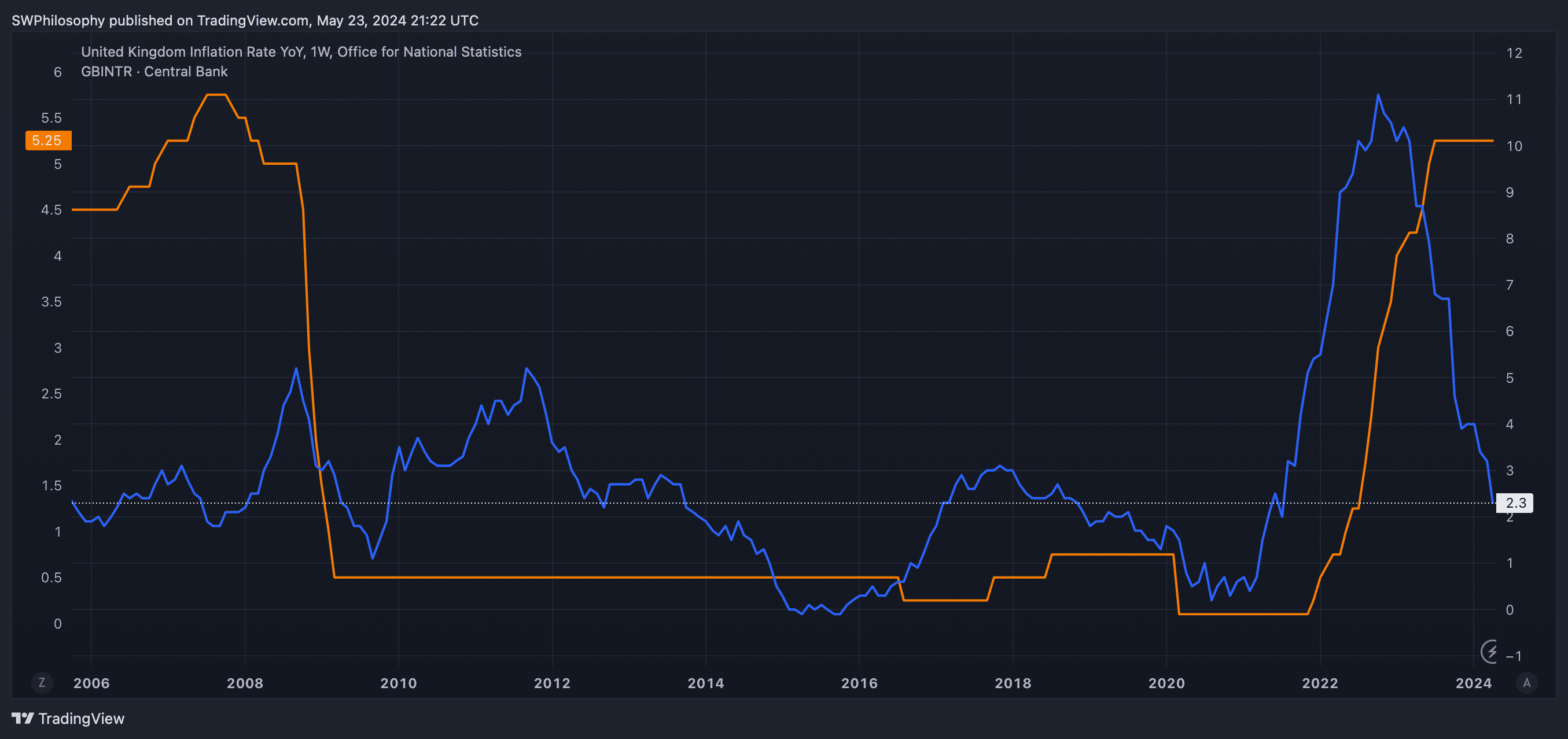

Inflation and interest rates

Interest rates in the UK are at their highest levels since 2008. And that’s caused dividend yields to rise to some unusually high levels.

This has been because inflation in the UK has also been unusually high. But that’s changing – the rate of price increases has been falling and is close to the Bank of England’s 2% target.

UK interest rates vs. inflation 2004-2024

Created at TradingView

Given the correlation between inflation and interest rates before, I’m expecting rates to come down before too long. And if that happens, dividend yields should follow.

The market agrees – the latest consensus expectation is for interest rates to start falling from August. That means time might be running out to buy some dividend stocks.

Primary Health Properties

Shares in Primary Health Properties (LSE:PHP) are 11% cheaper than they were a year ago. As a result, the dividend yield has reached 6.7%.

The company is a real estate investment trust (REIT) with 27 years of consecutive dividend increases. This makes it a dividend aristocrat, but investors should be aware of a certain risk.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice.

The amount of debt on the firm’s balance sheet is a lot – even by REIT standards. And the more Primary Health Properties owes, the harder it will be for the business to keep growing.

Lower interest rates would be a big help with this though. If these start to emerge, I don’t think the stock’s going to come with a 6.7% dividend yield for much longer.

Games Workshop

Games Workshop (LSE:GAW) is a very different type of business in a couple of ways. First, it isn’t required to distribute its earnings to shareholders – it does this out of choice.

Second, the company has a much stronger balance sheet. It doesn’t have the same debt to worry about, but it could still benefit from lower interest rates.

The biggest risk with the stock comes from weak consumer spending. Its products aren’t essential, so the business is vulnerable if customers find their budgets under pressure.

If interest rates fall though, lower mortgage costs should boost disposable income. This could send Games Workshop shares higher, so I’m aiming to lock in a 4.5% yield while I can.

Buying opportunities

I’m convinced the next move for interest rates is down, not up. And this means dividend yields are likely to be lower in the future than they are now.

Right now, I think there are opportunities for dividend investors in a variety of sectors. That’s why I’m scrambling to load up on shares before prices go up.